knape/E+ via Getty Images

Written by Nick Ackerman, co-produced by Stanford Chemist

BlackRock Health Sciences Trust II (BMEZ) has been having a tough time performing. That is despite its exposure to healthcare as it is invested heavier in the healthcare innovation/growth space. It also has private holdings that also can increase its risk level. The losses had been accelerating as of late in its underlying holdings but I view it as being more attractively priced.

Over the last year, the fund has been down nearly 26% on a total NAV return basis. The losses accelerated significantly even more recently, with the broader markets also participating.

Over the last few months, it was mostly the innovation/tech space that was difficult. Below we can see the comparison between BMEZ and its predecessor, BlackRock Health Sciences Trust (BME). BME holds the more traditional healthcare names. We can see how much better BME has been holding up relative to BMEZ. However, losses have still occurred there too.

Ycharts

BMEZ’s discount has been widening, and the overall decline could provide a fairly attractive entry into this fund. That being said, it remains a riskier holding and not for conservative investors. After the poor performance in 2021, it isn’t exactly going to be the most encouraging investment either, which means that the discount could linger for quite some time. There weren’t a lot of places that provided for losses in 2021, but BMEZ was one.

The Basics

- 1-Year Z-score: 0.85

- Discount: 3.55%

- Distribution Yield: 8%

- Expense Ratio: 1.31%

- Leverage: N/A

- Managed Assets: $2.511 billion

- Structure: Term (anticipated liquidation January 29th, 2032)

BMEZ “seeks to invest up to 25% in private companies.” It intends on doing this through “at least 80% of its total assets in equity securities of companies principally engaged in the health sciences group of industries and equity derivatives with exposure to the health sciences group of industries.” With this, it also utilizes an options strategy.

It last reported 21.92% of the portfolio being overwritten. This is below its target range of 30% to 40% and would indicate a bullish stance. In hindsight, if they were more aggressive in this strategy, it could have offset a bit more of the losses. At this point, keeping a lower percentage overwritten seems appropriate, so positions aren’t called away during a rebound. Of course, that is if there is a rebound and to how aggressive the rebound might be.

The fund has a term structure that will see the fund potentially liquidated around Jan. 29, 2032. They may switch to a perpetual fund after a tender offer for 100% of outstanding shares at 100% of NAV. If there are still $200 million in total net assets, the board can convert to a perpetual structure. After that point, there will be no more support to keep the fund to its NAV.

Even if the fund finished flat from here, at least the 8.43% discount could be harvested. It isn’t realistic to believe that there won’t be a change in the fund’s price and NAV over the next ten years. It’s something to continue to monitor and can be taken advantage of closer to the fund’s termination date.

The term structure is designed to keep the fund from trading at a perpetual discount. If the fund performs well, the fund would likely continue to operate. After the fund’s launch, it made some significant moves that certainly helped give it a jump start towards that goal.

Performance – Disappointing So Far

The fund seemed as though it had a lot of potentials when it first began. It was one of the best-performing funds in 2020. Although CEFs are just a function of their underlying investments – they are a wrapper for investments and not an asset class themselves.

The inception date of January 29th, 2020, just happened to be a great time to launch a fund of this type. The COVID pandemic hit, and they could take advantage of depressed prices to build out their portfolio. In addition to that, we also know that the innovation space was exactly what worked in 2020.

Since then, it has been a slow grind lower. 2021 delivered a total return of -8.31% and a total NAV return of -5.76%.

With the losses accelerated into 2022, BMEZ wouldn’t necessarily look like a promising investment. However, I would take the other side and say that now is an even better time to invest. I’m not sure when the sell-off will let up or if we are just getting started with it. What I do know is that the fund’s discount is looking fairly attractive, and the sell-off has definitely made it a lot cheaper than it had been.

Launching in 2020 means, we only have a couple of years’ worth of data to look back on. That being said, we see that the fund’s discount is around its average. It snapped back quickly from the latest dip. Still, the overall dip is presenting an attractive opportunity on its own.

CEFs tend to sell off harder than other investments due to their discount/premium mechanics. They are also owned mainly by retail investors, so they generally shoot first and ask questions later. That dries up the buyers for these funds, which can fall significantly below their NAV levels. For those of us that invest in CEFs, we generally see this as an opportunity to exploit.

Distribution – 8% Is Attractive, But Be Cautious

While the fund is pretty attractively valued now – a higher distribution rate is appealing – I’d have to be a bit somber here. It will not be sustainable if we don’t start getting a rebound.

Currently, the distribution rate comes to 8%. Higher yields are great, but we start running into sustainability issuers the higher we go. The NAV rate comes to 7.72%.

