Introduction

When casting an eye across the midstream industry, Delek Logistics Partners (NYSE:DKL) stands out for not only defying the wave of distribution reductions but actually increasing their distributions once again. Even though this small increase would normally indicate that their very high distribution yield of almost 13% is safe and sustainable, this is not necessarily the case as my previous article discussed. This article provides a follow-up analysis that takes a look at their subsequently released financial results and the impacts from their IDR elimination, plus a brief recap for new readers.

Executive Summary & Ratings

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that was assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Image Source: Author.

*There are significant short and medium-term uncertainties for the broader oil and gas industry. However, in the long term, they will certainly face a decline as the world moves away from fossil fuels.

**Whilst the oil and gas industry to which they service has high economic sensitivity, given the more stable nature of the midstream sub-industry, this was deemed to be average.

Detailed Analysis

![]()

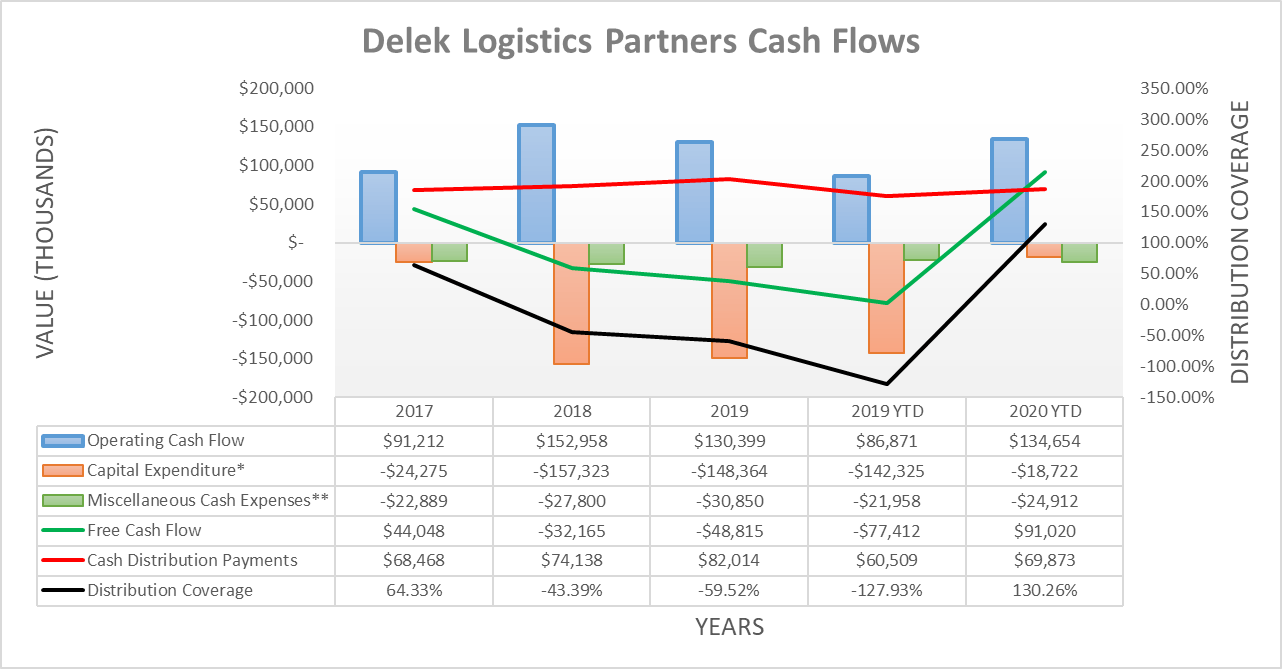

Image Source: Author

Instead of simply assessing distribution coverage through distributable cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and best captures the true impact to their financial position. The main difference between the two is that the former ignores the capital expenditure that relates to growth projects, which, given the very high capital intensity of their industry, can create a material difference.

