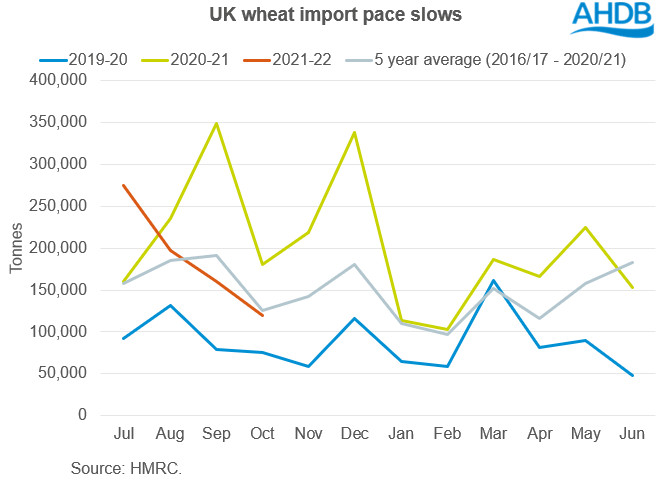

HMRC have released their latest trade data to October. These figures show UK wheat imports (inc. durum) continuing to slow. At 119.3Kt, this is below the previous 5-year average (2016/17 – 2020/21) of 125.4Kt for October wheat imports.

This brings total wheat imports for this season (July to October) down 19% from last season.

Will this slow pace continue? Well, the discount of UK feed wheat futures (May-22) to Paris milling wheat futures (May-22) has started to narrow. At the start of November, this was reported by Anthony as c.£17.24/t. This then widened to £19.25/t on 15 November. As at yesterday, this had tapered to c.£11.59/t. While there may be different reasons playing into this, including exchange rate changes and reduced concerns around EU wheat availability, this could mean we start to see UK pricing move away from export competitiveness.

However, challenges remain for sea freight, which may be impacting on slow imports. Though domestic haulage issues may mean some regions could see sea freight if more readily available.

Why is this important?

The UK wheat supply and demand balance is tight this season. With opening stocks the lowest this century, this presents a picture with not much room to give.

On Friday, we saw Defra’s final estimate of the 2021 UK wheat crop at 13.99Mt. This is down slightly from 14.02Mt estimated in October, tightening availability slightly further.

Should UK availability tighten further, and demand remain strong, we may see UK prices remain firm. Especially in areas where the basis is already increasing at a faster pace, e.g. Northern and Scottish ex-farm wheat.