LONDON (ICIS)—The European Court of Auditors

(ECA) has assessed a significant risk that the

EU will not meet its plastic packaging

recycling targets for 2025 and 2030.

The

report, which was released on Tuesday,

highlights that changes to the Packaging and

Packaging Waste Directive (PPWD), which was

updated as part of the European Comissions’

adoption of its plastic strategy in 2018, could

see current reported plastic packaging

recycling rates of 42% across EU member states

revised down to 30%.

Current reported recycling rates are “far from

being accurate or comparable across Member

States,” the report concludes.

It also highlights that impending

changes to the ‘Basel Convention’ which

from 2021 will see strict restrictions come in

to force on the export of plastic waste. It

argues that, at present, member states are

reliant on waste exports to non-EU countries to

meet their recycling waste commitments.

The ECA estimates that nearly a third of the

EU’s reported plastic packaging recycling rate

is down to exports to non-EU countries.

Although not mentioned in the report this has

significant implications for the

EU plastics charge of €800/tonne which is

due to come into force in January and paid by

member state. The charge will use the PPWD and

its implementing Decision to calculate the

amount each member state is required to pay. If

recycling rates are revised down due to changes

in reporting this will result in a heavier

financial burden for each member state.

The charge is not a tax, although commonly

referred to as one, because it is payable at

state level rather than by individuals or

corporations. Nation states could,

however, seek to recover the cost of the charge

through taxation.

The methods used to meet the cost of the charge

will be up to individual countries, and the EU

Council has not proposed any regulatory

stipulations around this.

Individual countries are free adopt different

approaches and could seek to recoup the cost of

meeting the charge from differing parts of the

supply chain, leading to potential regulatory

divergence.

Coupled with this, it takes on average

12-18 months to build a recycling processing

facility and average testing times at packaging

firms are around 18-months, meaning that any

additional recycling capacity resulting from

the bill will not enter the market by the time

the bill takes effect. This runs the risk that

any cost relating from the charge will simply

be passed on to the consumer, or will encourage

a shift to other materials regardless of

whether the environmental impact is

greater or smaller.

The only country which has so far announced how

it will pass through the EU plastics charge to

the supply chain is Austria, which will

implement a tax on plastic packaging

manufacturing, reusable quota and a Deposit

Return Scheme (DRS).

Regulatory and consumer pressure against

single-us plastic continues to grow. As a

result many Fast Moving Consumer Goods (FMCG)

brands have announced ambitious recycled

content target for plastic packaging, which

typically go beyond regulatory requirements,

with a target of 50% recycled content common.

ICIS has repeatedly highlighted the current

shortages of waste collection

infrastructure and recycling capacity to meet

these targets. The

effects of the Covid-19 pandemic – which

has seen delays to investment and limited

underlying growth in 2020 – have made these

targets even more difficult to achieve.

“The conclusions from the ECA are

unsurprising,” says ICIS, Senior Analyst

Plastics Recycling, Helen McGeough,

“Having assessed the recycling industry,

particularly for the more mature RPET market,

ICIS found the 2025 targets were clearly

challenged due to slowing collection rates and

increasing contamination levels, alongside the

continued trade of waste despite changing

regulations.

The standardisation of recycling rate

measurement clearly exposes some of the

challenges in the recycling chain.”

Meeting food packaging targets presents a

particular problem for most polymers because of

the absence of large quantities of suitable

waste volumes. This is due to contamination,

the prevalence of mixed-recycling chains, the

economics of sorting and separating, and

tensile strength weakening during the recycling

process.

In Europe, the challenge is heightened by the

European Food Safety Authority (EFSA)

requirement that 95% of material used in

food-contact approved recycled material must

have originated from a food contact source. For

recycled polyethylene terephthalate (R-PET)

this is relatively easy to ensure since the

bulk of collected material is from

post-consumer drinks bottles.

For other polymers, where end-use sources are

varied and typically collected in a single

input stream, it is an intense challenge and a

barrier to market growth.

