The report titled “Saudi Arabia Dry Logistics and Warehousing Market Outlook to 2025 – Warehousing Automation and Investment within Transport Infrastructure to Drive Market Revenue)” provides a comprehensive analysis of the dry logistics industry of Saudi Arabia. The report also covers an overview of transportation infrastructure, major economic / industrial zones, International benchmarking basis Logistics Performance Index, overall logistics and warehousing market size and dry logistics market size and market segmentation by service mix (freight forwarding, warehousing and value added services including customs clearance) and by regions / cities (Jeddah, Riyadh, Dammam and Others); dry freight forwarding market segmentation by freight mode (road, sea, air and rail); by inter-national and domestic freight (road freight, sea freight and air freight); by flow corridors (Asian Countries, European Countries, Middle East, NAFTA and Others); and by international and domestic companies; dry warehousing market segmentation by business model (industrial / retail warehouses and container freight / inland container depots), by end users (construction material / industrial, consumer retail, food & beverage, healthcare, automotive and others), by entities (real estate companies, captive companies and logistics companies) and by regions / cities (Jeddah, Riyadh, Dammam and Others); Customs clearance procedures followed at sea ports and airports, customs clearance revenue by sea and air out of Value Added Services; Trade scenario, trends and developments, issues and challenges, SWOT analysis, regulatory landscape, Descision making process, VAT impact on the logistics and transportation industry and law of public transport on roads of the KSA; Cost of setting up a logistics business in Saudi Arabia, Comparative landscape including cross comparison of major players operating in KSA dry logistics market and cross comparison of major players operating in KSA online retail market. The report also covers cost component model for trucking industry in the Kingdom of Saudi Arabia, Warehousing investment and operation model; and container yard models in Dammam and Riyadh regions. The report concludes with future market projections on the basis of overall logistics and dry logistics revenue, by service mix and analyst recommendations highlighting the major opportunities and cautions.

