Editor’s note: Seeking Alpha is proud to welcome Aseity Research as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Sundry Photography/iStock Editorial via Getty Images

The sharp decline of the F5 Inc’s (NASDAQ:FFIV) share price means that value investors can snap up a strong company that has consistently beaten yearly revenue estimates at a bargain.

Shares fell 14.8% on the 28th of Jan following the release of the company’s earnings report and its projected revenue growth for this year. Citing the ongoing concern of global supply chain issues, the company revised its revenue growth estimates to 4.5% to 8%, which is down from a previous forecast of 8% to 9%.

Although it is impossible to know when the global supply chain issues will end, I feel it is also inevitable that it will come into balance again eventually. Therefore, I believe that the drop in F5’s share price is the result of irrational mispricing by the market. To further support my thesis, the growth of F5’s software and security product line, which it has gradually pivoted towards through a series of acquisitions and internal product development over the years, was forecasted to be unaffected by supply chain issues and will instead grow “near the top” of its 35% to 40% guidance range, while its global services revenue, or revenue which is dependent on the delivery of physical products through the global supply chain, will grow at 1% to 2%.

By looking at F5’s financials over the last three years, the trend of the company growing its software revenue while its hardware revenue shrinks as per a change in its strategy looks set to continue, so even in the unlikely worst case scenario that the global supply chain is fundamentally broken and won’t be resolved in the foreseeable future, F5 is still well positioned for consistent growth as it has doubled its addressable market.

Company Overview

To provide some context of where F5 sits in competitive scene, I’ll briefly touch on two of its most recent acquisitions as well as its operating segment and how it is positioned for future opportunities. Acquisitions are what helped the company respond to trends of how its market uses and secures its cloud and physical infrastructures, and ultimately set F5 up for increased projected growth in the future.

In 2021, F5 acquired Volterra which provides application delivery and security solutions through a SaaS subscription model. In the same year F5 also acquired Threat Stack, a company that provides cloud security and workload protection services. These acquisitions allow F5 to provide application security and delivery solutions in any environment, be it through on-premises products or in the cloud. The bigger picture is that these acquisitions have doubled F5’s addressable market from $14 billion in 2020 to $28 billion in 2023.

According to F5’s latest annual report, the business has one reportable and operating segment, which it describes as “the development, marketing and sale of application services that optimize the security, performance and availability of network applications, servers and storage systems.” This statement to me reflects the company’s strong commitment towards reshaping its business model towards selling software.

F5 has moved towards a software business model over the last three years, with software making up 40% of its total revenue in 2021, up from just 24.3% in 2019. With the company’s acquisitions in mind, I don’t think it’s unreasonable to expect this number to grow to greater numbers as it tries to reposition itself as not being seen as just a hardware company.

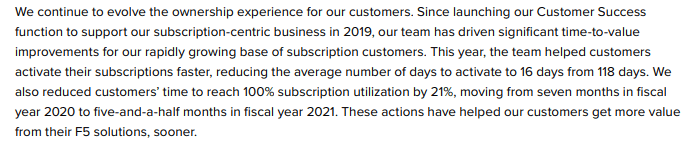

Total net product revenues grew in each consecutive financial year, growing 2.4% in 2021 and 5.4% in 2020. Crucially, there is some evidence that F5 has already successfully begun moving its pieces into play to deliver on the pivot towards a subscription-centric business. Taken from the company’s most recent annual report, F5 has significantly reduced the time it takes for its customers to activate their software subscriptions, reducing it down to just 16 days from 118 days.

F5 Inc Excerpt (F5 Company Report)

This metric means its sales and customer service teams have become much more efficient in converting its sales opportunities into paying customers. Another promising development is the company’s increase in 100% subscription utilization, which grew to 21%. My theory is that a greater utilization of the company’s products means there will be less reason for its customers to churn, and therefore the company will retain more of them in the future.

Segment Growth Opportunities

The future growth of F5’s revenues is catalyzed by several strong customer trends in the software and security industries. I feel that these trends will make the company’s revenues resilient to the current, and future supply chain issues if they emerge. More importantly, I estimate that they will also send F5’s revenues higher than their current and previous levels, which would increase the company’s free cash flows and valuation.

BIG-IP

BIG-IP is F5’s proprietary software suite for managing application availability, performance, security, and access control in cloud and data centre environments. Owning BIP-IP confers F5 several competitive advantages. Used with the company’s traffic management operation system, the software can be deployed in any environment, which reduces development time and cost to its customers.

The biggest advantage of the company owning BIG-IP is its potential synergy through integration with the products of its acquired companies, which I predict will increase the company’s brand awareness and boost market share. For example, in March 2019, F5 acquired the open source developer NGINX. As a competitor to Apache, NGINX is the world’s most popular web server software that powers over 400 million websites worldwide.

NGINX Market Share (NGINX.com)

A total integration with F5 would see NGINX become a web server as well as application server running on BIG-IP software, exposing F5’s suite of security, access control, and load balancing software to potentially millions of new users.

In its recent annual report, the company states that it has experienced growth in several key use cases of its server software, including API Gateway, Kubernetes ingress controller, NGINX App Protect, and software-based load balancing.