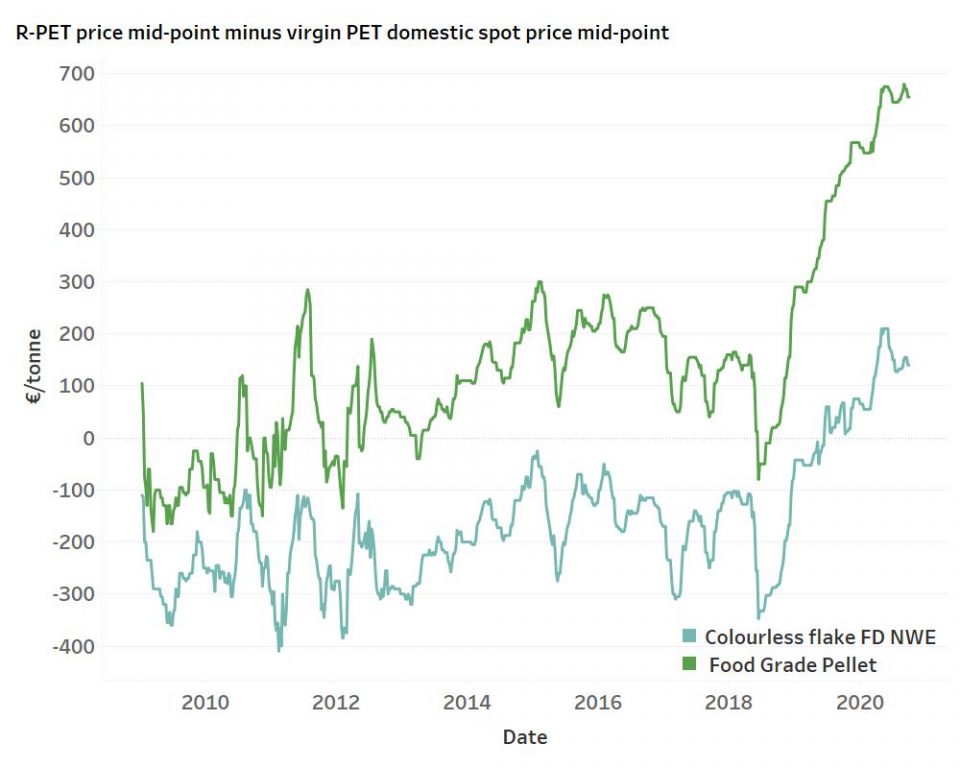

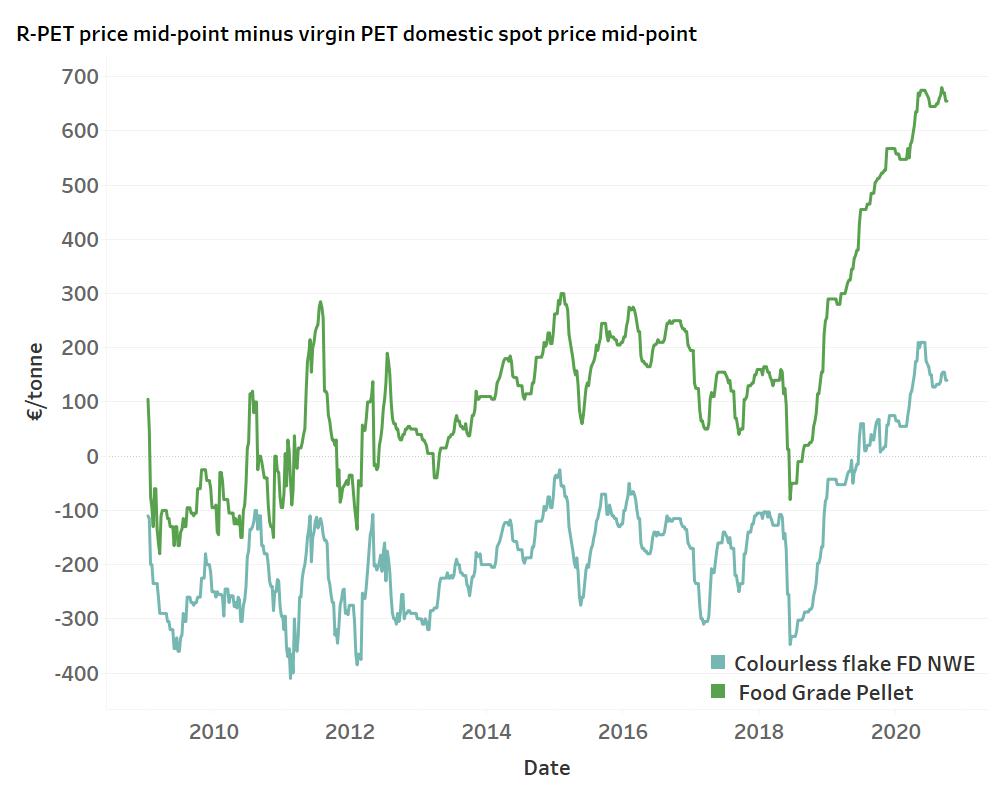

Even with R-PET there is only currently around

350,000 tonnes/year of food-grade pellet

capacity.