Last year we saw a small special distribution from the fund of $0.0621. This came as they realized many of the gains that they carried over from 2021. It wasn’t a function of actually good performance in 2021; as we touched on above, they produced losses for the year. That strong 2020 performance was exactly why we saw a boost to the distribution in 2021 too.

BMEZ covers its distribution through capital gains. It earns no net investment income. NII is simply the total income minus the expenses. Since the fund is focused on innovation and private companies, it doesn’t collect a lot of dividends or interest.

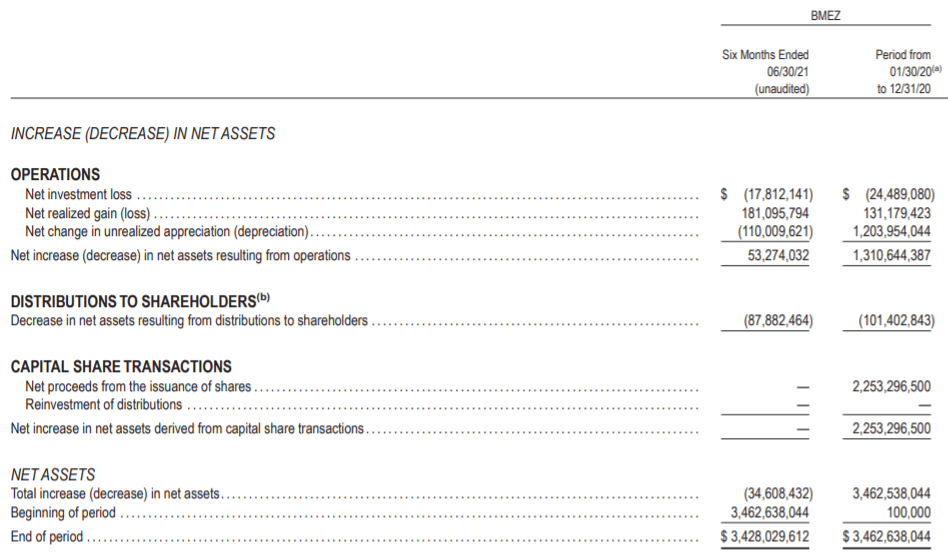

BMEZ Semi-Annual Report (BlackRock)

Now that the gains are drying up, we could see a distribution cut. All this being said, it will remain one of the only ways to continue to get paid until a rebound. The fund will ultimately continue to pay at least something due to the CEF structure.

BMEZ’s Portfolio

The average market cap of the underlying investments in its portfolio comes to $21.724 million. The average market cap of the underlying holdings for BME comes to $167 million. That just shows that BMEZ is investing in a lot smaller companies relative to BME. Smaller companies tend to be riskier, which is the case with BMEZ. That’s what makes it a riskier CEF in the first place. Then we have the fund’s private holdings as well.

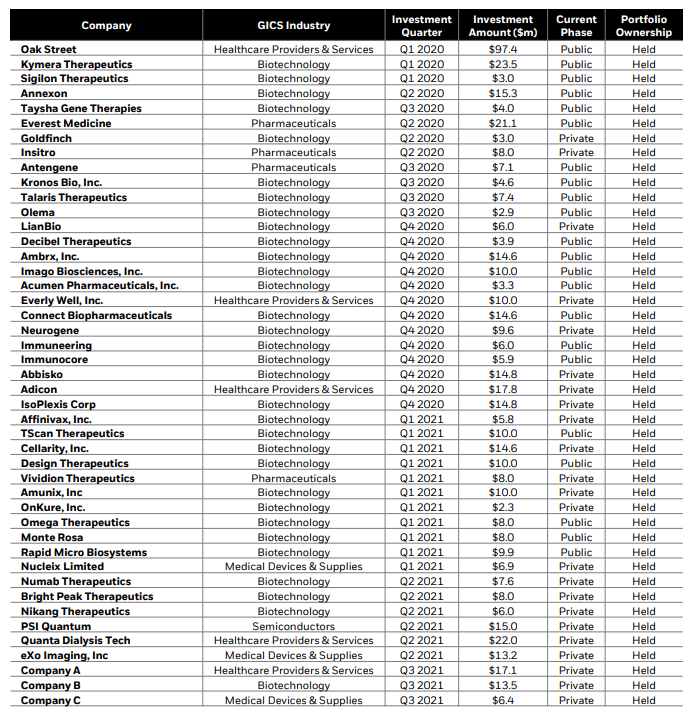

At the end of Q3 2021, most of their private investments have been oriented towards biotech stocks. No surprise, this is one of the worst areas of the market – that’s why BMEZ has performed so poorly.

Fortunately for us, many of the private holdings BMEZ had invested in have gone public now. That means we can take a look at how some of them have fared.

