Rising production and input costs, supply-chain disruptions and changing consumer needs due to the coronavirus are facing cattle producers in 2022.

“The biggest concern facing beef cattle farmers this year is the increased cost of raising cattle,” Clemson University Cooperative Extension Area Livestock/Forages Agent, Midlands District Nicole Correa said.

“One big concern that contributes to this is the cattle inventory, especially in the state of South Carolina as a whole,” Correa said. “Nationwide, the cattle inventory has declined and South Carolina has a higher decline than the rest of the nation.”

A severe drought in the northern plains is causing increased cow herd reduction as well.

“The importance of that means that purchasing replacement animals will cost more,” Correa said. “The cost of fertilizers have more than doubled overnight, and accessing herbicides is getting harder, also driving up that cost.”

“As we all see while passing gas stations daily, the cost of gas and diesel have increased, just furthering the dilemma of cost of production,” Correa said. “All of these increases don’t just mean an increased cost directly on cattle operations but also on operations that cattlemen frequently rely on.”

People are also reading…

“We have seen the national fertilizer price index trend downward since November 2021 but is currently still 200% above this time last year,” Clemson University Cooperative Extension Area Agri-Business Agent Matthew Fischer said.

“Fertilizer prices and availability will locally require strategic planning and application,” Fischer said. “2022 will be a year to rely on soil sampling for efficient applications.”

Hay and grain will be at higher costs as adjustments are made to try to offset production costs for those areas.

“It will be important for cattlemen to watch hay production and availability moving into the summer and secure necessary stocks at a price point that pencils out,” Fischer said.

For now at least, prices at the Orangeburg Stockyards are up, per Craig Whisenhunt’s last report at the Orangeburg Cattlemen’s Meeting on Feb. 17.

“Calves marketed through South Carolina sale barns in January and February have seen a premium of $10/cwt to the five-year average and over a $20/cwt to premium to January/February 2021,” Fischer said. “There has been a premium on the calves for the past three years post-June marketing.”

Higher beef prices can be attributed to a high beef demand and retail prices are driving prices paid to producers,” Clemson University College of Agriculture, Forestry and Life Sciences Livestock Specialist Dr. Brian Bolt said.

“There is still a large packer margin in place,” Bolt said. “In other words, prices paid in restaurant and retail settings are disproportionately higher than prices paid for feeder and finished cattle.”

Correa said last year’s live prices were no lower than $4 per pound for consumers, which translates to roughly $7 per pound dressed weight in the Orangeburg area.

“Considering that ribeyes can now cost $20 per pound in a retail location, consumers are still getting a great deal by purchasing a live animal in whole, half, or quarter form,” Correa said.

Global politics has the potential to be disruptive on beef prices in the near term, Bolt said.

“Price premiums for program cattle (i.e., cattle of known management, genetics and third party verified production practices) continue to increase for cow-calf producers in our state,” he said.

Bolt said while cattle prices are positive in comparison to last year, the industry may not be more profitable due to high input costs meaning tight margins for beef cattle producers.

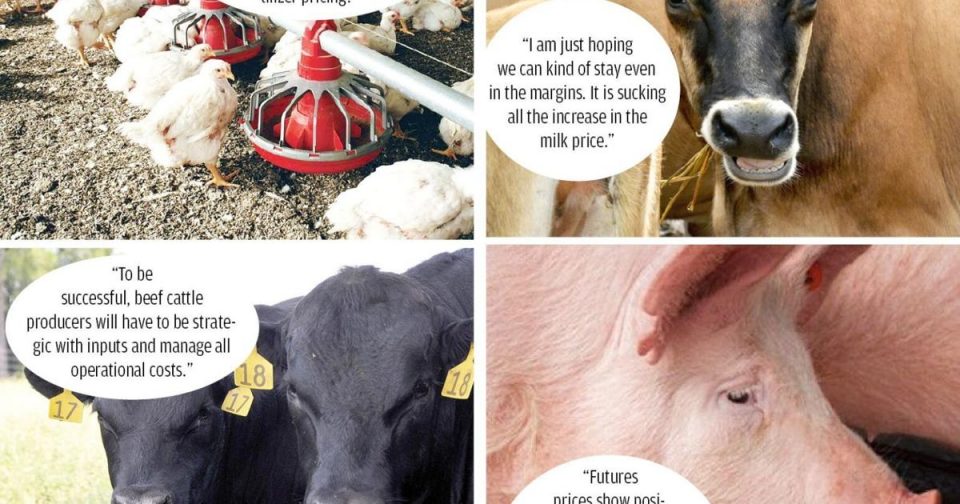

“To be successful, beef cattle producers will have to be strategic with inputs and manage all operational costs,” Bolt said.

