This article was selected to be shared with PRO+ Income subscribers – find out more here.

Elevator Pitch

Singapore-listed national postal service provider Singapore Post Limited (OTCPK:SPSTF) (OTCPK:SPSTY) [SPOST:SP] currently trades at 20.8 times consensus forward FY2020 (YE March) P/E and offers a trailing 3.8% dividend yield. Singapore Post’s share price of S$0.93 as of November 13, 2019 is close to its historical five-year share price low of S$0.89.

I am positive on Singapore Post’s recent initiatives and long-term plans to transform the country’s postal landscape and become the national deliverer of all things, including letters, packets and parcels, in the future. But this will take time and could potentially involve the company committing to significant investments to roll out next-generation letterboxes nationwide.

In the near-term, Singapore Post’s Post & Parcel and Logistics businesses continue to suffer from declining business letter volumes and subdued global trade activity respectively.

This is an update of my initiation article on Singapore Post published on August 19, 2019. Singapore Post’s share price has declined slightly by -2% from S$0.95 as of August 16, 2019 to S$0.93 as of November 13, 2019. I retain my “Neutral” rating on the stock, as the stock does have a potential for a turnaround in both its Post & Parcel and Logistics businesses in the long-term, although the near-term outlook remains bleak.

Disposal Of U.S. E-Commerce Businesses Fails To Materialize But Losses Are De-consolidated

In my earlier initiation article, I highlighted the potential divestment of Singapore Post’s U.S. e-commerce businesses, TradeGlobal (an end-to-end e-commerce services provider focused on fashion, beauty and lifestyle brands) and Jagged Peak (an e-commerce logistics enabler for high-velocity consumer products), as the key upside catalyst for the stock.

Earlier, Singapore Post announced on April 3, 2019 that it will start the sale process for its U.S. e-commerce businesses. However, the planned disposal failed to materialize as expected. On September 19, 2019, Singapore Post disclosed that the sale process for the U.S. e-commerce businesses has closed with no offers deemed to be acceptable and commercially feasible. Instead, TradeGlobal and Jagged Peak have filed voluntary petitions for relief under Chapter 11 of the United States Bankruptcy Code in the United States Bankruptcy Court for the District of Nevada. It was disappointing that Singapore Post could not realize any value from the two U.S. e-commerce businesses, which it earlier spent approximately $180 million to acquire in 2015.

On the flip side, the two U.S. businesses’ losses are completely de-consolidated from Singapore Post’s financial numbers with effect from September 2019. Singapore Post’s profit and loss statement is now presented as “Continuing Operations” (excluding U.S. e-commerce businesses) and “Discontinued Operations” (losses from the U.S. subsidiaries for the period prior to de-consolidation). The losses from discontinued operations will continue to be represented in the company’s accounts until September 2020, purely for comparative purposes.

In other words, Singapore Post will no longer recognize any profit or loss associated with the U.S. e-commerce businesses going forward. This suggests that Singapore Post’s 2HFY2020 (YE March) numbers are expected to boosted by the de-consolidation of the U.S. e-commerce businesses, as loss from discontinued operations of approximately S$12 million in 1HFY2020 represented close to 19% of the company’s profit from continuing operations of S$52 million for the first half of FY2020.

Positive On New Initiatives For Post & Parcel Business In The Long Term

Singapore Post’s core Post & Parcel business segment, which accounted for 57.4% and 87.3% of the company’s 2QFY2020 revenue and operating profit respectively, continued to be under pressure in the most recent quarter. Singapore Post’s Post & Parcel business saw segment operating profit decline by -20.8% YoY from S$42.6 million in 2QFY2019 to S$33.8 million in 2QFY2020. The continued secular decline in business letter volumes (partially offset by growth in e-commerce related deliveries), a decrease in advertising mail volumes and higher expenses associated with service quality improvements were responsible for the Post & Parcel business segment significant operating profit decline for the recent quarter.

