Maddie Meyer/Getty Images News

Of the smaller restaurant chains in the US, one of the most iconic has got to be Cheesecake Factory Inc. (NASDAQ:CAKE). Despite suffering from the COVID-19 pandemic, the company has returned to growth and surpassed the kind of performance that it had achieved in years prior. Some of this was due to the firm’s decision to acquire North Italia and Fox Restaurant Concepts Back in 2019 for $308 million, plus up to another $57 million over time, but growth is growth nonetheless. With management setting its sights on some of its more attractive properties, with the end goal of replicating that success, and with shares of the business trading at low levels, it may not be a bad prospect to consider at this time.

At the end of the day, Cheesecake Factory is not a prime prospect by any means. But given recent performance, it’s not unthinkable that some upside could be on the table.

Improvements At The Cheesecake Factory

It has been a long time since I have last written about Cheesecake Factory. My only other article on the company was published back in April of 2015. At that time, I indicated that the company was starting to see something of a growth spurt. However, shares at that time looked rather pricey and my recommendation for investors who were value-oriented was to avoid the company until it became more attractive. Since then, things have not gone particularly well for the business. Despite seeing some nice revenue growth, much of it driven by the aforementioned acquisition, shares have generated a loss for investors of about 18%. That’s at a time when the S&P 500 more than doubled, climbing by 108.8%.