Saudi Arabia Dry Logistics and Warehousing Market

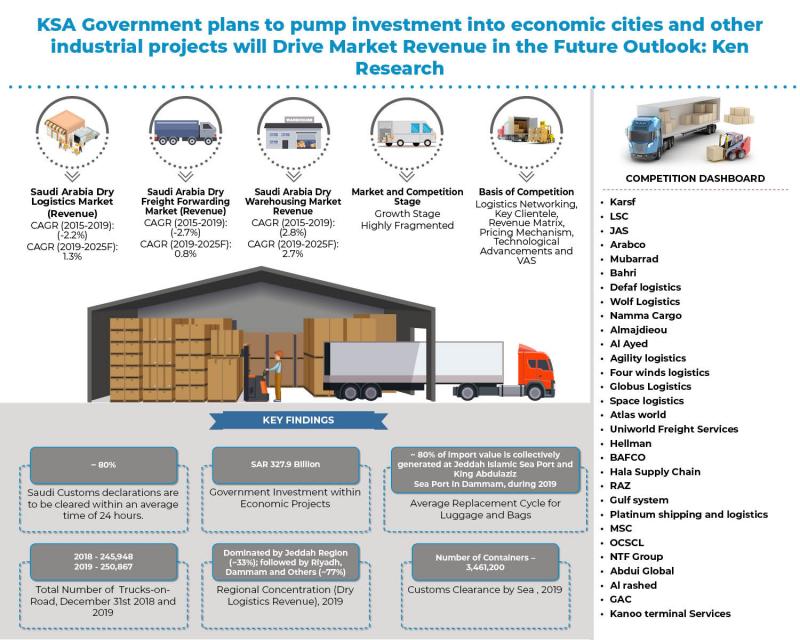

The market showcased a volatile growth trajectory. Dry logistics revenue declined at a CAGR of single digit CAGR during 2015-2019 due to oil price shock further leading to an economic slowdown during 2016-2017 period. Saudi Arabia is located at the crossroads of significant international trade route that connects Asia, Europe and Africa. This strategic location provides the Kingdom with a unique advantage over other nations thus, enabling it to become a leading regional logistics hub. In April of 2016, Saudi Arabia announced its Vision 2030 which includes transforming the Kingdom into a preferred logistics hub. It is making continuous efforts to make imports and exports processes more streamlined. Additionally, government is restructuring the regulations and structures logistics sector government and opening the way for market liberalization and private sector participation. Expansion of industrial cities continues to offer opportunities for foreign investors towards developing the non-oil manufacturing base, warehousing & logistics segments. For instance, Pfizer opened a manufacturing facility in the King Abdullah Economic City in the year 2017. Non-oil manufacturing growth is facilitated by launch of National Industrial Development and Logistics Program (NIDLP) in Jan 2019 by KSA government. Various companies are investing in Special bulk trucks and heavy lift movements to diversify their Revenue streams and Operations. For instance, Bahri launched new dry-bulk carrier ‘Sara’ & increased their total fleet of dry-bulk carriers to 6 ships in KSA.

For More Information on the research report, refer to below link:-

https://www.kenresearch.com/automotive-transportation-and-warehousing/logistics-and-shipping/saudi-arabia-dry-logistics-and-warehousing-market-outlook-to-2025/366821-100.html

Saudi Arabia Dry Logistics Market Segmentation

By Service Mix (Dry Freight Forwarding, Dy Warehousing and Value Added Services): The industry is highly fragmented with few players offering complete end-to-end logistics solutions. The inability of domestic and international providers to offer nationwide end-to-end logistics is due to the lack of a capable and willing workforce, as well as issues around asset ownership, IT requirements, structural and legislative trade restrictions. The freight-forwarding segment of the logistics market is the biggest contributor to growth in this sector.

By Regions (Jeddah, Riyadh, Dammam and Others): Jeddah has been dominated in terms of dry logistics revenue during 2019. The cities of Jeddah & Riyadh have been the most populous cities in the kingdom. These cities also account for most of the industrial areas and indicate a high demand for built-to-suit and automated warehouses therefore, driving revenue from dry goods storage. Lastly, value added services segment include packaging, labelling, inventory management, cross docking, and door-to-door delivery.

Saudi Arabia Dry Freight Forwarding Market:

Freight forwarders offer all a limited range of services depending on their size, number of personnel, and number of branches. Major Flow corridors include the Asian region and European countries in terms of freight revenue during 2019. Saudi Arabia launched new logistics zone in 2019 which is open to private investors in the Red Sea port city of Jeddah therefore, diversifying the economy away from oil and creating more jobs for local Saudis. Road was observed as the most prominent freight mode in Saudi Arabia for dry logistics, followed by air, sea and rail in the year 2019. International freight had dominant share largely due to higher exports of F&B, white goods, textile, furniture & machinery, engineering products, industrial products and others. Asian Countries were observed to lead in terms of International Freight Movement. Major export destinations include China, Singapore, India, Malaysia, and Japan. Growth is expected to be majorly contributed by economic and industrial activities associated with logistics services such as transportation of goods & warehousing. The country is concentrating in expanding & developing its logistics infrastructure such as intermodal connectivity, logistics parks, and ports, which are expected to create more business opportunities in Saudi Arabia. KSA government aims to aggressively drive and position 50 islands and 100 miles of Red Sea as a global tourist destination. The expansion of Red Sea corridor in Jeddah, the minerals hub in Yanbu, King Abdullah port and NEOM project are also expected to drive the freight forwarding industry. During COVID pandemic, cargo was backlogged at KSA’s major container ports, travel restrictions led to a shortage of truck drivers to pick up containers, and ocean carriers canceled sailings. All passenger flights remain suspended, causing capacity constraints. However, commercial aircraft are operating to carry freight and freighter schedules have been ramped up. Saudi customs authority has restricted freight forwarders to only two brokers from each company at all ports of entry, which is causing delays in freight clearances. Free time has been extended in all air and seaports to 10 days from freight arrival.