The domestic postal business has high fixed costs in terms of infrastructure, so there is significant operating leverage within this business. As a result, a small decline in domestic mail volumes can translate into a significant fall in profits. It is worrying that Singapore Post highlighted in its recent 2QFY2020 earnings call on November 4, 2019 that “H1 (first half of FY2020) was indeed an accelerated decline as well as a concern compared to previous quarters previous years.”

On October 30, 2019, Singapore Post announced new initiatives, which are part of plans to turn around its core Post & Parcel business, in response to decreasing mail volumes and the growth of e-commerce. The key new initiatives coming into effect from December 2, 2019 include new postal service categories for packages and the renaming of its existing Ordinary Mail services to Basic Mail with new restrictions on mailing.

The two new postal service categories for packages are “Basic Package” and “Tracked Package” which are specifically for packages weighing up to two kilograms and delivered to the recipients’ letterboxes. “Basic Package” is a basic letterbox package delivery service with no delivery tracking or notification; while “Tracked Package” is an over-the-counter package delivery service that also delivers packages to the recipients’ letterboxes, but this category allows customers to be updated on the delivery progress of the package, and recipients to be notified when the package is delivered to their letterboxes. “Tracked Package” is slightly more expensive with a price range of S$3.20-S$4.80, versus S$0.90-S$3.50 for “Basic Package.”

For packages weighing up to two kilograms and being able to fit into a standard letterbox (maximum dimension of 240mm x 340mm x 70mm), Singapore Post’s “Basic Package” and “Tracked Package” services are expected to gain market share away from courier companies which are reliant on doorstep deliveries, as consumers find it inconvenient to wait at home for doorstep deliveries. As the national public postal licensee, Singapore Post is the only one with the right to deliver into letterboxes, and letterboxes remain the most cost-effective and convenient way of delivering small packages weighing less than two kilograms, versus alternatives such as doorstep delivery or locker systems utilized by certain courier companies.

Existing Ordinary Mail services will be renamed as Basic Mail, only accepting letters and printed papers up to 500 grams for delivery. Items that weigh between 501 grams and two kilograms will have to be delivered via Singapore Post’s “Basic Package” and “Tracked Package” package delivery services. Prior to this change, customers sent small packages using Singapore Post’s existing Ordinary Mail services (which was primarily meant for letters), which was a significant burden on the company’s business operations and operating efficiency.