Throughout 2017-2019, their distributions were routinely funded with debt, given their coverage averaged only a very weak negative 12.86%, primarily as a result of their relatively high capital expenditure. When the turmoil in 2020 rolled around, they reduced their capital expenditure, which helped boost their distribution coverage to 93.13% for the first half of 2020, and despite being a significant improvement, it nonetheless was still less than the minimal level for adequate coverage of 100%. During the third quarter of 2020, their capital expenditure essentially ground to a halt and only increased approximately $3m during the quarter, which allowed their distribution coverage for the first nine months of 2020 to soar to a strong 130.26%.

Whilst this undoubtedly sounds very promising for unitholders, the impacts of eliminating their IDRs should also be considered. The additional units issued under these terms have pushed their latest outstanding unit count to 43,433,239, which is a considerably large increase versus their previous 29,433,239 outstanding unit count at the end of the second quarter of 2020. This means that their current quarterly distribution of $0.905 per unit should cost them $157m per annum.

Their ability to adequately cover these distribution payments with free cash flow going forwards will largely depend upon their future capital expenditure. However, it is currently too early for management to provide guidance for 2021. During 2018-2019, their operating cash flow was only $153m and $130m, respectively, and whilst their annualized first nine months of 2020 was considerably higher at approximately $180m, this too only leaves a thin margin for capital expenditure.

Their distribution coverage will hopefully continue strengthening in the future, but at the moment, it was still deemed to be weak in order to remain conservative until more time has elapsed with more information coming to light. This naturally means that reviewing their capital structure, leverage, and liquidity is especially important.

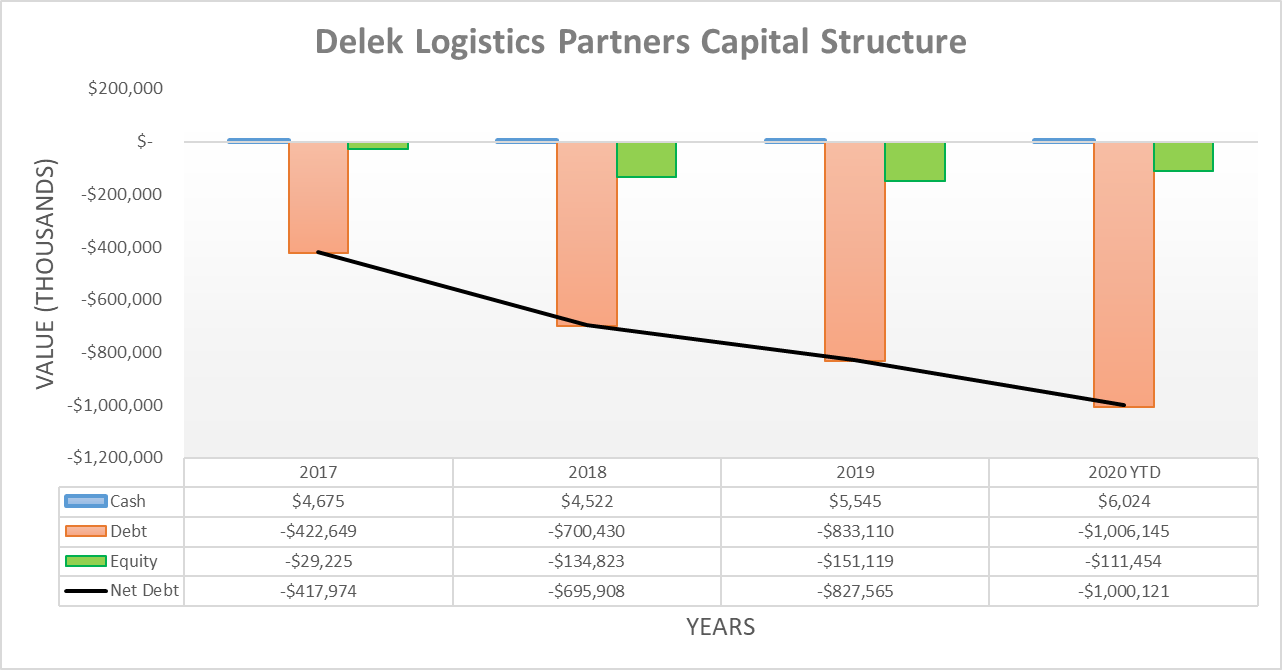

Image Source: Author.