Author – SEC EDGAR Data

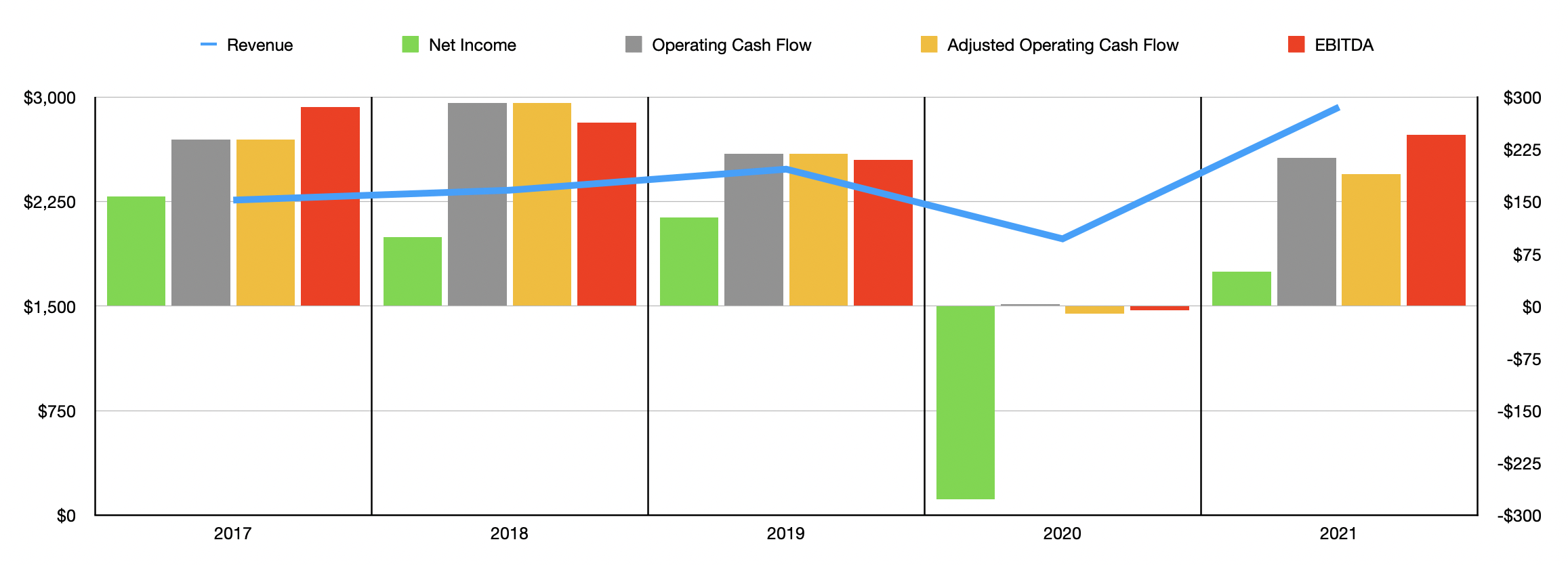

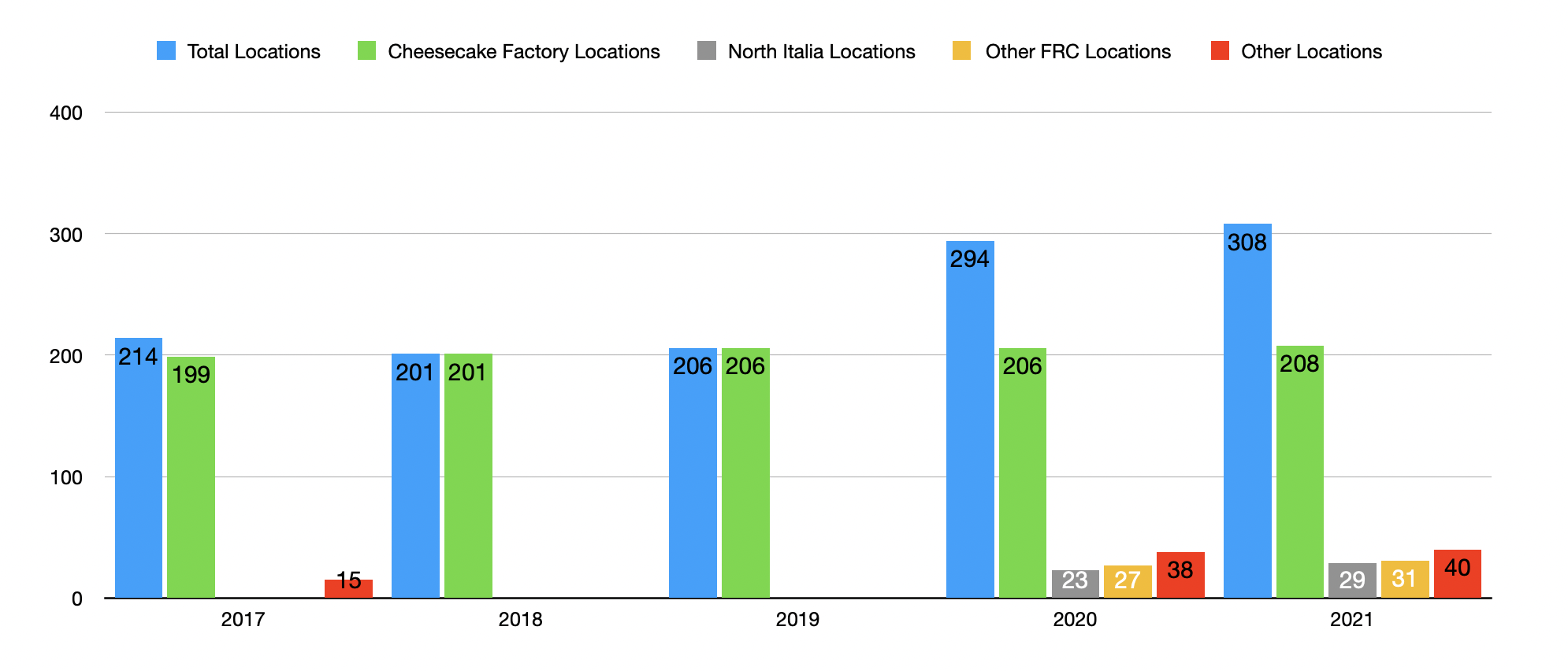

You would think that fundamental performance of a business that has experienced that kind of disparity relative to the market would be awful. But I wouldn’t say that’s the case. Revenue expanded consistently between 2017 and 2019, climbing from $2.26 billion to $2.48 billion. The COVID-19 pandemic hit the company hard, sending sales down to a more modest $1.98 billion before the company rebounded in 2021 with sales of $2.93 billion. In addition to adding 100 restaurants to its portfolio, through the end of 2021, thanks to the acquisition mention and because of a continued buildout of locations associated with those brands, the company has also seen the number of Cheesecake Factory locations increase modestly, rising from 199 in 2017 to 208 in 2021.