The bigger picture is that the web server market is set to grow at a CAGR of 18% to reach a total market size of $267.10 billion in 2018, which is up from just $75.03 billion in 2020. The growth of the industry is catalyzed by forces such as COVID and increased online business competition.

Cybercrime

One of the most important catalysts in my opinion is the exponential growth of cyber attacks directed towards businesses. Attacks grew 600% since the start of the pandemic, targeting individuals and teams being forced to work from home due to lockdowns. The global economic cost of cybercrime is set to grow to $10.5 trillion by 2025, up from $3 trillion in 2015. NSA chief Keith Alexander described this growth of cybercrime as “the greatest transfer of wealth in history.” Criminals are adapting their strategies to launch more targeted, frequent, and sophisticated attacks while businesses remain their primary targets. Damages caused by cyber attacks include financial losses, reputational damage, legal liability, business continuity problems, and more.

F5 is positioned nicely to respond to the growth of cyber attacks. One of its products is named Distributed Cloud Bot Defense and has successfully been integrated into Volterra’s product line according to an except found in the company’s annual report. This integration will allow customers to protect their servers from malicious and automated bot attacks as part of Volterra’s SaaS subscription model. It should be noted that automated cyber attacks account for over half of all hacking attempts on servers, thus the product can be seen as severely mitigating the dangers of financial loss and business disruption for its customers with a high growth potential as cybercrime increases in the future.

Global supply chain issues

Now that I’ve addressed the catalysts and potential upside for F5’s software business, it’s now time to address the global supply chain issues. I feel that these problems are temporary and that they will be resolved in time, so it does not make sense to me that the company’s share price should have plummeted by over 14% if F5’s hardware sales will inevitably recover, more so when one considers the company’s attractive pivot towards the software and security industries.

Instead of providing evidence that it is inevitable that the supply chain will be fixed eventually, which I believe the vast majority would agree with, I will instead present evidence that the supply chain is already in the process of recovering.

Peaked demand for durable goods

First, there is evidence that the demand for household durable goods has peaked in the US market, which will ease pressure on the supply chains. The demand for durable goods surged due to more people spending time at home during lockdowns and a swell in household savings.

Consumer demand for durable goods (Federal Reserve Bank of St. Louis)

A cursory glance at the demand of durable goods from the Federal Reserve Bank of St. Louis indicates that it reached its peak in March 2021.

Increased shipping capacity

While the amount of goods being shipped to the United States decreases, shipping capacity is on an upwards trend to further ease pressure on the global supply chain. The shipping market size this year is projected to reach $9.84 billion, up from $9.44 billion in 2021.

Yearly growth of shipping capacity (Statista)

In a report released by trade credit insurer Euler Hermes, the new containers are set to be fully operational near the end of this year, which will help alleviate bottlenecks. Other findings in the report included that $17 billion has been earmarked in the US for new port infrastructure and waterways to reduce port congestion.

So, as the demand for durable goods has reached its peak and total shipping capacity is increasing, this suggests to me that the supply chain problem is already in the process of improving. For this reason, I also believe that the market responded more to F5 reducing its revenue forecast than the underlying reason for why it was reduced in the first place.

Competitive Analysis

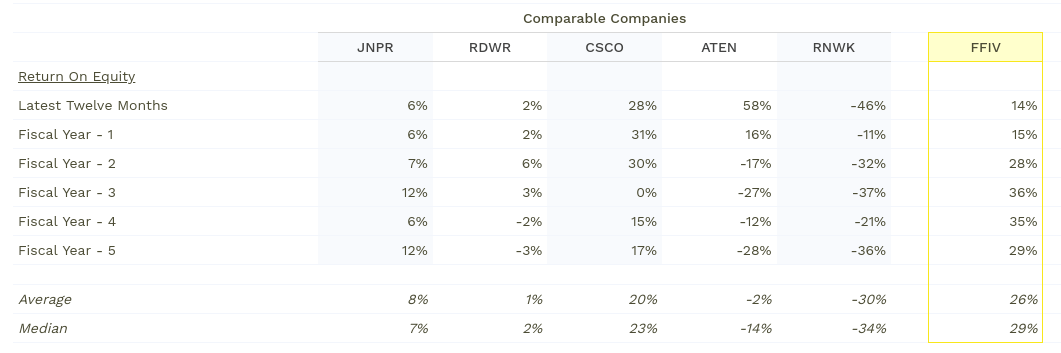

In this section I will analyze F5’s quantitative and qualitative strengths and weaknesses against its competitors. The companies I chose to measure the brand against include Juniper Networks (JNPR), Radware (RDWR), Cisco Systems (CSCO), A10 Networks (ATEN), and RealNetworks (RNWK).

Comparing the company’s ROE against its peers reveals that F5 has the highest ROE out of the selected companies with an average ROE of 26%, which is significantly higher than its main competitor Cisco’s ROE of 20%.

ROE Comparison (Author)

This means that the company is relatively more efficient at generating income and growth from its equity financing than its key competitor and significantly more than the other companies in this group that only have little or a negative return on equity.

