JamesBrey/iStock via Getty Images

Introduction

After significantly reducing their distributions following the onset of the Covid-19 pandemic, the start of 2021 saw USD Partners (USDP) put their distributions back in growth mode, as my previous article discussed. Seeing as nearly ten months have passed since this last detailed analysis, it feels timely to provide a refreshed analysis covering their financial performance during 2021 and the outlook for the future, which sees that investors can grab three more distribution hikes for 2022, which make for a no-stress high near 9% yield.

Executive Summary & Ratings

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Author

*Instead of simply assessing distribution coverage through distributable cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and also best captures the true impact upon their financial position.

Detailed Analysis

Author

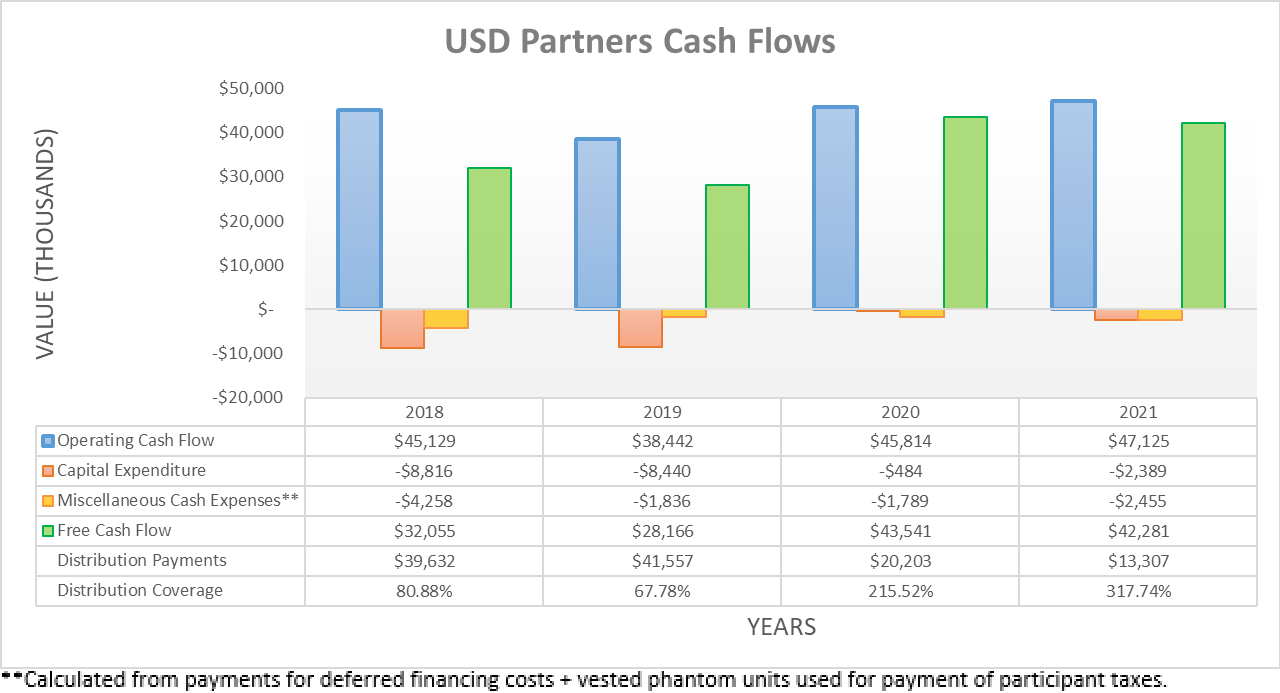

They wrapped up another steady year throughout 2021 with their operating cash flow coming in at $47.1m, which was a handy increase of 2.86% year-on-year versus their previous result of $45.8m during 2020. Even if removing the temporary working capital draw that slightly benefitted their results during 2021, their underlying operating cash flow was still $44.8m, which is essentially within a mere $100,000 of their previous equivalent result of $44.7m during 2020. When combined with their only very low capital expenditure and miscellaneous cash expenses, their free cash flow ended 2021 at $42.3m and thus was ample to provide very strong coverage of 317.74% to their distribution payments of $13.3m, which appears set to continue throughout 2022 given their positive language, as per the commentary from management included below.