COVID has also impacted the industry.

“The largest COVID influence on the cattle industry has been slaughter facility shutdown due to COVID outbreaks among employees and the increased interest in locally grown beef putting pressure on local, custom slaughter facilities,” Clemson Extension Livestock and Forages Extension agent Brian Beer said.

Buying from the farmer

Correa says the virus has encouraged individuals to take a better look at where their food comes from.

“There has been a dramatic rise in individuals wanting to purchase directly off the farm, which can be great for pricing for both cattle producers and the consumer,” she said. “This trend has not subsided and appears to be increasing even with the downward trend of COVID numbers.”

“There has also been an increase in processors who can do custom processing (not USDA-certified) who were previously deer/hog processors to meet the demand of consumers,” Correa said. With that in mind, this could be a great time for producers in the area to consider doing more live animal sales directly to consumers, allowing consumers to make a direct connection with processors to have their live animal turned into meat.”

Correa says while there has been an increase in custom processors in the state of South Carolina since the start of COVID, there has not been an increase in U.S. Department of Agriculture processors, meaning that the meat can’t move through state lines.

“This severe limitation for our cattlemen adversely impacts their ability to market to different areas,” Correa said. “In good news, the Infrastructure Investment and Jobs Act of 2021 was recently signed into law, which should positively affect our producers in a few areas.”

She notes that the the National Cattlemen’s Beef Association fought for an additional 150-air-mile exemption on the destination of livestock hauls, $127 billion for roads, bridges, ports and waterways, and $40 billion to states to build out broadband internet infrastructure along with much more to expand broadband in rural areas. With this assistance, hopefully that will help to open up more opportunities, Correa said.

Correa, citing the latest article by the U.S. Meat Export Federation, showed numbers in 2021 were at a record-setting high in exports. But again with marketing restrictions, is has proven difficult for cattle producers.

“U.S. beef exports surpassed $10 billion, which was up 15% from 2020,” Correa said. “However, considering the current difficulty in S.C. producers getting meat past state lines, let alone exported to different countries, S.C. cattlemen will be unable to see these benefits until something is done about the lack of federal processors.”

As with other agricultural sectors, beef cattle farmers will be dealing with the implementation of the SCATE card for tax-exempt businesses.

After July 1, 2022, agricultural businesses will need to show this card in order to get tax-exempt purchases from any store.

For anyone who needs to apply, information can be found here: https://agriculture.sc.gov/scate/.

Poultry

The top issue of concern for poultry farmers in The T&D Region will be input cost management.

“This is not forsaking flock health,” Fischer said. “Farmers need to focus on feed efficiency as much as energy efficiency.” Input cost increases in the feed grain markets will find their way to the feed bins much like rising fuel cost to the farm.”

Aside from expected input price management, access and availability to inputs will be the change for 2022.

“A big question out there for poultry farmers: What will feed cost and management look like for 2022? How will planting intentions in the feed grain markets react to the current fertilizer pricing?” Fischer said.

Poultry prices are strong.

- National frozen hen weighted average price is roughly 30% above the three-year average.

- All egg classes are priced higher than the same time in 2021.

- Broiler egg sets are up 4% and broiler chick placement is up 1% over the same week in 2021.

“Demand across the poultry industry is mostly moderate and inventories of broilers, eggs and frozen turkeys are currently above this time last year,” Fischer said.

Supply chain issues and global protein markets are also facing poultry farmers this year.

“Supply chain issues arise where we least expect them,” Fischer said. “Given the past few years with various sectors having unforeseen disruptions, it is wise to follow the adage. “A bird in the hand is worth two in the bush.” It is important for poultry farmers to ensure the required inputs are on hand for smoothest operation possible.”

