The floating buoy lidar designed to measure the winds and calculate the movements of waves and … [+]

AFP via Getty Images

Part 1 (published 4/12/2020), dealt with the parallels between the automotive LiDAR and telecom optics investment booms, and posited that going forward, consolidation and pivots for LiDAR companies are inevitable. Part 2 (this article) discusses which types of companies will survive as stand-alone entities in the AV LiDAR space, and the factors dictating how the remaining companies consolidate and survive. I also present a few ideas for new directions in LiDAR that I think have been overlooked and present ripe areas for innovation and funding.

One of the questions I dealt with in a recent article was whether LiDAR was even essential for AV deployment. I felt this question needed to be answered prior to Part 2 – the conclusion was that as things stand, LiDAR is critical but competing approaches in cameras, AI, imaging radar and V2X could potentially be disruptive, and need to be monitored by AV and LiDAR companies. The latter should be paranoid about these disruptive developments and focus on providing compelling performance that cannot be matched by anti-LiDAR developments. Lower performance LiDARs will naturally have a tougher case to make in this regard.

Several recent news events are germane to the discussion here. Tesla recently announced a plan to provide ride hailing services (with a human driver) by mid-2021, with a plan to go driverless once enough driving experience accumulates (6B Autopilot miles and 1M vehicles on the road). Since Tesla is well known for pushing a non-LiDAR approach, its success means trouble for LiDAR. On the other hand, AV companies in the US and China that use LiDAR are gaining significant public acceptance during the COVID epidemic (and hopefully its aftermath) by providing ride hailing and grocery delivery services that minimize human contact. This is good news for LiDAR companies.

On the AV front, there is sobering news. The COVID crisis has put tremendous cash flow pressures on automotive OEMs, with subsequent scaling back of investments on AVs. Ford is in a particularly difficult situation with its dismal stock price, difficulty in obtaining financing and suspending their dividend payments. It is likely that they will need substantial help and delay their AV efforts. GM-Cruise recently announced an 8% reduction in staffing in areas such as business strategy, design, and product development, following on the heels of Ike, Velodyne, and Kodiak. Zoox, the vaunted Silicon Valley unicorn with an ambitious vision of using purpose-built battery driven AVs for ride sharing is finding a difficult time raising more money and could likely get acquired. And hold your breath – even Waymo had to raise almost $3B recently because they acknowledged that developing AVs is expensive (and presumably because the new Alphabet management is getting what we all routinely go through – the “other bets” syndrome). These events are likely to multiply and trickle down, with a natural impact on the survival of many AV focused LiDAR companies. They all simply cannot survive going forward.

Why Do So Many LiDAR Companies Exist Today?

Primarily because of the large number of technology options that exist at this point – in the choice of wavelengths, scanning mechanisms, waveform types, laser options and detection modalities. LiDAR companies emphasize one or more of these as their core competence and IP focus, with the added attributes of overall system design, manufacturability, scalability, and cost. All reasonable stories in the early days of the technology, with the promise of AVs being imminent and massive quantities of revenues for all in the food chain. Circumstances today are different than over the past 5 years. The boom is past, AV deployment faces a long slog ahead, and the funding picture is challenging. And the market is simply not big enough for investors to continue funding the large number of LiDAR companies that exist today.

The Strongest Companies Will Survive

These are the companies who have:

1) An embedded and committed base of customers who have designed their software stacks around their products

2) Strong relationships and penetration with the OEMs, other mobility providers (trucking, delivery, campus shuttles) and AV players

3) System performance consistent with requirements for urban & highway AVs

4) Great teams

5) Significant levels of funding ($100M+)

6) Products with demonstrated automotive grade manufacturing and reliability

7) Credible supply chain and manufacturing relationships, with scaling to automotive grade manufacturing and reliability

8) A credible story for costs and profitability

9) Significant presence in other markets – security, construction automation, etc.

Captive LiDAR efforts are likely to survive because they meet many of the attributes listed above. However, even these are not immune – as part of the 8% staff reduction, the LiDAR effort at Strobe (which Cruise acquired in the rich old days) was impacted. Funding and money do play a part here, although other factors are probably also at play – GM-Cruise may be planning to go forward without a LiDAR or the internal effort was simply not paying off in terms of performance and viability.

For Tier 1s (Valeo, ZF, Aptiv, Continental), LiDAR is a natural business opportunity in terms of supply of a critical component to OEMs for ADAS and AVs. It also enables them to supply sensor fusion systems with cameras, radar and LiDAR. Additionally, Bosch is also reportedly developing their own LiDAR. Some AV companies (GM-Cruise, Waymo, Aurora, Argo, Yandex) prefer an internal LiDAR effort either because of perceived supply chain issues, cost reduction, and most importantly design control to enable efficient integration and performance optimization of their AV hardware and software systems.