”… given the inventory levels I just described, our producers, our potential customers in Canada are experiencing some of the best netbacks that they have ever experienced.”

“So consequently, in 2022, our expectation is, we will see incremental production or supply growth relative to 2021.”

“So obviously, we’re very encouraged about 2022 and what’s happening. We always take a more conservative view in terms of our distribution policy, but we’re very encouraged about it. Our coverages is good and we want to try to continue to review that distribution policy and continue to grow as we can.”

-USD Partners Q4 2021 Conference Call.

Even though their management does not provide any exact guidance for 2022 or previous years as a matter of fact, their commentary seemingly implies that 2022 should be a positive year, albeit rather uneventful. Whilst they mention reviewing their distribution policy, thus far they nevertheless appear to be sitting tight with their current slow pace of growth, as per the commentary from management included below.

“Accordingly, management intends to recommend to the Board of Directors of its general partner to remain on its current distribution growth trajectory of increasing its quarterly cash distribution per unit by an additional quarter of a cent per quarter for the first, second, third and fourth quarters in 2022.”

-USD Partners Q4 2021 Conference Call (previously linked).

Even though their ample free cash flow could easily see their distributions doubled overnight, it seems that management is keeping with their conservative slow pace of growth but thankfully, this still adds up across the year, despite their forecast quarter of a cent increases not sounding too impressive on the surface. Since their first quarterly distribution increase for 2022 was to $0.121 per unit, their remaining three quarterly distributions should be $0.1235, $0.126 and $0.1285 per unit for a total of $0.499 per unit across 2022. When viewed against their current unit price of only $5.69, this sees a high distribution yield of near 9% with no stress given their ample free cash flow.