Author – SEC EDGAR Data

Although revenue growth has been generally positive, profitability has been less consistent. Between 2017 and 2019, net income at the company ranged from a low point of $99 million to a high point of $157.4 million, with no clear trend from year to year. The firm then lost $277.1 million in 2020 before recovering some of this to generate a small profit of $49.1 million last year. Other profitability metrics have also had a bumpy ride. Operating cash flow remained between $218.8 million and $291.3 million in the three years ending in 2019. Cash flow then dropped to just $2.9 million in 2020 before recovering to $213 million last year. A similar trend could be seen with EBITDA, with that metric ultimately recovering as well, climbing back up to $246.3 million in 2021.

The Cheesecake Factory

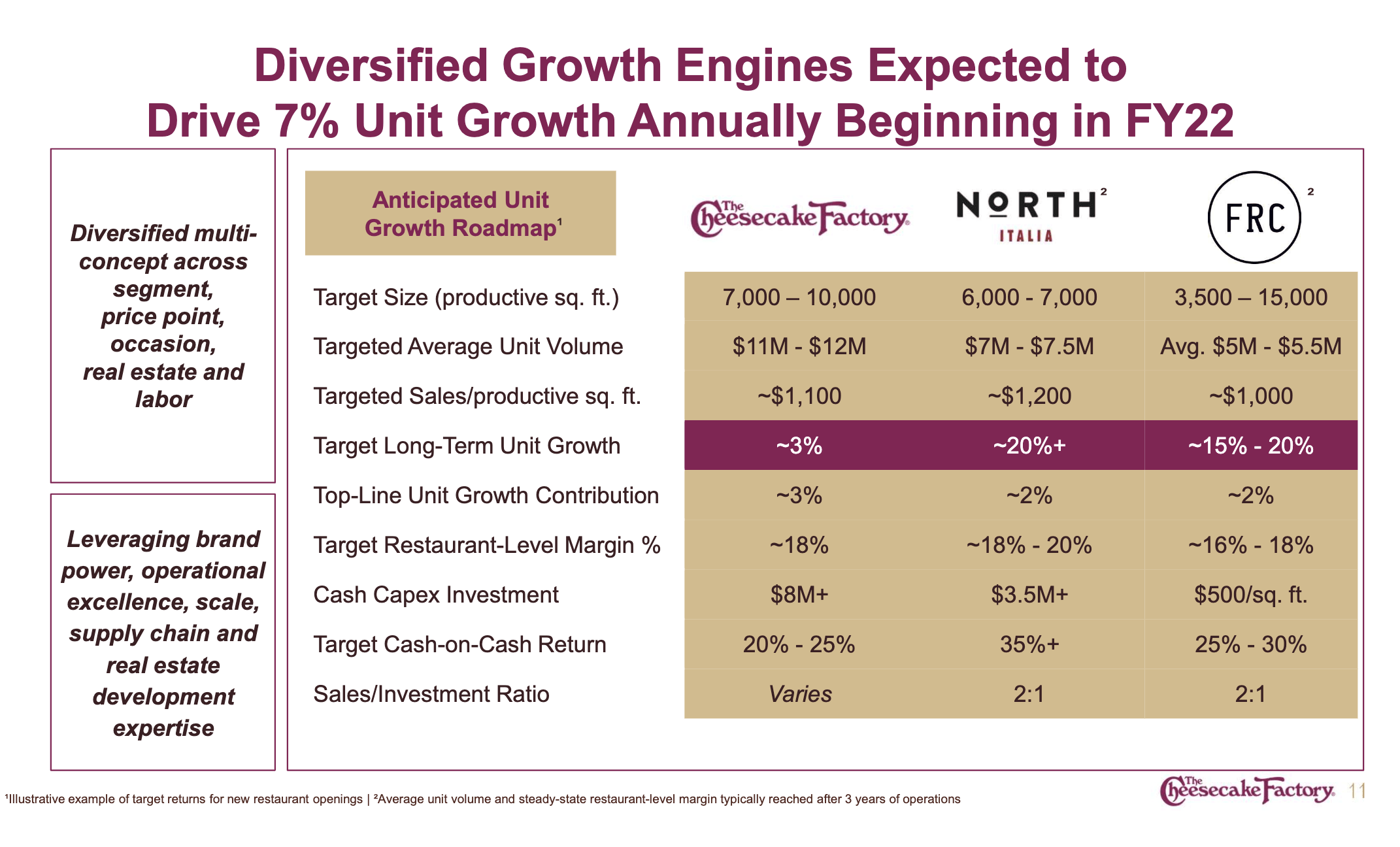

Moving forward, management does have some interesting plans for the business. Citing the attractive payoff of investments in both North Italia and FRC restaurant concepts, the company plans to grow the property count of both types of assets in the years to come. To see what I mean, consider that the average Cheesecake Factory costs about $8 million to set up and generates revenue of about $11.5 million annually. That translates to a revenue to capital expenditure ratio of about 1.4. By comparison, North Italia restaurants, on average, cost closer to $3.5 million to set up and generate revenue of around $7.25 million for a ratio of about 2.1. The numbers for the other FRC properties can vary significantly. But taking an average, you’re looking at about $2.63 million in setup costs for revenue of about $5.25 million annually, which translates to a ratio of about 2. This is why management is expecting long-term unit growth for the North Italia brand to be around 20% or higher, and for the other FRC properties to be between 15% and 20%. That compares to the 3% anticipated for Cheesecake Factory locations. Management also expects, as a result of the favorable ratio, for the cash-on-cash returns to be higher for these new properties by between 5% and 10%, on average. That could help the firm’s bottom line considerably moving forward.