It’s also worth discussing the technical advantages that F5 networks has over its competitors. The first comes from the ease of BIG-IP’s deployment that can be made in any environment: be it physical, virtual, or in the cloud. BIG-IP’s applications also give the company a significant leg up on the competition that allows operators to monitor and shape traffic more effectively. All of the applications are controlled from a single interface which makes the management and deployment of the software easier and faster.

Another advantage is that BIG-IP allows operators to consolidate multiple services into one, which allows F5 to save costs, also meaning that they are unlikely to be forced to use a competitor. Supported software includes traffic management, optimization, and security services.

Consolidation of F5 services (F5 Networks)

BIG-IP solutions are programmable, which allow operators to customize their software as they see fit. The result of programming their software reflects in real-time changes to application traffic and device configuration. The bottom line is that F5’s software has several competitive advantages that can provide its users with economies of scale from both a cost savings as well as an operational perspective.

Valuation

I’ll now explore how F5 is fundamentally undervalued by the drop in its share price through a 2-stage DCF model.

F5 has also consistently beaten analyst estimates for four straight years, which may give investors some assurance that the company is capable of delivering on the growth of its software business.

F5 Ltd Earning Estimates (Yahoo! Finance)

Here are my projections for F5’s revenue as the worst-case scenario, with revenues only growing at 6.69% per year, which is near the bottom of the company’s range in its most recent earnings report.

Note that all numbers in the below table are in millions, and the currency is in USD.

F5 Ltd DCF model (Author)

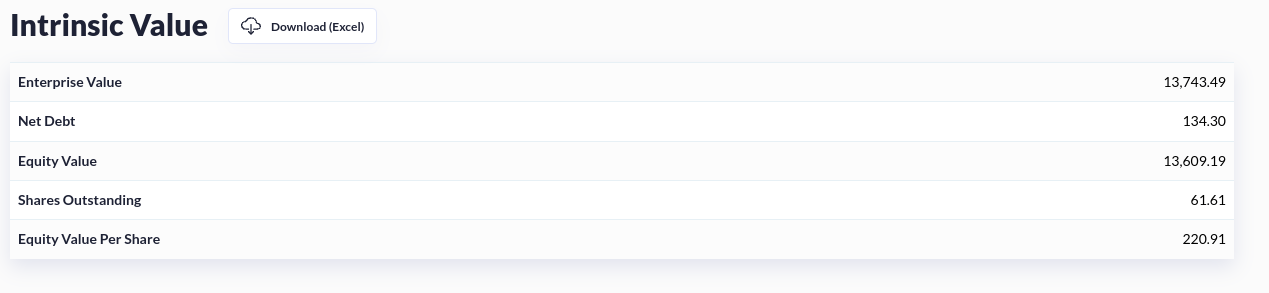

For the rest of the DCF model, the discount rate I am using here is 7%, which is a conservative estimate of the company’s WACC. The long-term growth rate is 3%, keeping in mind that 2.5% is the minimum a company that’s a going concern would need to grow at in order to keep above the 10-year average of inflation in the United States. These values give an equity value per share of $220.

Equity value per share (Author’s calculations)

Thus, even with a reduced projected revenues for this year and the next the company is still trading below its intrinsic value according to this method of valuation at the time of writing. Keep in mind that the DCF is very sensitive to assumptions made in the discount rate and the long-term growth rate, much more so than adjustments made to yearly revenues. On the other hand, the company has reportedly doubled its addressable market, so I still feel that this is a conservative estimate.

More caution should be taken using this method if one is serious about investing, including a full-stage DCF model that forecasts each item on the balance sheet and income statement individually. I chose the 2-stage DCF model to quickly illustrate the effects of changing the free cash flows and to give readers a starting point to see if creating a full model would be worth their investment of time and effort. The risks of relying on the 2-stage model are that I am only making assumptions about the company’s revenue growth, discount rate, and terminal growth rate. By themselves these assumptions are a good starting point to dive into further analysis but a more accurate valuation can be arrived at using a full DCF model. The risk of using a two-stage model is that it may produce inaccurate valuations above or below its intrinsic value.

Risks

In order to facilitate growth and to fund its acquisitions, F5 has continually issued equity which has diluted the company’s value to shareholders. If the company continues to fund its growth through equity, then investors who get on board now could see a dilution in their investment even if the company achieves its goals in the software space.

Another risk is that F5 has for a long time been a traditional hardware company. Senior management might not have the skills or industry experience required to pivot the company successfully towards software, and may end up losing valuable market share in the hardware space in the process.

Finally, although the company has made several strategic acquisitions, it is still largely theoretical how the company intends to synergize its BIG-IP software into the product lines of its acquired companies. There have been no specific announcements by the company that indicate its strategy in this regard, so it is difficult to assess how likely and risky such an integration would be.

Conclusion

F5 is a solid company with great earnings potential and I feel that the supply chain problems have discounted its long-term projected revenues irrationally. There is also evidence that the supply chain is coming together again while the firm has a lot of potential for the future. Value investors can then get on board this pick at a considerable discount.