Author

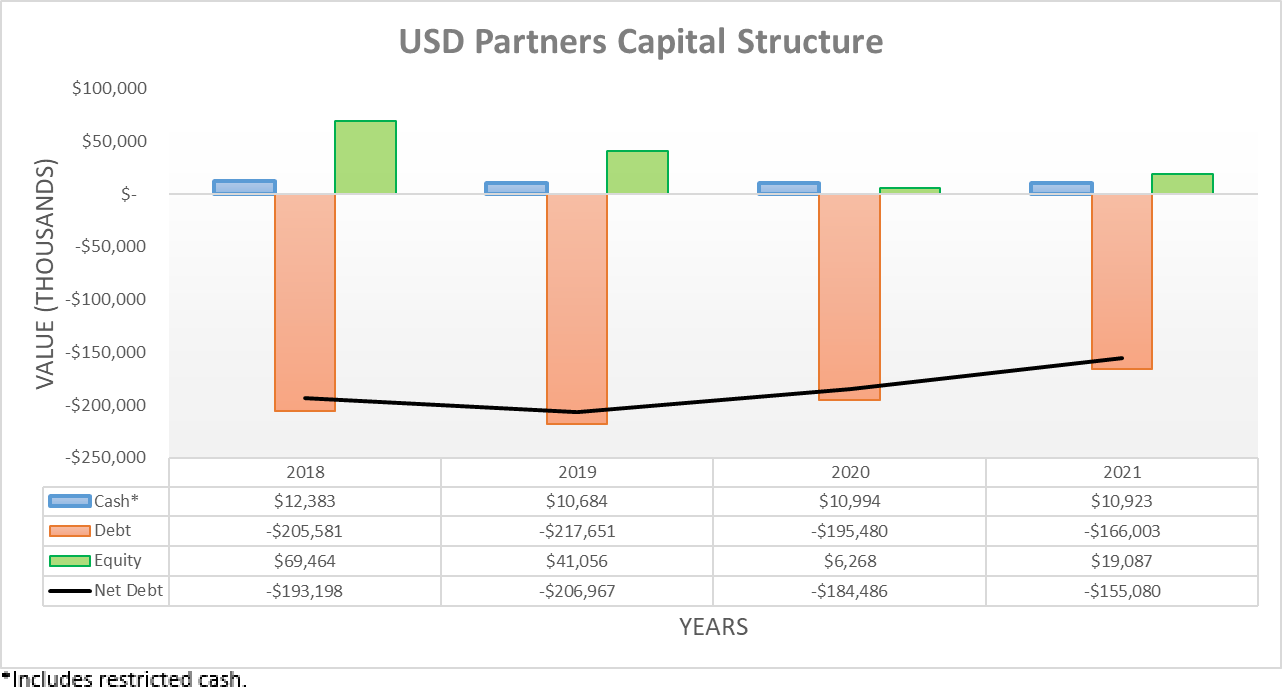

Thanks to their continued strong free cash flow throughout 2021 and relatively small distributions, it was not surprising to see their net debt continue trending lower to finish the year at $155.1m, which represents a solid decrease of 15.94% year-on-year versus its previous level of $184.5m at the end of 2020. Given their forecast continued slow pace of distribution growth during 2022, their net debt should see another comparable decrease by the end of the year, thereby pushing down their leverage.

