Sundry Photography

If there’s one trend that is for certain in today’s market, it’s that growth is out. No investor wants to touch risk right now, especially with rising rates and fears of a global macro recession. This being said, however, many of the steep corrections we have seen in some of the highest-quality growth stocks in the market don’t make sense against current fundamentals.

Snowflake (NYSE:SNOW), a one-time Wall Street darling that has lost 50% of its value this year, is one such example. This data warehousing company sports one of the largest TAMs in the industry, and its weedlike growth rates despite its gargantuan scale prove that is still very much operating in greenfield territory. Investors looking to deploy capital in beaten-down names have a chance here to catch Snowflake on a rebound.

At the height of tech-stock mania during the pandemic, I had been bearish on Snowflake – but now, at significantly diminished levels despite impressive holdup on its financial results, I remain quite bullish on Snowflake’s prospects.

As a refresher for investors who are newer to Snowflake, here is what I consider to be the key bullish drivers for this stock:

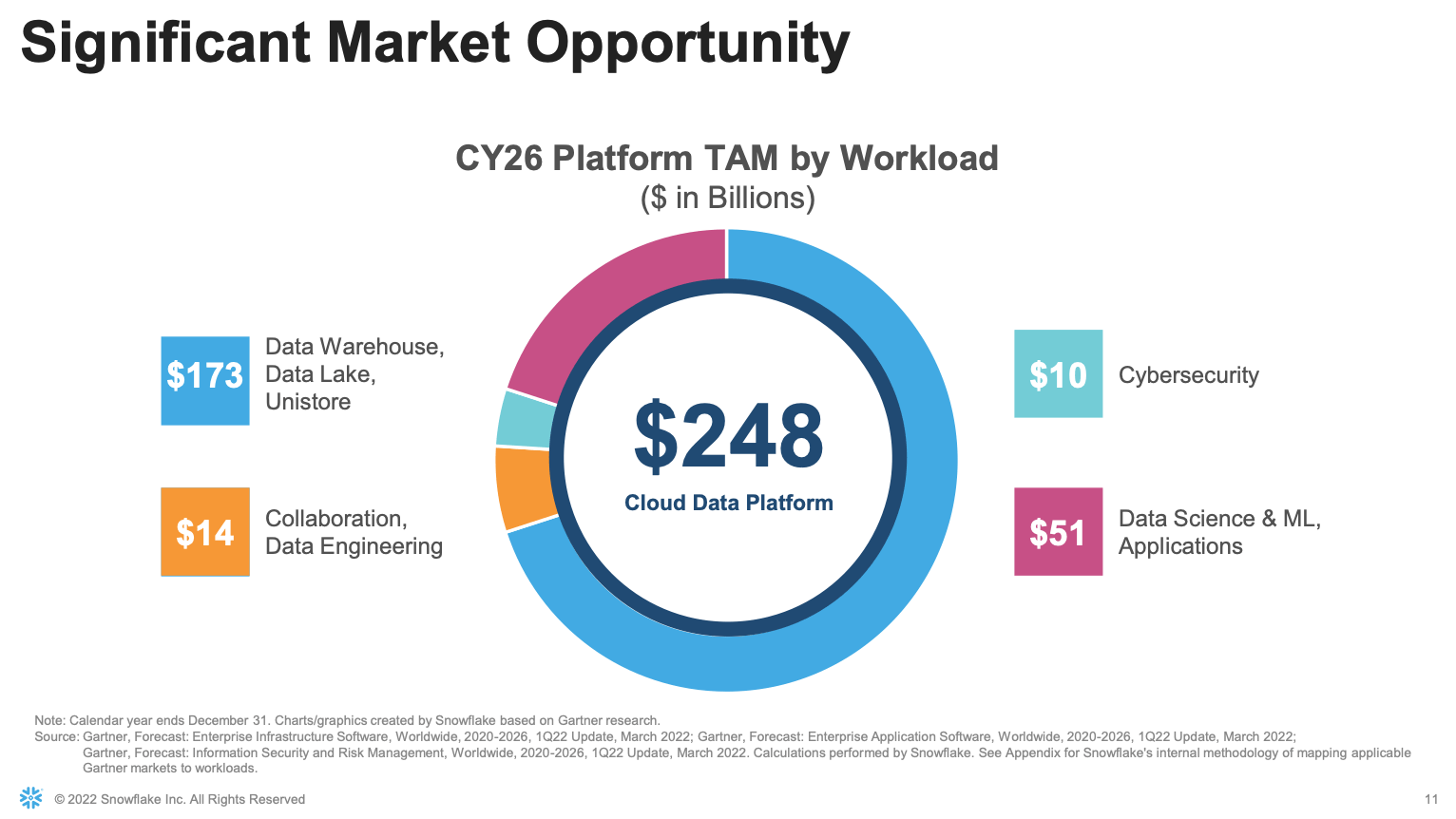

- Large TAM. More to the point above, Snowflake estimates its overall cloud data platform TAM at $248 billion, suggesting that at its current scale, Snowflake is only single-digit percentage penetrated into this market. You can take a look at the breakout of the company’s latest FY26 TAM estimate in the chart below:

Snowflake TAM (Snowflake Q2 earnings deck)

- Humongous growth rates. If you needed proof that Snowflake’s market is a massive one, you only need to look at the company’s top-line growth rate. Even at a ~$2 billion annual revenue scale, the company is still managing to grow at a ~2x y/y pace. That signifies that Snowflake is nowhere near the saturation point, and that there are still plenty of customers left to go – large and small.