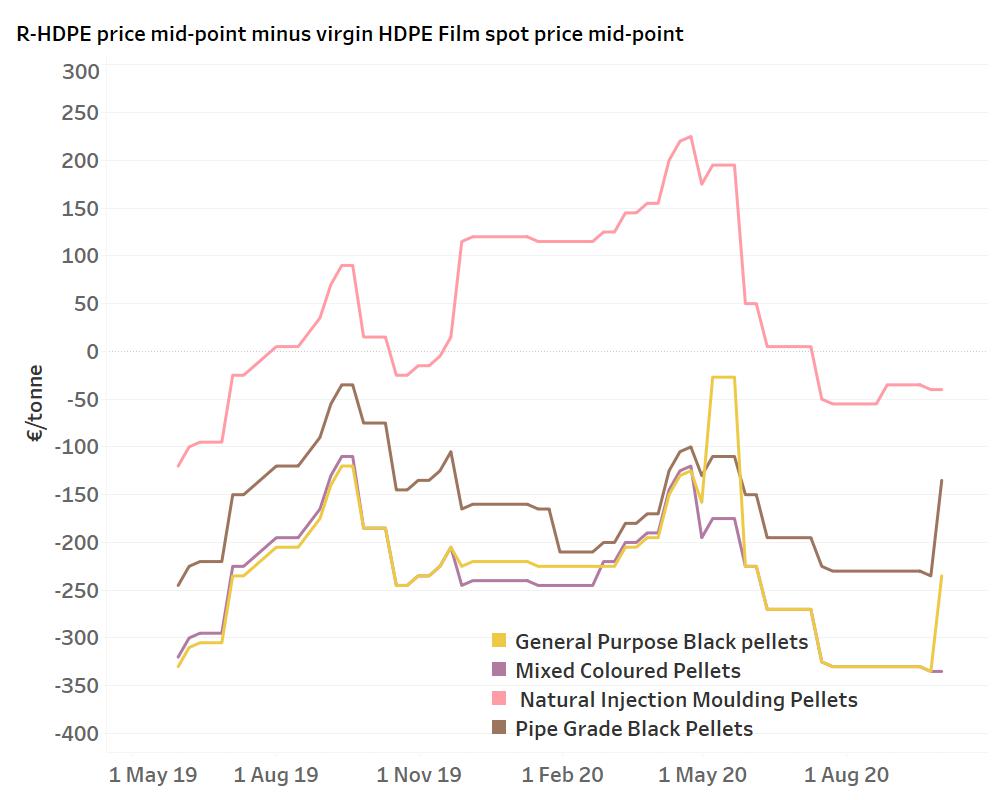

Structural shortages have seen prices of

recycled polyethylene terephthalate (R-PET),

recycled polyethylene (R-PE) and recycled

polypropylene (R-PP) for grades serving the

packaging sector increase and exceed virgin

values in Europe in recent years.

Many players see chemical recycling as a magic

bullet. Nevertheless, it remains in its

infancy, can increase competition for

mechanical recycling plastic waste bales due to

contaminant and moisture limitations for some

depolymerisation processes, and can be

cost-intensive and low yield. Coupled with

this, the legal status of chemical reycling

remains

uncertain.

At any rate, with sources estimating it will

take at least 5-10 years for chemical recycling

to reach industrial scale, it may come too late

to assist with legislative targets.

“Relying on chemical recycling to address the

supply gap is unrealistic given the

timeframes as already discussed,” said

McGeough.

“It is clear that the near term challenges

for the plastic packaging industry rely on

combatting the entrenched issues that

continue to impede the long term development

of the recycling industry.

“Investment in the front end of the supply

chain is key but also the least likely to

happen in a time when governments are facing

the financial hurdles of a pandemic and

global economic downturn.

“It should not come as any surprise that the

plastic packaging industry is in line to bear

the bulk of the costs of recovery and

recycling. However, there is the risk that

the reaction will be to switch to potentially

more harmful materials rather than address

the end of life issue of packaging

altogether.”

ICIS is prototyping a new Recycled

Polyethylene Terephthalate (Asia) price

report for more details and to receive a copy

of the prototype, please

contact [email protected].

Insight by Mark Victory

(Thumbnail picture: A recycling plant in

Sweden. Source: IBL/Shutterstock )