Clemson Extension Associate Professor of Agribusiness and economist at the Sandhill Research and Education Center Dr. Adam Kantrovich said inflation will continue to be an issue for poultry farmers in the short to mid-term.

“We will have to be prepared for this,” he said.

Trade will continue to be a concern, as well as other geopolitical issues that are taking place.

“But some of the trade issues may be in the favor of the U.S.,” Kantrovich said. “Due to the Russian invasion of the Ukraine, some grains typically purchased from that part of the world may be unattainable, pushing for countries to look elsewhere to make their purchases. The U.S. is open for business and willing to sell.”

The negative aspect of the invasion, however, could mean feed cost increases.

Many area poultry farmers contract with Pilgrim’s Pride or Columbia Farms. The companies provide the birds, feed and veterinary services, while the growers provide the labor, housing, litter and utilities.

Dairy

Norway dairy farmer Allen Riddle, a fourth-generation dairyman, milks about 800 cows on 1,300 acres.

“Inflation is the biggest problem,” Riddle said. “Inflation of everything.”

For example, Riddle recently paid $4.25 a gallon for diesel fuel, and the same amount of fertilizer, which cost about $5,000 to put out last year, this year cost him $15,000.

“That is awful,” he said, noting that cost is just for 250 acres.

Riddle said he received about $23 per hundredweight of milk and expects prices to continue to go up through the spring.

But with input costs, margins will be thin. Feed prices since the war in Ukraine are now about $50 a ton.

“The margins are not any better,” he said. “I am just hoping we can kind of stay even in the margins. It is sucking all the increase in the milk price.”

Riddle says he has increased the pay of his workers but “they will use that up in gas money coming back and forth to work.”

Riddle has been farming since February 1970 and says the last two years “have been the craziest of any in my life.”

Kantrovich said the top concern for dairy farmers, especially those needing to purchase the bulk of their ration, is feed and fertilizer costs.

“Presently we are seeing continued strong milk prices with indications of rising milk prices for the fall of 2022, dairy producers should be happy, but due to the value of feed, we may see a tightening between the value of feed and the price of milk,” Kantrovich said.

“Rising input costs will require farmers to pencil out expected results,” Kantrovich said. “This now requires farmers to make management decisions looking at the costs vs. returns as well as the overall cash-flow needs of the farms with many of the decisions that will have to be made. These rising costs can quickly erode the better prices that we are seeing for milk and for culls.”

Kantrovich said it may be time for farmers to begin using the manure sitting onsite to help with soil fertility to help lessen the need for commercial fertilizer.

In addition to higher input costs as much as 200% higher in some cases, Kantrovich said inflation is going to impact the dairy farmer in a few ways this year.

“The inflation we are presently seeing was caused by a few key variables, starting with money provided to individuals (consumers) from the government in response to the COVID pandemic,” Kantrovich said. “This initiated purchasing of all kinds of products increasing their demand and due to the pandemic, limited supplies. This then began the issues we are still continuing to see to some extent with shipping.”

“So as long as consumers have money, they may continue to spend that money including in the protein market i.e. meat, dairy, etc.,” Kantrovich said. “If due to inflation, consumers need to begin to make choices when making purchases, will they begin to purchase less dairy products?”

There is another question.

“Will the increase at the mailbox for milk increase greater than the cost of feed?”

Kantrovich said this is a question that will be able to be answered at the end of the year vs. now.

“Those dairy farmers that have been thinking about retiring or selling the cows may look at the present beef prices and prices at the sale barn and decide it is time to sell now when the prices are high vs. waiting for things to stabilize,” Kantrovich said. “If this occurs, we will see how much of an affect it will have on the dairy industry through possible increase in milk prices due to having a smaller supply of cows and milk produced. But we would need to see this occur on a large scale to have any major effect.”

Despite high input costs, milk prices are strong and should continue to strengthen through fall before beginning to back off toward the end of the year and into early 2023, Kantrovich said.