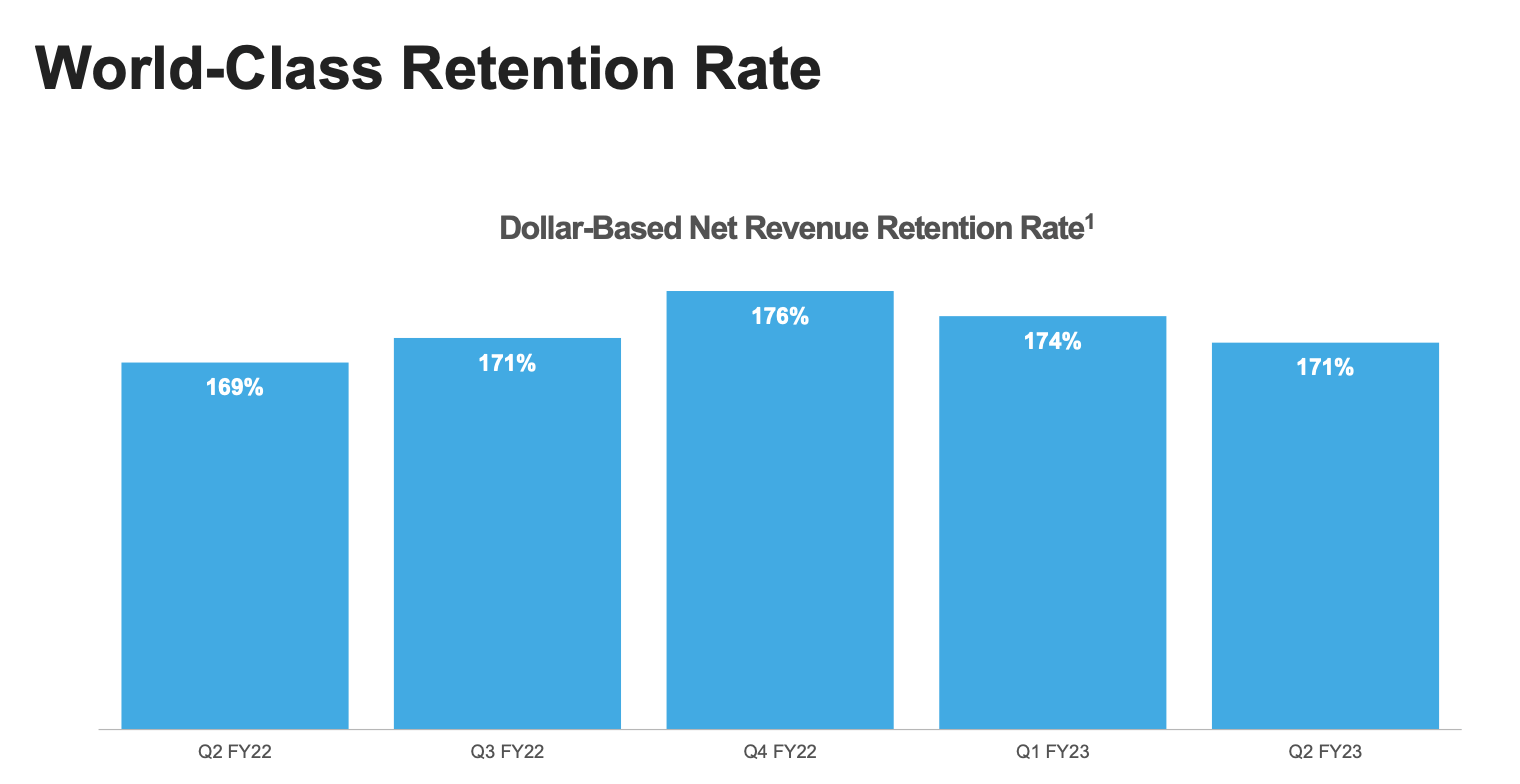

- Consumption-based revenue model. Snowflake adamantly declares that it is not a SaaS company. It charges its customers based on data usage, and this means that as data volumes grow, Snowflake grows as well. Snowflake boasts net revenue retention rates above 170%, which is an insanely high number far above most other software companies (which tend to be in the ~110-120% range). Snowflake grows not only by adding new customers, but by expanding significantly within the existing customer base.