BMEZ Private Holdings (BlackRock)

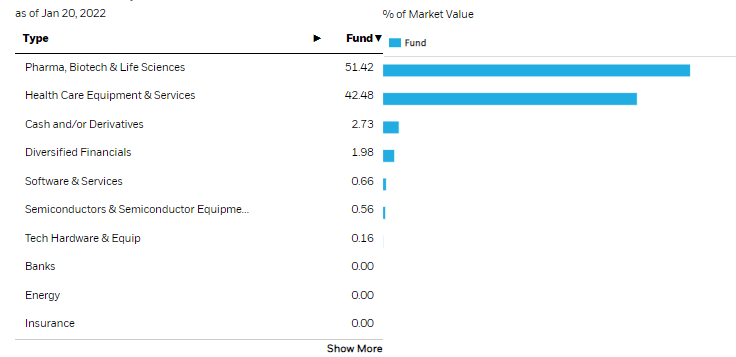

As of January 20th, 2022, “pharma, biotech and life sciences” is the largest sector allocation of the fund. Which just reiterates what we were seeing in its private holdings.

BMEZ Sector Allocations (BlackRock)

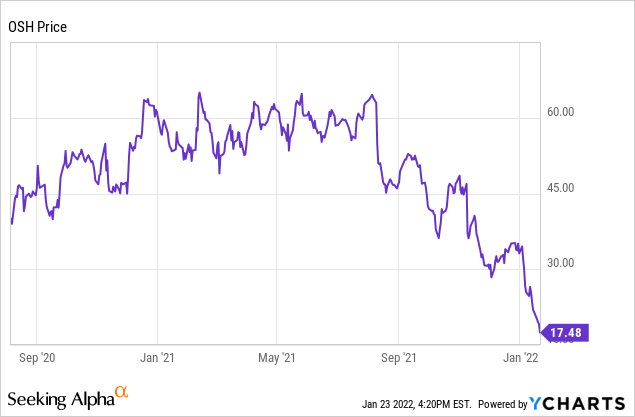

One of the fund’s largest private holdings was Oak Street (OSH). This stock was a 2020 darling when it went public. The IPO price was $21, and it quickly shot up after its IPO. A large decline that began in August 2021 has sent the shares back below this price at below $18 now.

Ycharts

Let’s look at Kymera Therapeutics (KYMR). This was another fairly significant investment for BMEZ in the biotech space. This stock went public in August 2020 at $20 per share. We once again saw it open sharply higher. Then towards the end of 2020, it started to go parabolic. Since then, the stock has held above its IPO price but has been cut in more than half from its peak. Losses in the share price accelerated in the last few weeks.

Ycharts

Suffice it to say, a lot of the other charts are similar. Sigilon Therapeutics (SGTX), Annexon (ANNX) and Taysha Gene Therapies (TSHA) all went public at various times. SGTX has to be one of the worst, though; it is now a penny stock. ANNX and TSHA are heading that way.

Ycharts

Many of these stocks seem as though it could be hard to recover these losses as well. While the private investments of BMEZ make it more unique and interesting, it also shows how erratic, volatile and risky these things are.

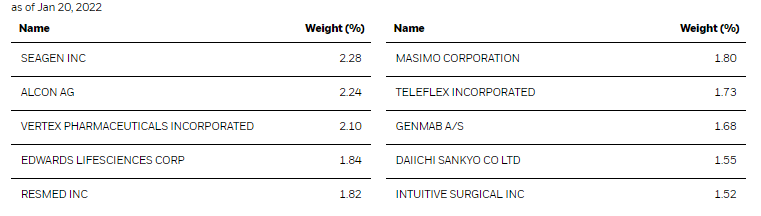

BMEZ Top Ten (BlackRock)

Though to be fair, the private holdings that more recently went public in 2020 aren’t the only stocks struggling. BMEZ’s top ten include several names that have been around for years. Of the top five, only Alcon (ALC) doesn’t have more than 10+ years of being publicly traded. Here is a look at the performance of BMEZ’s top 5 positions.

Ycharts

It isn’t surprising to see why BMEZ has been having a tough go with performance such as this. A lot of what the fund invests in is just not performing. Positions providing results for shareholders are relatively few in this fund. I believe some of the private holdings at this point are a lost cause; however, others here seem just to be providing an attractive entry point. That’s what makes BMEZ more interesting too.

Conclusion

BMEZ has been having a tough time since its early successes. Those successes translated into higher distribution for shareholders. However, that distribution seems to be under pressure now, with assets deflating rapidly for the fund. Most of the fund’s private and public holdings all have the same trajectory – that is sharply higher then a rapid decline. The declines picked up more momentum as we head into 2022. It has been rebounding strongly, and I’m not sure if this is a turnaround or we’ll head lower. However, I do believe that if one can handle the higher risks here, it is a tempting offer being served up.