Following years of soaring net debt from debt-funded distributions, their capital structure only saw their net debt expand slightly during the third quarter of 2020 with it increasing slightly from $979m to $1b. This was simply due to the $45m one-off payment to eliminate their IDRs more than counteracting their free cash flow, and whilst higher net debt is not ideal, given it was only very small, it should not have materially changed their leverage.

![]()

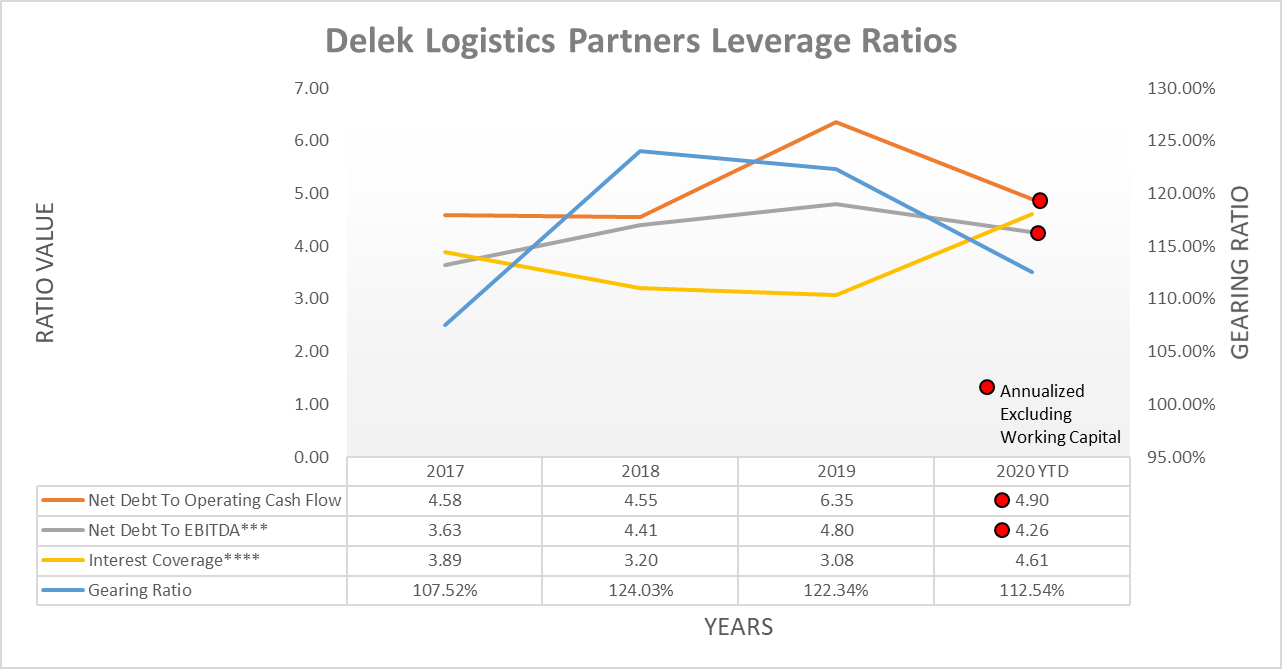

Image Source: Author.

Thankfully, their leverage slightly improved during the third quarter of 2020 despite their slightly higher net debt, thanks to their annualized 2020 EBITDA increasing from $220m to $235m as per my calculations. It should be remembered that their net debt to EBITDA of 4.26 still sits materially above the threshold for high leverage of 3.50, and thus, their situation has not fundamentally improved to a material extent. If they can continue generating free cash flow after distribution payments in the quarters ahead, this should improve, which once again will depend on their capital expenditure. At the moment, this leverage does not pose any danger to their ability to remain a going concern and only a slight risk to their distributions, providing that their liquidity remains adequate.