Author

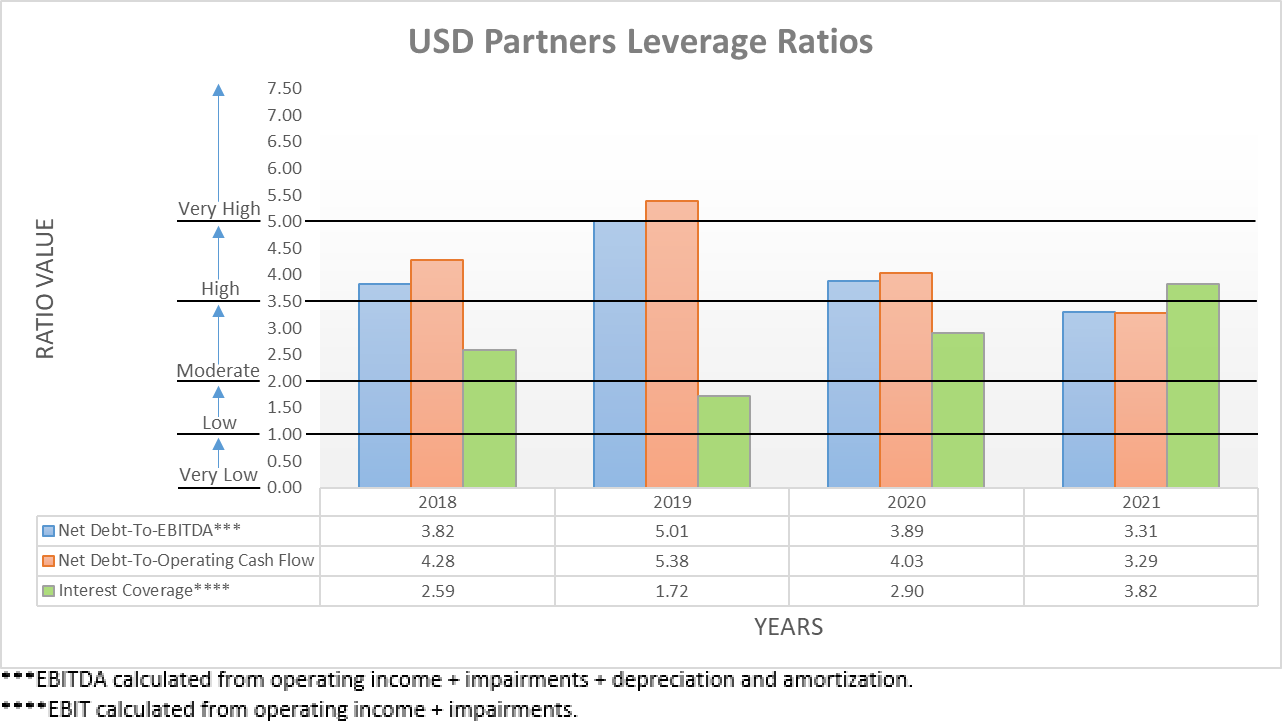

Following their lower net debt, it was not surprising to see their leverage also trended lower in tandem with their respective net debt-to-EBITDA and net debt-to-operating cash flow of 3.31 and 3.29 both now sitting under 3.51 and thus only within the moderate territory. This marks a solid improvement versus the end of 2020 when their respective results were 3.89 and 4.03, thereby clearly sitting within the high territory of between 3.51 and 5.00. Meanwhile, their interest coverage improved as well to 3.82 versus its previous result of 2.90 at the end of 2020. Since all of these leverage ratios should see comparably sized improvements during 2022 as their net debt trends lower, it further enhances the prospects for management to boost their distribution growth rate higher in 2023.

Author

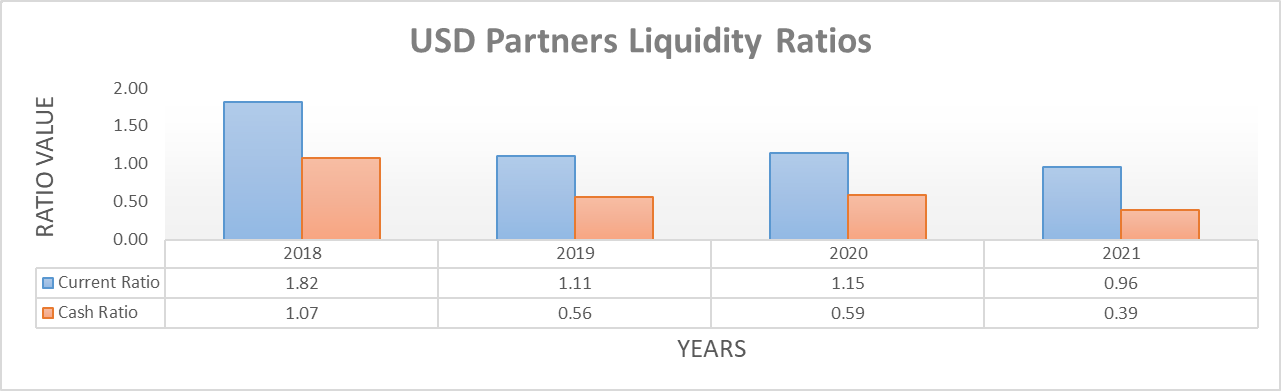

Even though their respective current and cash ratios decreased to 0.96 and 0.39 versus their previous respective results of 1.15 and 0.59 at the end of 2020, thankfully, their liquidity remains strong. Even more importantly, they refinanced their credit facility during 2021 that as a reminder, houses the entirety of their debt, thereby extending its maturity from November 2022 to one year later in November 2023. This also saw its borrowing capacity reduced to $275m versus its previous level of $385m, which only leaves $109m remaining to be drawn but given the outlook for their deleveraging during 2022, this should not be required and will continue to expand as they reduce their net debt.

Conclusion

Even though it would have been preferable to see more substantial distribution growth for 2022 given their ample free cash flow, at least their slow pace will see their financial position strengthen, thereby lowering risks and hopefully lining up 2023 to see higher unitholder returns. Thanks to the prospects of collecting a no-stress high distribution yield of near 9%, their units have earned a place within my personal portfolio and thus as a result, I now believe that upgrading my rating to a strong buy is appropriate. Whilst I am not necessarily advocating for a set and forget attitude when it comes to investing but in this situation, it almost seems warranted given their steady financial performance and uneventful outlook, which means that unless something unexpected happens later in the year, this will be my only update for 2022.

Notes: Unless specified otherwise, all figures in this article were taken from USD Partners’ SEC filings, all calculated figures were performed by the author.