These captive efforts put significant pressure on independent LiDAR providers, who not only have to overcome and exceed performance and cost expectations relative to these captive efforts, but also need to manage their funding and cash flow as they await the AV revolution. It is likely that < <10 independent companies will survive as stand-alone AV LiDAR entities over the next couple of years. The remainder will either pivot successfully into other applications or get acquired (by the captives or the stronger independent LiDAR companies). Or, unfortunately, face bankruptcy.

I asked Martin Pichinson (Co-Founder of Sherwood Partners with 40+ years of experience in handling IP sales restructurings and bankruptcies) regarding the parallels between the dot.com era boom and bust, and the current environment for AV companies. Mr. Pichinson has been working with such companies since 1994 and knows what can happen during difficult times. Martin Pichinson “There are parallels between the dot.com era boom and bust, and the current environment for AV companies. This is the Second “Great Unwinding.” We are now going to be diving deep into services, which include AI, Robotics, Changes in Healthcare, IoT and more. The human has finally accepted the changes technology has offered and will now embrace them with open arms. It is no longer a long sales job – create the right products and they will come. We are attached.” Hopefully, the consolidation process ensures that the LiDAR players with the right product will survive.

Consolidation Scenarios

Processing of the raw LiDAR data and its subsequent integration into the AI and software stacks that provide perception and sensor fusion is probably the most critical driver for how the consolidation scenarios will play out. Critical features of the LIDAR that impact this include:

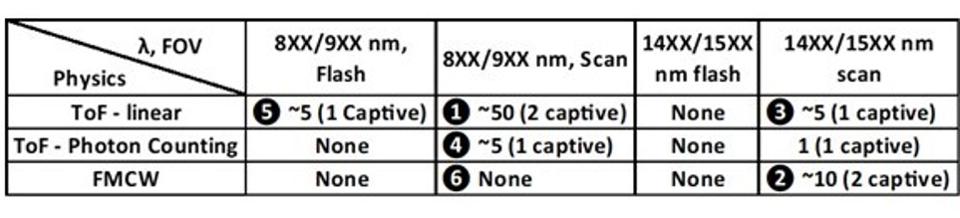

1. LiDAR physics, primarily, ToF with linear detectors, ToF with photon counting detectors and FMCW: each of these options require different software and signal processing algorithms and integration into the perception and sensor fusion stacks. Additionally, the types of laser and detectors used across these three categories are dramatically different and impacts the supply chain, cost, and scalability.

2. Operating Wavelengths (8XX-9XX nm, 14XX-15XX nm): affect the calibration and thermal management aspects, and to a significant degree, the supply chain, manufacturability, and cost aspects.

3. FoV coverage (Flash vs scanning) – the big distinction here is between flash and scanning, which significantly impacts the signal processing and post processing stack as well as hardware integration. The specific scanning mechanism does not matter at the fundamental level – whether mechanical, opto-mechanical, MEMs or solid state

For example, it is unlikely that a company doing 1550 nm, ToF lidar with linear mode detectors and flash operation would acquire one focused on 905 nm, photon counting detectors and mechanical scanning. The integration of hardware and software between such systems is not straightforward and does not create any accretive value (other than providing a second stand-alone system to complete its suite of offerings although this type of consolidation play seems unlikely at this point). It is more likely that they look to acquire instead specific capabilities in the supply chain like lasers, detectors or scanning technologies to create more vertical integration around specific areas of competitive differentiation and reduced BOM costs.

Table 1: Factors Impacting Consolidation Decisions (Cells indicate LIDAR companies in each category) … [+]

SSR 2020

Table 1 lays out the ~75 LiDAR companies across the 3 major LiDAR physics approaches. For the reasons described above, I think consolidations will first occur within these cells. My predictions are as follows:

❶ offers the highest possibilities of consolidations in the immediate timeframe. Many companies are in this category, with at least 5 strong ones (including the captives). The remainder are not as strong and will likely get acquired or go bankrupt. It is worth noting that this category pioneered the era of automotive LiDAR, however it has limitations on resolution and range performance due to eye safety constraints. It also has the least amount of vertical integration in terms of owning the design of the lasers and detectors.

❷FMCW LiDAR companies currently use the 15XX nm wavelengths (primarily due to availability of coherent lasers developed for the telecommunications industry). However, these lasers are challenging to make and control for free space applications where significantly more launch power is required to achieve long range performance. Unlike other LiDARs, FMCW provides depth and axial velocity information, which reduces processing time for image segmentation and object recognition (and leaves more time for decision making and control). An added advantage is that because of low optical peak powers, this type of LiDAR offers possibilities of purely solid-state scanning using Optical Phased Arrays and Liquid Crystal Meta-surfaces. (both of which need significant material science innovations to productize). Blackmore, which pioneered the FMCW approach was recently acquired by Aurora, but there are other standalone companies pursuing this direction. Unfortunately, only a few of them have the high level of funding required to continue independently and are likely to get acquired or conduct IP sales. The critical IP here is in the transmission waveforms deployed and the subsequent coherent mixing and data processing. This type of LiDAR offers a path to high performance critical for forward and rear LiDARs for highway AV operation.

