Written by Nick Ackerman, co-produced by Stanford Chemist

The RiverNorth Opportunities Fund (NYSE:RIV) is a highly diversified fund as it invests with a “fund of funds” approach. It is also starting to have quite a history with double-digit yields. Based on inception in late-2015 and spending a large portion of that time offering a high level of distributions. That can be perfect for an income investor. The caveat here is that the fund’s NAV has also declined some since it launched in 2015. The NAV per share at launch was $19.36, and today, NAV stands at $15.18. Of course, this wasn’t helped any by the pandemic sell-off earlier this year.

RIV has an investment objective of “total return consisting of capital appreciation and current income.” As we just highlighted, the returns have come from income and not capital appreciation at this time.

It “employs a tactical asset allocation strategy primarily comprised of both closed-end funds and exchange-traded funds. RiverNorth implements an opportunistic investment strategy designed to capitalize on the inefficiencies in the closed-end fund space while simultaneously providing diversified exposure to several asset classes.”

Essentially it is managing the fund just like any other CEF investor out there. Its portfolio just happens to have ~$153 million to manage. The fund also utilizes leverage but sparingly. The fund notes that it won’t go over 15%. This can be important because the fund’s underlying positions can also utilize leverage, essentially – leverage on leverage.

Speaking of that, the other “problem” with a fund of funds is that it also means fees on fees. That’s why it is important to keep expenses low for these types of funds. RIV has some room for improvement here as its expense ratio comes in at 1.56%. In other funds, this would be reasonable, but their underlying positions will have expense too – creating a “drag” of performance. The Cohen & Steers Closed-End Opportunity Fund (NYSE:FOF) in comparison charges a much lower 0.96%.

The payoff for RIV is that it also invests quite a significant portion outside of CEFs. Other investment vehicles include SPACs, investment company bonds and BDCs. BDCs are a type of closed-end fund but operate fairly differently than “traditional” CEFs.

(Source)

Performance

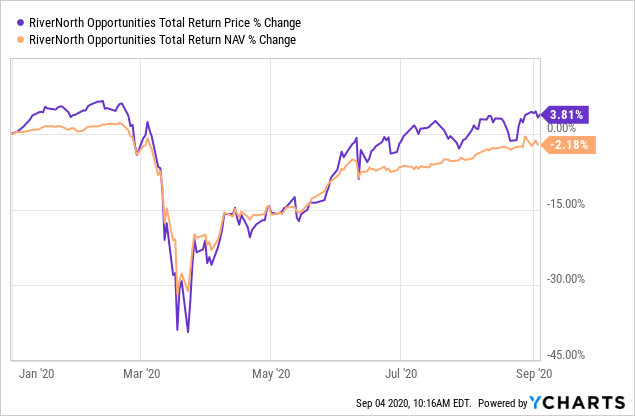

On a YTD basis, the fund wasn’t immune to the black swan COVID-19 event that sent markets tumbling in March. With that being said, it clawed a large portion of this back. More impressively, it didn’t manage this by having a large allocation to the tech sector. That can be important as tech is certainly a healthy long-term bet, but over the shorter term is looking quite lofty.

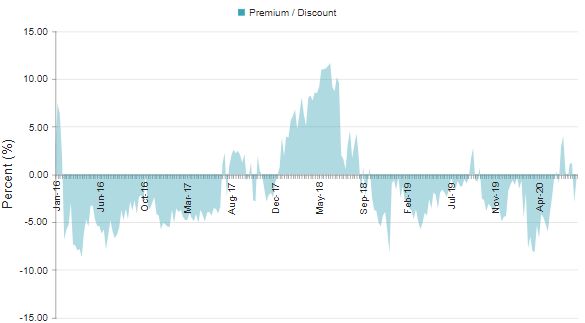

As we can see above, RIV’s share price has been outpacing its NAV price recently. This has led to a slight premium of 0.59%. The one-year average of this fund is at -2.47%. Based on these numbers, this puts the one-year z-score at 0.97. Longer term, the three-year average discount of the fund is -0.37%. Based on these averages, this fund has traded near par. Getting the fund at even a small discount can be attractive.

(Source – CEFConnect)

Over the longer term, if we are being honest, RIV hasn’t been able to put up great numbers. Perhaps we can give it some slack as it launched at the end of 2015. That means it wasn’t too long before it hit the sell-off of 2018 and now the black swan event of 2020. The fund also invests with a greater emphasis on fixed-income positions. Which makes it interesting, as it lists performance against the S&P 500.

(Source – Fund Website)

Its last reported quarterly performance is above. Since its inception, for a fixed-income focused fund, performance has been reasonable. Even more, the three-year annualized numbers are going to start looking poor for a broader range of funds as well. Not making excuses, but the markets weren’t exactly rosy in 2018 and this year. Meaning that of the annualized period two of the three years in that time was rough for most investments.