“For those that have signed up for the Dairy Margin Coverage program through the USDA-FSA … those with a $9.50 coverage level, the milk price trigger looks to be between $21.30-$22.50 for most of the year,” Kantrovich said in early March. “This of course can change drastically tomorrow as global events continue to unfold, changing demand and prices with it.”

Kantrovich said cheese consumption has continued to increase and has done so over the last two decades to about 40 pounds of cheese per consumer annually. Cheese prices have also increased over time. Both production and cheese pricing are not expected to change dramatically.

And this is good news for fluid milk prices.

“Due to the continued demand for cheese, this will only continue to help the milk price if we don’t over produce milk or cheese,” Kantrovich said.

Overall, nationally, according to the USDA Milk Report (Feb. 23) on milk production for the months of December 2021 and January 2022, milk production was down from the same months in the previous year, production per cow was also down (about 14 pounds) and milk cow numbers were also down for the two months.

“The entire 2021-year milk production was up 1.3% over 2020 annual numbers, with production per cow up 171 pounds per cow for the year over 2020 and the U.S. Dairy herd saw an increase of .6% over 2020,” Kantrovich said. “With the tightening of profitability of many small to medium size dairies with some moving out of the dairy business, we may begin to see other more profitable herds begin to expand to take advantage of the present milk prices.”

Overall, Kantrovich said “dairy is in a safe spot right now when looking through a national and global lens.”

“The demand seems to be there, schools have students in them, and we are continuing to see the slow reopening of society from the pandemic,” he said. “I don’t know what the true ‘new normal’ is, and I don’t think we will know until some other issues are resolved. But we have some of our markets back that utilize our dairy products.”

But locally “things may not be as rosy.”

“We have lost so many farms and cows in the recent past, we are seeing our commercial dairy infrastructure go through contraction pains,” Kantrovich said. “This will continue to make some things more difficult for South Carolina dairy farmers. This includes everything from needing to purchase dairy-specific equipment, dairy nutritionist, milk hauling, and even the selling of bred heifers. With fewer dairies, there are fewer buyers.”

Globally, Kantrovich said challenges remain with shipping and processing.

“Trade issues continue to hinder our markets with some countries,” he said. “Although we are seeing great U.S. exports of agricultural products, it could be better.”

While many in the dairy industry are realizing the virus is going to have to be dealt with as other viruses known throughout the ages, he said COVID-19 still means challenges in shipping and manufacturing, creating pinch points around the globe.

“Depending on the events occurring in Europe, hopefully we will continue to see easing in these areas as more of the global population receives a vaccination and or booster for COVID, allowing manufacturing sites to remain open for production and continue to clear the backlog at major shipping terminals,” Kantrovich said.

Labor on the farm is also a challenge for dairymen.

“Local labor continues to be difficult to attract and a cost that remains reasonable for a farmer to afford,” Kantrovich said. “Farms are trying to get creative to attract and/or maintain their farm labor, but it is becoming increasingly more difficult when competing against other industries.”

“Some dairies have had to make production decisions based on the labor they know they have. This unfortunately can have unintended consequences, especially for a dairy where herd health is very important to maintain milk production or if contracting the herd size to meet the labor capacity will have a direct effect on the revenue generated for the farm and to put groceries on the table for the family,” Kantrovich said.

Kantrovich encouraged farmers to engage more with their political representatives in order to address labor issues.

According to the 2017 agricultural census, Orangeburg County ranked second in South Carolina in the number of milk cows at 3,100. The census shows the county has 20 dairy farms.

Despite the decline in dairies over the years, Orangeburg County ranked second in South Carolina in total milk production in 2012 at 48.5 million pounds, according to Southeast Dairy.

The dairy business in Bamberg County, like the rest of the state, has decreased significantly since the 1980s.

There are 10 dairies remaining in the county. The county ranked third in the number of milk cows at 1,800.

Calhoun County does not have any dairy farmers and has not had any for several years.

The Sandy Run Dairy is situated in the northern part of the county just off Interstate 26 at Exit 125 on S.C. Road 31, but the cows that produce the milk for the ice cream it makes and sells are raised outside of Calhoun County.

Swine

The 2022 pork outlook has prices at levels much higher than the previous two years, though input costs could eat into profitability.

