The Bank of England’s proprietary trading review came out this week, but it has largely gone under the radar. That’s a shame because among its findings is this (our emphasis):

There is evidence that other activities falling within the statutory definition of proprietary trading are substantial for some firms, but these activities arise in the context of the wider business needs of the firms concerned. Many firms, especially larger firms, continue to serve their clients through market making and related activities. Firms’ liquid asset buffers (LABs) hold material amounts of financial instruments, although these are largely cash, central bank reserves, or low risk government bonds, and interest rate risk in the LAB is often largely hedged. Furthermore, firms hedge the risks arising from serving clients in both trading and banking books through own-account positions in financial instruments and commodities.

The Bank’s conclusion is that this sort of activity is AOK because new capital and liquidity requirements for banks, as well as tougher internal controls, have diminished most associated systemic risks.

But to those in the know, especially with respect to how traders themselves view market-making risk, that feels like a regulatory a cop out sitting in plain sight.

In the exact same report the BoE also finds that there is evidence of substantial activities falling “within the statutory definition of proprietary trading” precisely under the market-making name. It goes on to disclose that it remains hard to separate market making from proprietary trading, since both activities involve holding positions for the bank’s own trading account, with the only real distinction being intent.

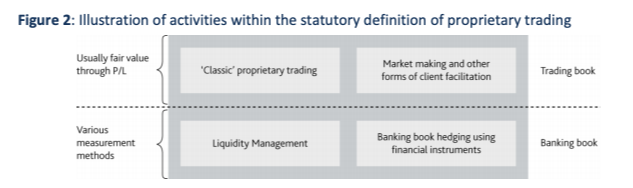

In case you’re confused about what falls under that statutory definition of proprietary trading, here’s a convenient diagram from the Bank:

Worryingly, the BoE says firms’ hedging activities and liquidity investments (the fuel that powers the market-making desk) are substantial and have not declined even as market risk has. But, again, the BoE is not worried because hedging is supposed to reduce risk — and there’s some evidence from both regulatory and firms’ own risk measures that they do, they say.

Even so, (and do consider the impact negative oil prices may have on airlines that hedged their fuel costs or the US Treasuries debacle in March, 2020), the BoE admits that if these hedges that usually offer a net benefit in risk reduction were to go awry, the “impact on the firm could be material”.

So, yet another mixed signal.

Liquid asset buffers as a place of risk

It’s not just market-making desks that absorbs so much of the proprietary trading risk these days. Another unexpected area of position-taking — at least to those not familiar with such things as the Repo 105 saga during the global financial crisis and/or the MF Global collapse — are banks’ liquidity management divisions, or as the Bank calls them areas focused on “investment of liquidity and other treasury functions”.

The risk relates to the liquid asset buffers (LABs) — stocks of highly liquid financial instruments — that banks are obliged to maintain in order to be able to meet payments as they fall due. Usually they consist of cash and central bank reserves. But other times, they also consist of so-called high quality securities. It’s in the classification of what qualifies as a high-quality security that the risk lies.

The Bank is right to point out that much of the MF Global-type risk (which famously both broke segregation fund rules and invested in sovereign bonds of dubious quality, speculatively) has been mitigated by liquidity coverage ratio rules and the incoming net stable funding ratio.

Nonetheless, institutions that regularly find themselves with excess liquidity need to park it somewhere, and when those funds exceed minimum coverage criteria the temptation is to look for cheaper areas of investment. This can involve risk. But as the Bank notes, because LABs are not recorded in a bank’s trading account they don’t necessarily get accounted for as prop trading.

This matters when you consider that even high quality bonds can occasionally (as in March, 2020) be subject to significant and persistent price falls.

Bear all that in mind as banks and the non-banks they service rush to adopt stablecoin crypto offerings, which are even more reliant on excess liquidity buffers.

There’s much more in the report, so do have a read. But one notable absence regards any reference to bank internalisation practices. There’s a section about the JP Morgan Whale, which in theory touches on the issue, but this is not put into any broader context with respect to wider internalisation practices, Delta-one trading and index arbitrage (especially the ETF sort).

What we are told is that some classic prop trading activities have clearly been transferred to the non-bank financial sector, often by hedge funds and principal trading firms (PTFs). While this has in some ways expunged a lot of the market-making position risk from banks, it has also made banks increasingly dependent on PTFs as short-term liquidity providers.

The Bank agrees this exposes the market to new risks, including flash crash events and “risks arising from the concentration of liquidity and service provision in a smaller number of players”.

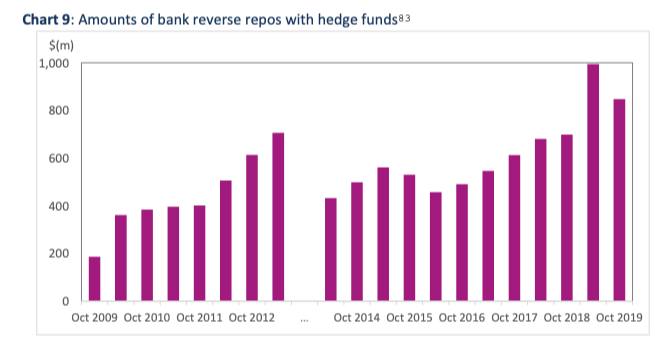

Equally, banks are now even more engaged with hedge funds via reverse repos — potentially exposing them to new types of counterparty risks.

An interesting and important point is that the new structure also seems to impede the closure of arbitrage gaps in many markets because hedge funds won’t engage in arb trades unless the pay offs are really worth their while. As the Bank puts it: “arbitrages have to be more profitable before they are exploited than was the case pre-crisis.”

What this implies, by our reading, is that the abolition of clearly defined prop trading at banks have in some ways made the market less efficient. They have both transferred the responsibility of arbitrage to hedge funds which are far less financially equipped (due to their cost of funding being higher than those of banks) to engage in the opportunities — making prices less efficient and more gappy — while also obscuring the true scale of prop trading that still goes on at banks.

The old prop desks were risky. Undoubtedly. But at least they were clearly defined. Furthermore, within the right regulatory environment, traders sitting within them could be incentivised or risk-managed in clear and transparent ways. Dare we say it, the report implies that the market as a whole may have benefited from the presence of such traders. The new structure is not a panacea.

Related links:

Proprietary trading review – BoE