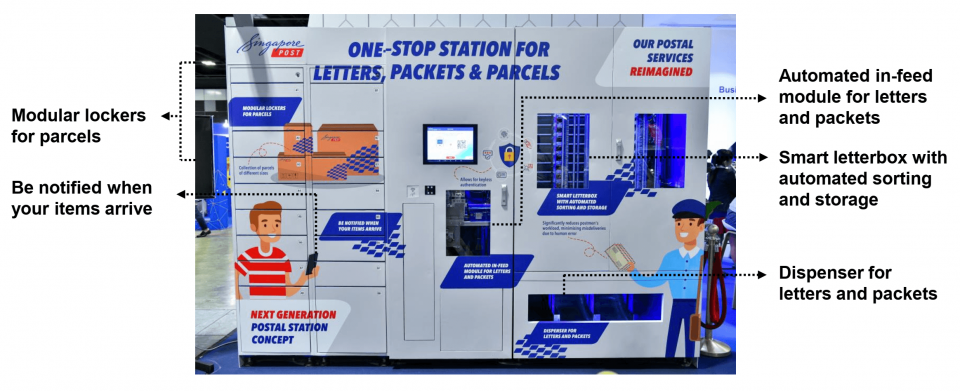

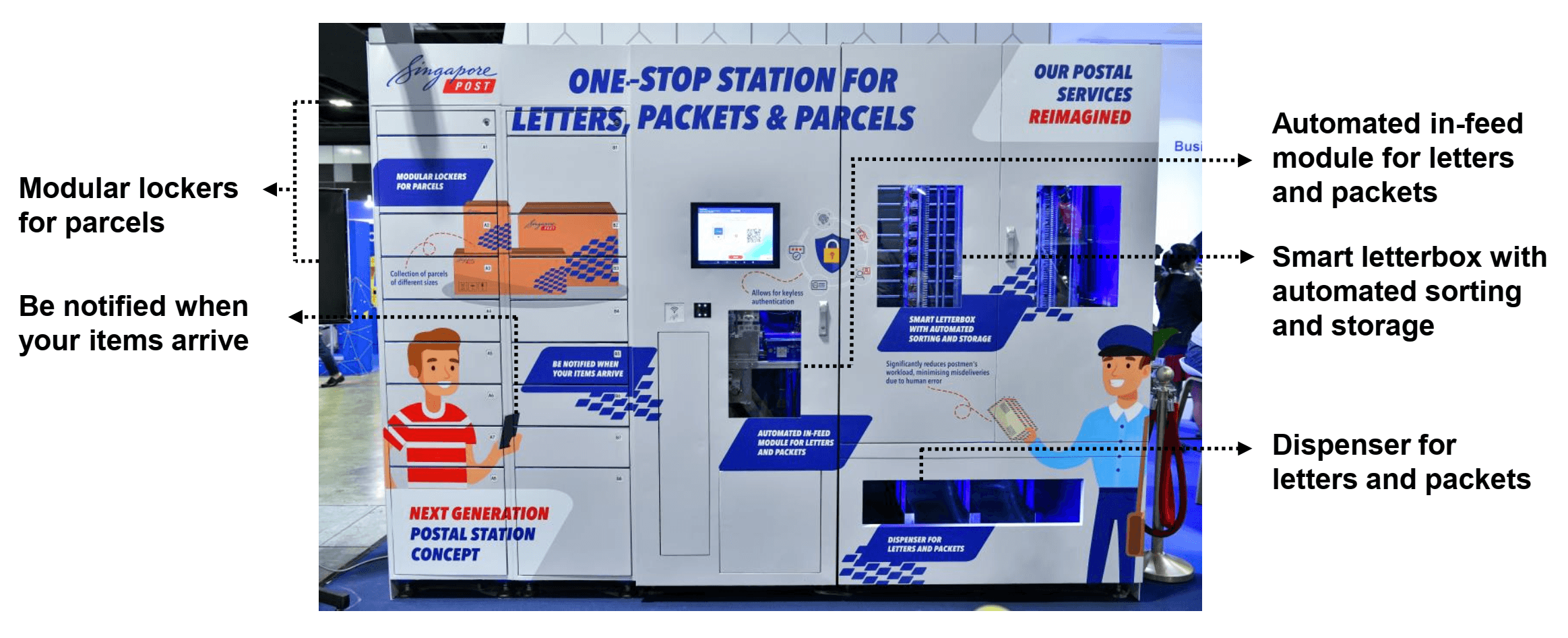

More importantly, these new initiatives are just the beginning of Singapore Post’s plans to transform the country’s postal service. The endgame that Singapore is envisaging is what it refers to as the “Future Of Post” with “Smart Shared Letterboxes.”

Singapore Post is currently in discussions with authorities regarding introducing its “Smart Shared Letterboxes” nationwide in future. The “Future Of Post” will see “Smart Shared Letterboxes” equipped with automated sorting & storage and an automated in-feed module for letters and packets being located across Singapore similar to regular letterboxes now. From the perspective of customers, they will have the ability to both send and receive letters & parcels conveniently using these next-generation letterboxes relying on autonomous authentication and mobile or email notifications. In the case of Singapore Post, the company will save significantly on costs, as most of the existing large parcels will be able to be delivered via letterboxes, rather than doorstep delivery. In the future, Singapore Post could be potentially become the national deliverer of all things, including letters, packets and parcels, with “Smart Shared Letterboxes” which would be a game changer for the company.