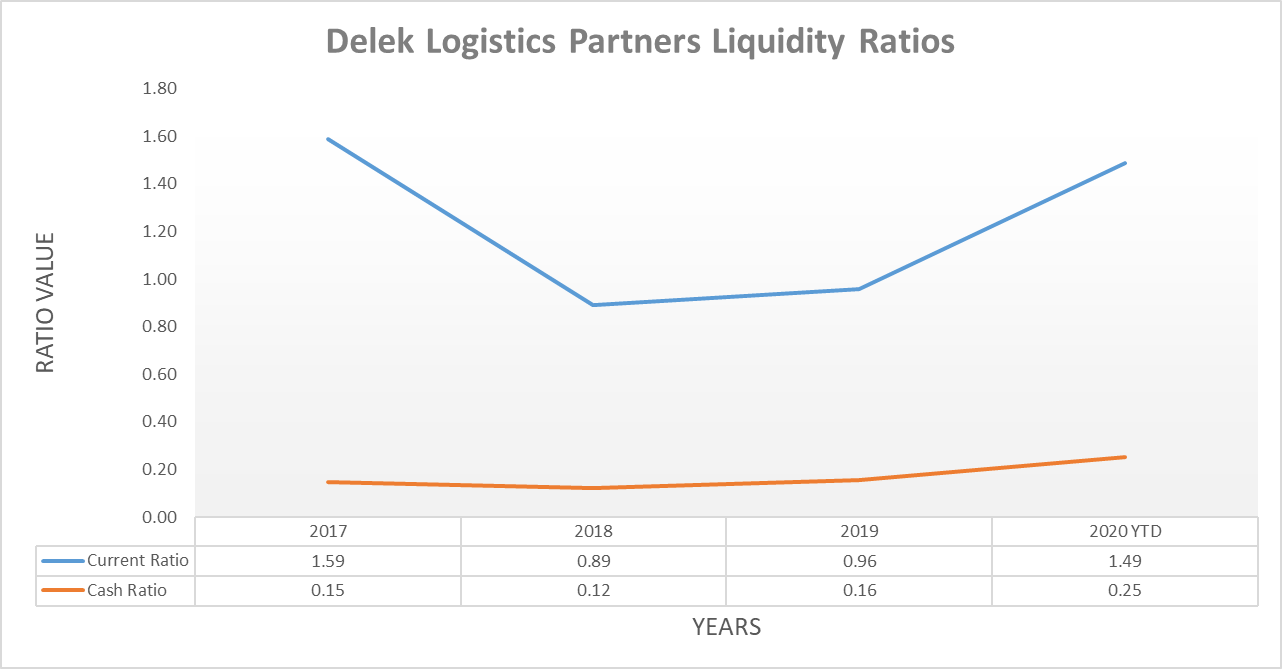

Image Source: Author.

Arguably, their most undesirable aspect remains their liquidity, which has rather mixed results that make it difficult to decide between an adequate and weak rating. On one hand, their respective current and cash ratios of 1.49 and 0.25 are easily adequate, even though they have deteriorated materially from 2.42 and 0.90, respectively, during the third quarter of 2020.

Whereas, on the other hand, their main weakness stems from their credit facility only having $89m available undrawn out of a total balance of $850m. This ultimately keeps their distributions risky and further highlights the importance of their future capital expenditure direction since the importance of generating free cash flow after distribution payments is now critical. Thankfully, their other debt is comprised of senior notes that do not mature until 2025 and, thus, provides them with ample time to refinance if required.

Conclusion

Even though their unitholders are likely rejoicing at the fact that they are once again getting an even higher distribution, until more time elapses, these remain risky, given their questionable coverage and liquidity. Given this situation, I believe that maintaining my neutral rating is appropriate for the time being.

Notes: Unless specified otherwise, all figures in this article were taken from Delek Logistics Partners’ Q3 2020 10-Q, 2019 10-K and 2017 10-K SEC Filings, all calculated figures were performed by the author.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.