Saudi Arabia Dry Warehousing Market:

Warehousing industry ecosystem is dominated by domestic companies in terms of warehousing space, followed by international companies. Ecosystem has underscored asset monetization deal with Real Estate developers purchasing the warehousing assets to generate current income under operating lease model to warehousing operators. Most of the warehouses are concentrated in Jeddah, Riyadh and Dammam in Saudi Arabia. The major Companies include LSC logistics, Almadjioue Logistics, Mosanda Logistics, Tamer, Agility, GAC, GSL and others. Construction Materials / Industrial end user dominated in terms of warehousing revenue followed by retail, healthcare, F&B, automotive and others in 2019. Industrial warehouses dominated in terms of dry warehousing revenue and have a regional concentration in Riyadh, Jeddah, Dammam and Al-Khobar. With increasing construction of warehousing hubs, the warehousing sector has presented real estate companies (especially office & retail) with multiple opportunities owing to their high need for high-quality & automated facilities to carry a smooth supply chain process. Real estate companies were observed to dominated in terms of overall warehousing space during 2019 followed by captive companies and logistics companies. Warehousing within Jeddah region has been undergoing a major redevelopment, driven by government’s objective to increase industrial contribution towards GDP. Jeddah region dominated in terms of overall warehousing space in 2019 followed by Riyadh, Dammam, Al-Khobar and others. Strong demand is anticipated for full-fledged integrated centers that include new-generation logistics facilities (built-to-suit automation model) along with the emergence of 3PL companies that handle stock distribution for companies with large and sophisticated supply chains. Various reforms introduced by the KSA government under the Kingdom’s Vision 2030 and increased participation of the private sector are expected to increase trade therefore, contributing towards warehousing requirements in future. During COVID-19 pandemic, large areas of warehousing lands are occupied by an aging supply of conventional warehouses. KSA market rents dropped by 10-15%, with an average lease rates for conventional warehouse dropping in 2020. Future supply is expected to be limited as developers delay development of new projects until market conditions progress.

Saudi Arabia Customs Clearance Market

Introduction to concept of E-filing of documents has significantly reduced the average time for customs clearance even before the docking of the vessel. Majority of Saudi Customs declarations are now cleared within 24 hours. Increased participation from local Saudi operators as they enjoy complete / full revenue sharing i.e. no regulatory constraints for domestic players and they can perform customs clearance operations on their own. Customs clearance revenue via air mode took a fall due to limited air freight movement leading to decline in shipments via air. It is further expected to go down in the near future as air freight mode is quite expensive compared to sea. Jeddah Islamic Port captures majority of total transshipment containers (discharged and loaded) in 2019 therefore, making it the transshipment hub of the Kingdom. With Red Sea on one side & the Gulf on the other side of KSA, both Jeddah Islamic Port and King Abdul Aziz Port are placed at strategic locations. Transhipment cargo volumes are driven by overseas ports in GCC region including UAE and Bahrain. Majority of containerized transshipment cargo was done via Jeddah Islamic port in 2019 and the remaining via King Abdulaziz Port in Dammam during the year 2019. Dammam Port has heavy port congession when compared other commercial sea ports in KSA owing to its large area.

Comparative Landscape in Saudi Arabia Dry Logistics and Warehousing Market

Competition was again observed to be highly fragmented in both freight forwarding and warehousing segment along with the presence of both international and domestic players. Nevertheless, the local / domestic players have a larger presence in the market and were observed to compete on the basis of key clientele, revenue matrix, logistics networking, average pricing, technological advancement and value added services.

Saudi Arabia Dry Logistics and Warehousing Market Future Outlook and Projections

Continued progress towards economic diversification should continue to reduce the economy’s reliance on hydrocarbons. The government also plans to pump investment into economic cities and other industrial projects to boost logistics and transportation centers. The KSA government is highly promoting the integration of multi-modal hubs across the country. FDI within the logistics infrastructure development, constructing regional & international logistics service centres and improving the efficiency of trade routes can collectively help the country in becoming a hub over long term. The KSA government’s preference towards domestic and foreign based contracting firms has promoted competition in the logistics segment. In order to attract new investments, the government is willing to open its project and tender market to qualified regional and international firms. Development of New Economic Zones / Cities such as KAEC to attract foreign investments by providing special incentives is another program by KSA government. The economic cities are planned to be located near to sea ports and major consumption bases, which is expected to bring manufacturing closer to these bases.