Singapore Post’s Smart Shared Letterboxes

Source: Singapore Post’s 2QFY2020 Results Presentation

Source: Singapore Post’s 2QFY2020 Results Presentation

However, it is too early to be positive on Singapore Post. In the short-term, the company’s recently announced initiatives will generate certain cost savings with a reduction in doorstep deliveries for smaller packages, but this will be largely offset by the continued decline in business letter volumes as corporate clients switch from physical mail to e-bills and digital communication. At Singapore Post’s recent 2QFY2020 results briefing on November 4, 2019, the company also acknowledged that the profit margins on delivering small packages will never be as high as that of delivering letters. In other words, Singapore Post is unlikely to be able to completely offset the loss in profit from declining business letter volumes with an increase in small package delivery volumes.

Singapore Post will have to obtain approval from the authorities prior to rolling out its “Smart Shared Letterboxes” nationwide. More importantly, it will take a significant amount of time and costs (building and setting up these next-generation letterboxes across the country) before the company can realize its vision for the “Future Of Post.”

Logistics Business’ Profitability Is Key To Offsetting Weakness In Core Post & Parcel Business

The Logistics business is the second largest revenue contributor after the core Post & Parcel business, accounting for 38.7% of Singapore Post’s 2QFY2020 revenue. But the Logistics business remained loss-making with an operating loss of -S$0.9 million in 2QFY2020, which widened from -S$0.7 million in 2QFY2019. This was mainly attributable to a decline freight forwarding volumes due to a slowdown in global trade and higher on-boarding costs for its new e-commerce customers in Asia Pacific.

The Logistics business’ Quantium Solutions subsidiary, a provider of logistics and fulfillment services across Asia-Pacific, continues to sign on profitable new clients to replace the revenue loss associated with exiting prior unprofitable contracts. Quantium Solutions’ revenue was up +9% YoY in 2QFY2020, and losses narrowed by 25%. The Australian logistics subsidiary, CouriersPlease, a leading metropolitan express parcel delivery service in Australia, has delivered positive revenue and earnings growth in local currency terms for 2QFY2020, and it has plans in place to optimize both the top line (targeting specific large Australian retailers for future growth) and bottom line (improving cost management via enhancing fleet efficiency and process re-engineering). On the other hand, the Logistics business’ Famous Holdings subsidiary, a freight consolidator and freight-forwarder with a regional presence in seven countries, has been hurt by a global slowdown in trade activity.

Putting short term headwinds aside, Singapore Post’s Logistics business remains unprofitable because of a lack of scale as highlighted in my earlier initiation article referenced in the “Elevator Pitch” section. Looking ahead, Singapore Post will have to build up the size of the Logistics business, either organically via acquiring new clients, or inorganically via acquisitions.

Valuation

Singapore Post trades at 20.8 times consensus forward FY2020 (YE March) P/E and 17.2 times consensus forward FY2021 P/E based on its share price of S$0.93 as of November 13, 2019. This is roughly on par with the stock’s historical five-year average forward P/E of approximately 19 times.

Singapore Post offers a trailing 3.8% dividend yield based on a consistent payout of S$0.035 per share every year. At the company’s 2QFY2020 earnings call on November 4, 2019, Singapore Post emphasized that there is no direct link between the company’s future dividend payout and the improvement in the company’s profit due to the de-consolidation of its loss-making U.S. e-commerce businesses. This is because Singapore Post needs to re-allocate most of the associated savings from the de-consolidation of its loss-making U.S. e-commerce businesses to rationalize its core postal business and invest in other potential overseas opportunities.

Variant View

The key risk factors for Singapore Post are a failure to execute well on new initiatives and future plans for its core Post & Parcel business, a faster-than-expected rate of decline for domestic mail volumes, and a longer-than-expected time for its Logistics business to be profitable.

Asia Value & Moat Stocks is a research service for value investors seeking value stocks with a huge gap between price and intrinsic value, leaning towards deep value balance sheet bargains (i.e. buying assets at a discount e.g. net cash stocks, net-nets, low P/B stocks, sum-of-the-parts discounts) and wide moat stocks (i.e. buying earnings power at a discount in great companies like “Magic Formula” stocks, high-quality businesses, hidden champions and wide moat compounders). Sign up here to get started today!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.