Author – SEC EDGAR Data

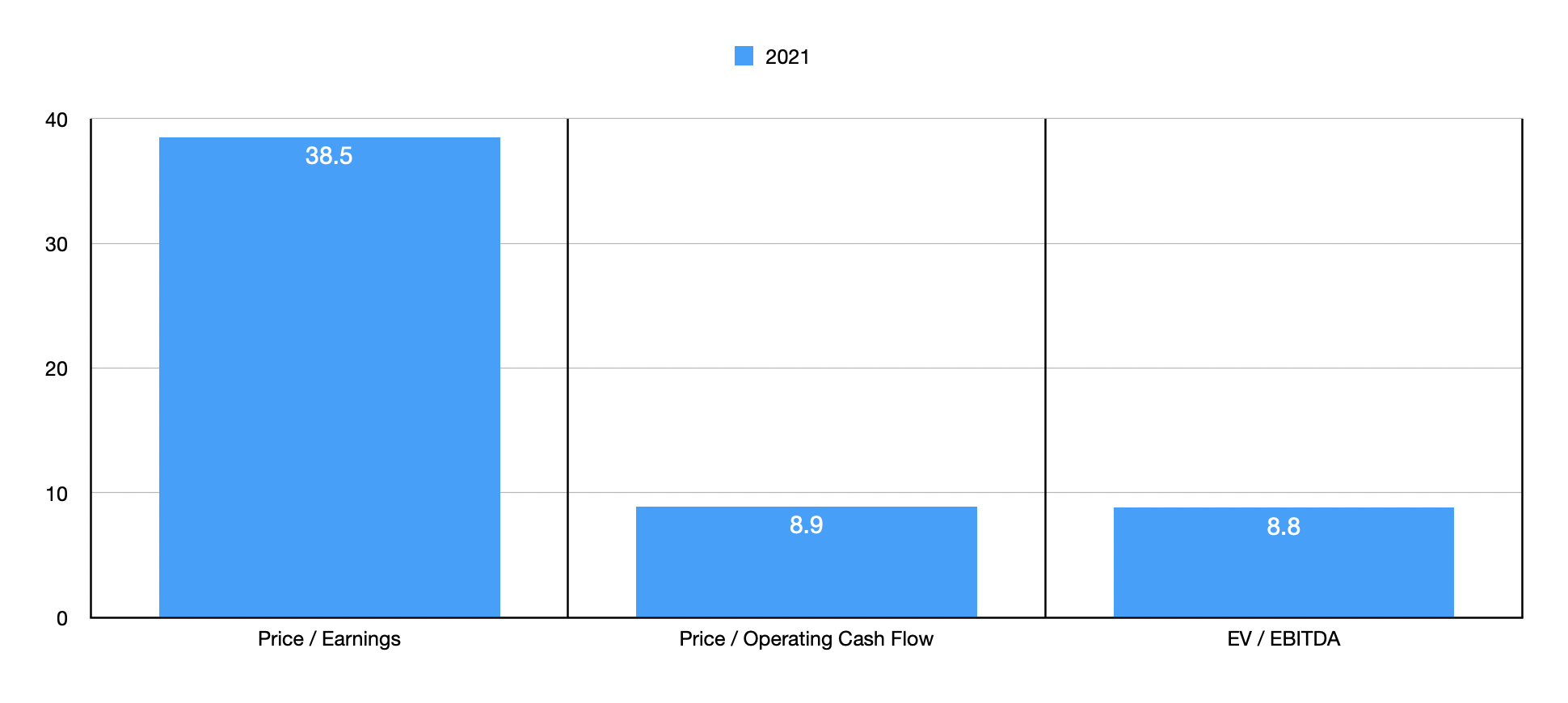

Truth be told, I do not believe that the price-to-earnings approach of valuing this company is very relevant because of how volatile earnings have been. Even so, using the data from the company’s 2021 fiscal year, we find a trading multiple of 38.5. This looks awfully expensive. But in other ways, shares look much more affordable. On a price to operating cash flow basis, the multiple is 8.9. And using the EV to EBITDA approach, the multiple is 8.8. To put this all in perspective, I decided to compare the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 4.8 to a high of 11.7. Three of the five companies were cheaper than Cheesecake Factory. Using the EV to EBITDA approach, the range was from 5.7 to 11.7. In this case, two of the five firms were cheaper.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| The Cheesecake Factory | 8.9 | 8.8 |

| Bloomin’ Brands (BLMN) | 5.9 | 5.7 |

| Dave & Buster’s Entertainment (PLAY) | 11.7 | 11.6 |

| Jack in the Box (JACK) | 10.3 | 9.1 |

| Arcos Dorados Holdings (ARCO) | 8.5 | 11.7 |

| Brinker International (EAT) | 4.8 | 6.7 |

Takeaway

At this point in time, Cheesecake Factory strikes me as an interesting prospect. Shares are probably fairly priced relative to similar firms. But on an absolute basis, shares are looking on the cheap side. I am also interested in the company’s growth plans, particularly whether they can achieve their objectives or not. If they can, then upside for investors might be attractive moving forward. And even if not, there could still be some additional upside for investors.

All in all, I do believe that the inconsistent earnings, even excluding the COVID-19 pandemic figures, makes this far from being a prime prospect. And in general, I believe the restaurant space is incredibly challenging and generally unfavorable to participate in. But for those who want a cheap prospect in this space, Cheesecake Factory may be worth a closer look.