Key Segments Covered in KSA Dry Logistics Market:-

Service Mix

Freight Forwarding

Warehousing

Value Added Services

Regions:-

Jeddah

Riyadh

Dammam

Rabigh

Others (Al- Khobar, Medina, Tabuk and several other cities)

KSA Dry Freight Forwarding Market:-

Mode of Freight

Road Freight

Air Freight

Sea Freight

Rail Freight

International and Domestic Freight

Road Freight

Air Freight

Sea Freight

International and Domestic Companies

Flow Corridors (International Freight)

Asian Countries

European Countries

Middle East

NAFTA (North American Free Trade Agreement)

Other Regions (Africa and South America)

KSA Dry Warehousing Market:-

Business Model

Industrial / Retail

Container Freight / Inland Container Depots

End Users

Construction Material / Industrial

Consumer Retail

Food and Beverage

Healthcare

Automotive

Others (Agriculture, Chemicals and Rest)

Entities

Real Estate Companies

Captive Companies

Logistics Companies

Cities

Jeddah

Riyadh

Dammam

Others (Al-Khobar, Medina, Tabuk and other cities)

KSA Customs Clearance Market:-

Overall Value Added Services

Customs Clearance Revenue by Sea

Customs Clearance Revenue by Air

Transhipment Cargo Volume

Discharged Transhipment Containers

Loaded Transhipment Containers

Key Target Audience:-

International Domestic Freight Forwarders

Warehousing Companies

Logistics Companies

Logistics Consultants

Time Period Captured in the Report:-

Historical Period: 2014-2019

Forecast Period: 2019–2025

Companies Covered:-

Karsf

LSC

JAS

Arabco

Mubarrad

Bahri

Defaf logistics

Wolf Logistics

Namma Cargo

Almajdieou

Al Ayed

Agility logistics

Four winds logistics

Globus Logistics

Space logistics

Atlas world

Uniworld Freight Services

Hellman

BAFCO International Logistics and Shipping Co.

Hala Supply Chain

RAZ

Gulf system

Platinum shipping and logistics

MSC

OCSCL (Oriental Commercial & Shipping)

NTF Group

Abdui Global

Al rashed

GAC

Kanoo terminal Services

Online Retail Companies Covered:-

Carrefour

Panda Retailing

Abdullah Othaim Market

Danube

Tamimi Market

Lulu Hypermarkets

Key Topics Covered in the Report:-

Saudi Arabia Overview and Major Economic Zones

Saudi Arabia Dry Logistics and Warehousing Market

Trade Scenario

Saudi Arabia Dry Freight Forwarding Market

Saudi Arabia Dry Warehousing Market

Snapshot on Saudi Arabia Customs Clearance and Transhipment Market

Industry Analysis (Decision Making Process, SWOT Analysis, VAT Impact and Law of Public Transport on Roads of KSA)

Cost of Setting up a Logistics Business in Saudi Arabia

Comparative Landscape – KSA Dry Logistics Market

Comparative Landscape in Saudi Arabia Online Retail Market

Recommendations / Success Factors

Research Methodology

Appendix

Related Reports:-

https://www.kenresearch.com/automotive-transportation-and-warehousing/logistics-and-shipping/philippines-logistics-market-outlook-to-2024/342232-100.html

https://www.kenresearch.com/automotive-transportation-and-warehousing/logistics-and-shipping/india-road-freight-market-outlook/338096-100.html

Contact Us:-

Ken Research

Ankur Gupta, Head Marketing & Communications

[email protected]

+91-9015378249

Ken Research Pvt. Ltd.,

Unit 14, Tower B3, Spaze I Tech Business Park, Sohna Road, sector 49 Gurgaon, Haryana – 122001, India

Ken Research is a Global aggregator and publisher of Market intelligence, equity and economy reports. Ken Research provides business intelligence and operational advisory in 300+ verticals underscoring disruptive technologies, emerging business models with precedent analysis and success case studies. Serving over 70% of fortune 500 companies globally, some of top consulting companies and Market leaders seek Ken Research’s intelligence to identify new revenue streams, customer/ vendor paradigm and pain points and due diligence on competition.

This release was published on openPR.