“There will be opportunities to price animals at a premium between the months of April and August,” Clemson Extension Associate Farm Management at the Sandhill Research and Education Center Bernt Nelson said. “These higher prices come with an onslaught of obstacles that could impact profitability.”

Lean hog futures have dropped off a bit since the Russian invasion of Ukraine, however, prices are still positioned to remain high, Smith said.

“Russia used to be a major buyer of global proteins. This is no longer the case,” Smith said. “Russia has worked to become self-sufficient in this area.”

Smith said Russia has become a net exporter of pork.

“This suggests that sanctions placed on Russia are likely to have little or no impact on global protein trade,” Smith said.

Locally, prices for feeder pigs in mid-February were $50 per head at an average weight of 38 pounds.

This is up a little from 2021, when feeder pigs ranged from $35 to $47.50 per head under 100 pounds.

Prices for slaughter hogs ranged from $27.50 per cwt to $90 per cwt at the Orangeburg Stockyards in the middle of February.

“Cash prices have rallied since Jan. 1,” Smith said. “Futures prices show positive signs for hog producers. The nearby April contract is in the $103/cwt range with the deferred months like July being even higher.”

“The combination of these two markets tells a story: Cash prices have risen since the first of the year as packers are looking for animals to make up for lower slaughter numbers in December and January due to weather and other continuing challenges,” Smith said. “Futures are showing continued strength in later months for 2022. This provides hog producers with marketing opportunities between April and August.”

Hog and pig inventories are down nationally about 4% from 2020 and 1% since last fall. Breeding herds have also dropped since 2020. These tighter supplies are expected to help maintain prices for the short term.

Input costs are also high.

“Feed prices are already much higher than the previous two years, fertilizer prices have already been increasing because of supply chain and other issues, and now with the instability caused by the Russian invasion of Ukraine, we may see additional increases in fertilizer cost,” Nelson said. “Management of input costs will be the key to profitability in the pork market.”

“Fertilizer prices have risen as much as 200% in 2022, Smith said, providing a snapshot of the situation.

“The Russian invasion brings into question the supply of potash,” Smith said. “The question becomes what happens when all three (nitrogen, phosphate, potash) types of fertilizer are in short supply globally?”

“The U.S. can produce fertilizer and has access to fertilizers from Canada,” Smith said. “This has the potential to tighten grain supply balance sheets such as corn, wheat and soybeans that are used as feed for the protein market.”

In addition to the Russian-Ukrainian war impacting fertilizer supplies, China has an export block on all nitrogen and phosphate products, which is set to expire in June, Smith said.

“China’s decision regarding this will play a role in determining how high fertilizer prices will climb in 2022,” Smith said.

Feed prices have also risen in 2022.

Prices for feeds such as corn and soybeans have all increased since January 1.

Another chink is supply-chain issues.

Smith described the situation the last two years as “chaotic.”

“There was a decreased ability to forecast demand from the service industry due to production and shipping challenges,” Smith said. “2022 should provide more consistency with less restrictions and shutdowns throughout the supply chain than in the previous two years.”

Lower supplies coincide with strong domestic demand.

Packers are trying to get their hands on animals to push the pace of slaughter after slowing down in the December-January months,” Smith said. “The Federal Reserve has indicated that it intends to increase interest rates in March to slow inflation. This may be a player in decreasing demand for protein if consumers cut back on spending.”

Global demand was sluggish at the beginning of the year, Smith said.

While orders for U.S. pork have remained high, February delivery has been slow, Smith said.

“China, South Korea and Mexico have all slowed in taking deliveries of pork,” Smith said. “December shipments were down 17.5% compared to last year. This was the lowest export volume since African Swine Fever (ASF) began to affect herds in some countries in 2018. USDA is forecasting overall pork exports to be down 1.2%.”

Swine’s place at The T&D Region table continues to remain small as integration has kept many farmers from entering the business.

Texas-based Cactus Feeders, which purchased Orangeburg Foods in 2015, is the only significant swine operation locally.

Cactus Family Farms, a division of Cactus Feeders, breeds, gestates and weans pigs and then transports them to be grown and sold to packers. The company also provides farmers with feed and hogs.