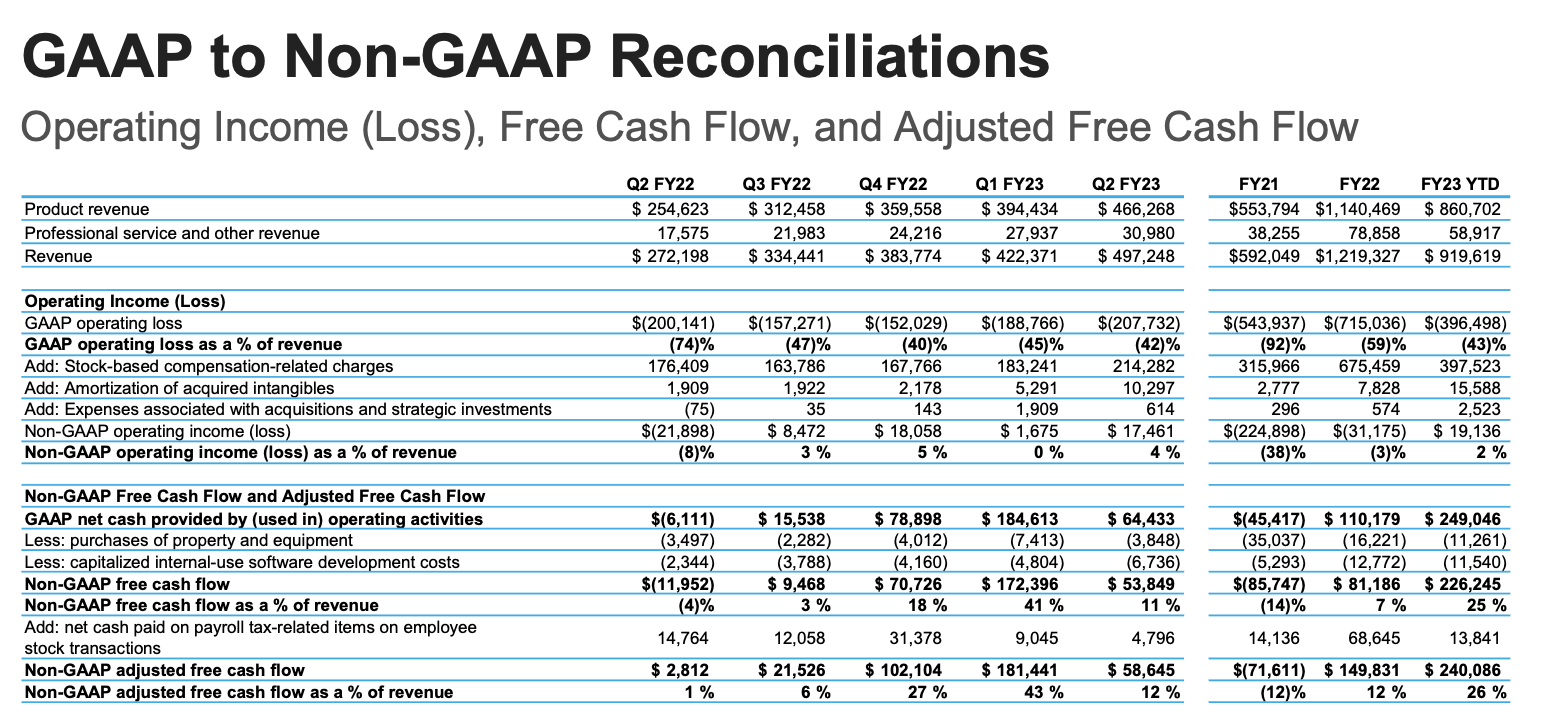

- Profitable bones. Snowflake’s ~70% pro forma gross margins have allowed the company to significantly scale up its profitability as it grows substantially larger. In FY22, the company achieved a -3% pro forma operating margin, which is almost unheard of for a company still growing at a >2x y/y pace; and in FY23, the company expects to be slightly above breakeven. Forget the “Rule of 40” – Snowflake is closer to a “Rule of 100”, and is in a class of its own.

Now, we’ll acknowledge that Snowflake certainly isn’t cheap, even after the year-to-date declines. At current share prices near $172, Snowflake trades at a market cap of $55.08 billion. After we net off the $4.08 billion of cash on Snowflake’s most recent balance sheet, the company’s resulting enterprise value is $51.00 billion.

Versus Wall Street’s FY24 (the fiscal year for Snowflake ending in January 2024) revenue estimate of $3.12 billion, representing 51% y/y growth (data from Yahoo Finance), Snowflake trades at a substantially rich 16.3x EV/FY24 revenue multiple.

I’d argue, however, that A) this is a much cheaper multiple than during the pandemic, when Snowflake traded at >30x revenues, and B) Snowflake’s massive growth rates on top of its expectations of pro forma profitability at such rapid growth rates make near-term revenue valuation multiples more moot. To invest in Snowflake is to bank on earnings that will sit years in the future – but everything about Snowflake’s current trajectory suggests it will get there.

The bottom line here: don’t forget about Snowflake just because momentum has temporarily evaporated on this name. Take advantage of the chance to buy this stock at a great entry point, and hold it well into the future.