❸14XX/15XX nm LiDAR has a natural advantage in terms of higher performance due to higher margins on eye-safety. The companies in this category have demonstrated excellent performance over long range using linear mode APDs or PINs. But laser peak power remains challenging, with many of them using expensive fiber lasers which are difficult to scale at high volumes. Some of these companies, notably Luminar recently announced a partnership with Volvo for AV deployment in 2022. This is not a highly populated cell, and possibilities for consolidation here are unclear, primarily because the performance is only possible with expensive fiber lasers and solving this will need significant financial investments.

❹ This cell is intriguing because it promises CMOS like costs for SPADs and use of low cost, VCSEL laser arrays. Like ❸, this is not a highly populated cell, although I think some consolidation is likely to occur here.

❺The advantage of this cell is that it uses no scanning and offers camera-like point clouds. Fusion with cameras becomes a lot easier and issues of image lag are eliminated. However, illuminating a large number of pixels requires significant laser power, confining their application to short-range applications like self-parking or longer ranges with poor angular resolution or field-of-view coverage. It is unclear whether LiDARs in this category will play a big role in AV deployment. Consequently, consolidation scenarios here are unclear, and pivots into non-automotive applications more likely.

What Should VCs With a Ton of Money with Nowhere to Go, Do?

It is not all gloomy and depressing. There are still promising areas of new investment that VCs and entrepreneurs should consider. Here are a couple of suggestions:

1) It is amazing to me that cell ❻ in Table 1 has not drawn any entrepreneur interest or VC/corporate money. FMCW LiDAR at 8XX-9XX nm has the potential to solve the inherent challenge of eye-safety constrained performance at these wavelengths that ToF systems are limited by. This is because the systems can operate with higher SNR using local oscillators, and therefore extract higher range performance than with the same amount of launched laser energy. Immunity to interference and Doppler based instantaneous velocity sensing (similar to 1550 nm FMCW) are other significant advantages. This high performance can be achieved at significantly lower cost since the systems can use lower cost silicon detectors and GaAs lasers and VCSELs. Additionally, SiN photonics eventually offers a path to solid state scanning in the future. In short, ❻ offers all the advantages of ❷ with the cost benefits of ❶. There is a catch – coherent lasers at these wavelengths do not exist in production, although there is nothing fundamentally limiting from a design perspective to make this happen. You do need a good team of laser designers as part of the team.

2) Over 90% of the data generated by a LiDAR for obstacle avoidance is generally useless. Collecting, storing, and analyzing all this data creates significant power, storage and latency challenges and does not enable resolution and laser resources where it is needed. Event based LiDAR therefore is another area to consider as an investment opportunity. Investments in event-based cameras are already occurring and these same principles could be used for event based LiDARs, although in a scanning mode, innovation in event based fast scanning also needs to occur.

3) Sony recently released a low-cost camera chip that implements AI processing functionality at every pixel in the array, enabling high-speed edge AI processing. This reduces dramatically the quantity of raw data that must be transmitted into post processing stacks, and improves metrics on latency, power consumption and costs. Investments in LiDAR systems that accomplish this type of data reduction is potentially a significant opportunity and integrates well with event-based LiDAR).

4) Solid state scanning is something that can truly make chip scale LiDAR a reality. Apart from the usual fascination with eliminating moving parts (in a moving car no less!!), solid state scanning will positively impact cost, scalability, and chassis-compatible LiDAR (critical for consumer ownership of AVs). It can also enable LiDAR in other applications like cell phones, AR/VR, and gaming. There is some funding in this area, although not to the scale required to solve complex materials engineering issues.

Apart from these areas of opportunity, pivots into non-AV applications is also a direction to consider. These include security, people monitoring, mining, construction, factory and warehouse automation, robotics, and agriculture. Urban Air Mobility (UAM) and drones also offer a promising pivot, although this is likely to take a while to develop and monetize. Essentially all LiDAR companies today are presenting themselves as engaged in many of these areas. Quanergy, one of the early unicorns in the AV LiDAR space, recently announced a funding round led by its existing investors along with the following message:

“While many LiDAR companies are focused on building LiDAR solely for transportation purposes, since its inception, Quanergy has emphasized the development of its technology for multiple industries,” said Dr. Kevin J. Kennedy. “With this new capital, we are deepening our investment in our team and our technology and are positioned to prove the value of LiDAR for broader market applications.”

A harbinger of events to come. It is going to be an exciting ride. However, you will need to drive yourself or tolerate another human driver for most of the ride. Cars that are designed for social distancing should do rather well.