Q2 download

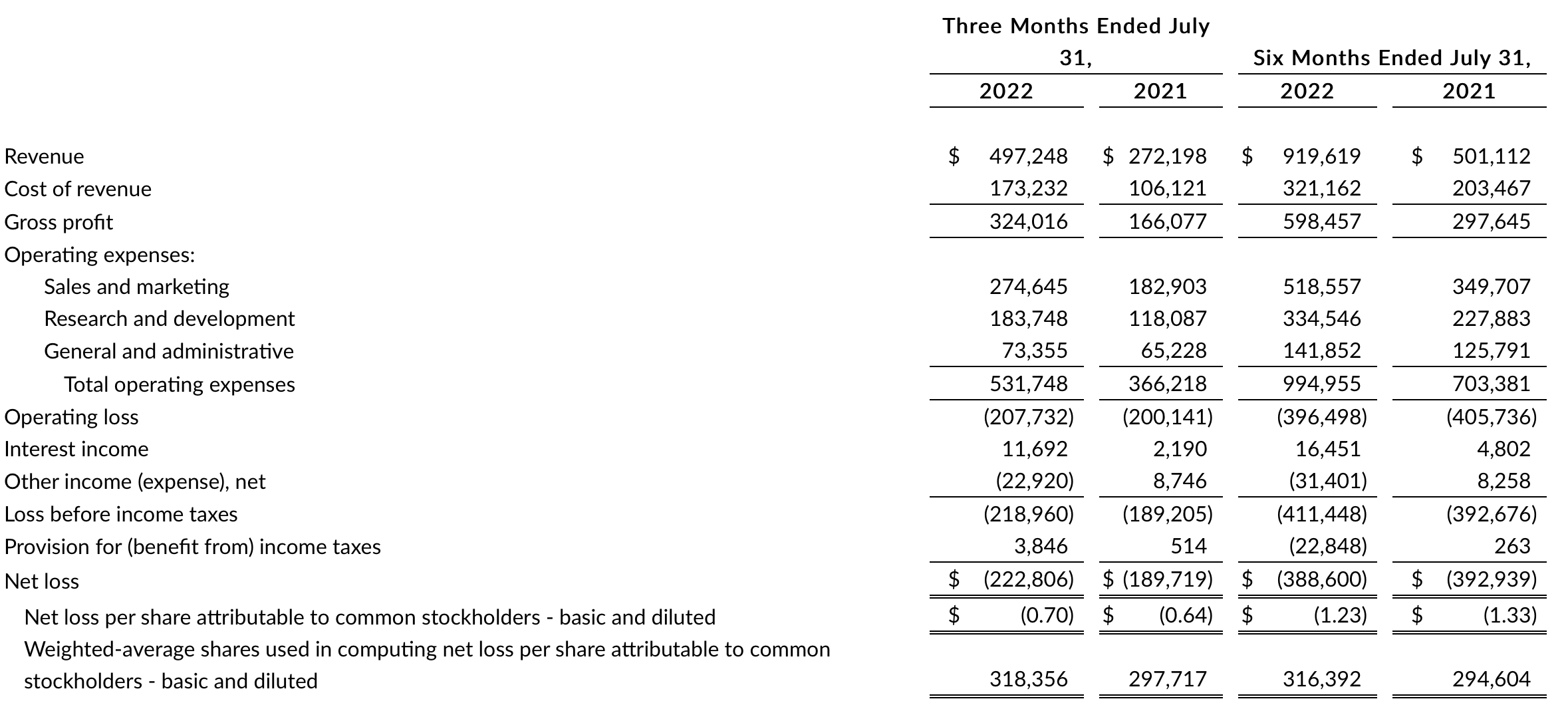

Let’s now discuss Snowflake’s latest Q2 results in greater detail. The Q2 earnings summary is shown below:

Snowflake Q2 results (Snowflake Q2 earnings release)

Snowflake’s revenue in Q2 grew 83% y/y to $324.0 million, beating Wall Street’s expectations of $467.3 million (+72% y/y) by an eleven-point margin. Again, we marvel at the fact that Snowflake can achieve startup-like growth rates despite already being one of the largest software companies in the market.

This is driven in part by the company’s consumption model, where it charges customers based on overall data usage. Snowflake likes to stress that it is not a subscription SaaS platform. Yet despite the popularity of the latter business model, Snowflake has managed to generate among the highest net revenue retention rates in the industry, clocking in at 171% in Q2:

Snowflake net revenue retention (Snowflake Q2 earnings deck)

Some more reassuring news from the company: Mike Scarpelli, the company’s CFO, noted on the Q2 earnings call that management does not currently see any macro-related slowdowns or FX headwinds as being potential drags on the company’s sales (key points highlighted):

Last quarter, we called out customers that were negatively impacted by headwinds specific to their businesses. The Q2 results from these customers were mixed. Some saw the weakness we expected while others outperformed. We are monitoring our key business metrics, which we believe are leading indicators of the macro economy impacting our business. We are not seeing these metrics soften across the customer base.

For example, our corporate sales team that addresses small and medium-sized businesses outperformed their net new bookings goal for the quarter. Our EMEA sales team contributed 4 of our top 10 new customer wins in the quarter. And as mentioned earlier, the largest organizations in the world continue to increase their use of Snowflake. These indicate that companies globally are prioritizing Snowflake right now. Foreign currency exposure has been a relevant topic recently. However, less than 5% of our revenue is invoiced in currencies other than the U.S. dollar. So at the moment, we do not evaluate our business on a constant currency basis given the immateriality.“

And in spite of blazing growth rates, Snowflake also still managed to hit a pro forma operating margin of 4% in the quarter, improving four points sequentially versus breakeven in Q1 and up 12 points versus -8% in the year-ago Q2. The company’s guidance calls for 2% margins for the full year, in-line with YTD operating margins.

Snowflake margins (Snowflake Q2 earnings deck)

Key takeaways

Forget the market turmoil: Snowflake has continued to execute brilliantly, growing at an unheard of pace for its scale and showing the first hints of profitability. This is a company that has a long runway to grow into its valuation (which admittedly is not exactly cheap today) – take the ~50% YTD decline as an opportune buying point and wait patiently for the rebound rally.