Double-Digit Distribution Yield – But Coverage Is Lacking

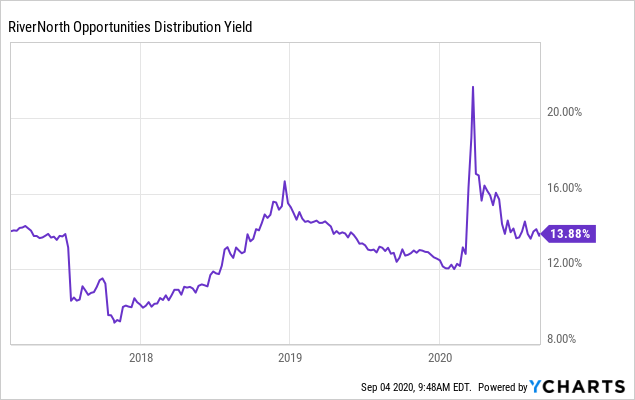

The main focus for most investors will be the over 14% distribution rate the fund is currently sporting. Additionally, it just announced the same $0.18 per month through the end of the year. Income investors won’t have to face any surprises, at least through 2020.

(Source – CEFConnect)

Another focus for income investors is that RIV has spent most of its operating time with a distribution yield of over 10%. There was a brief period in 2017 when it dipped below this level for a short period.

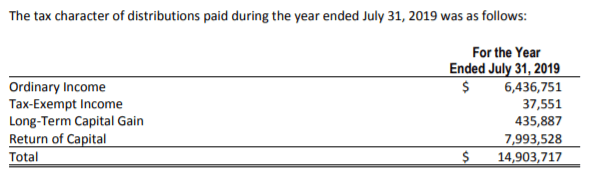

Of course, the main caveat here is that the fund hasn’t been able to support these levels either. The fund has had to resort to destructive ROC to maintain these rates.

Its last Semi-Annual Report available was for the period ending January 31st, 2020. That puts it about as close to the top of the market that you can get. February 19th, 2020, was when the market started its tumble.

(Source – Semi-Annual Report)

Its NII coverage stood at just over 38% for those six months. That was a huge improvement from its prior full-year reporting period. As a fund that leans heavier in fixed-income, though, I would generally like to see this higher. We also see that it was trimming some losers as it reported net realized losses.

We can also take a look at its capital share transactions. Since the fund trades at premium levels, its DRIP means new shares are issued on occasion. It also conducts rights offerings fairly regularly. Some investors view those as a hassle and a disruption that they would rather not deal with. I’ve held RIV shares in the past and November 2019 was the last RO. I held through that period and sold my rights as they were transferrable.

However, at the CEF/ETF Income Laboratory, we generally sell out of positions that announce rights offerings. This has worked out well as funds face selling pressures due to dilution. Historically, this has meant a better price to pick up shares at a later date. While for that particular time I held through, I ultimately sold the position in the subsequent bounce in January.

For the prior year, ROC was a large part of the fund’s tax classification. This was destructive ROC too, as the NAV declined in that period. Thanks to an overall poor performance at the end of 2018 across most investments.

(Source – Semi-Annual Report)

Holdings

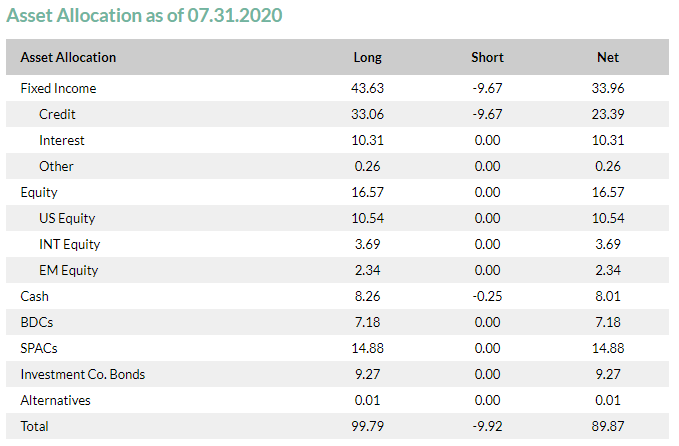

As previously mentioned, RIV isn’t just a fund of CEFs – it includes other investment vehicles as well.

(Source – Fund Website)

Of note, the SPAC market has been quite spectacular this year. SPACs have been particularly popular with companies going public, rather than the traditional IPO way. At almost 15% of its portfolio, it has certainly taken notice. The last time I covered this fund, it was at only 10% of its portfolio.

While the fund still has an emphasis on fixed-income exposure, it has pared this back a bit since that previous coverage. Equity positions have been reduced as well. This accounts for some of the shift to SPACs, but also BDCs and investment company bonds (which would be fixed-income) have increased.

(Source – Fund Website)

Investment-grade makes up almost 28% of its fixed-income portfolio, followed by high-yield at almost 36% and debt that isn’t rated at around 36% as well. The other interesting note here is that bank loan CEFs make up the largest portion of its portfolio at 24.14%.

This does make sense because of the extremely large discounts we are seeing in that space. Of course, it comes on the back of the Fed lower interest rates to a target of 0%. As floating rate investments, the income from these will take a hit. Rates aren’t anticipated to go anywhere soon either, meaning potentially years before these investments might pay off. Though, they can also provide a LIBOR floor for how low they can go too. Stanford Chemist has discussed this in-depth previously.

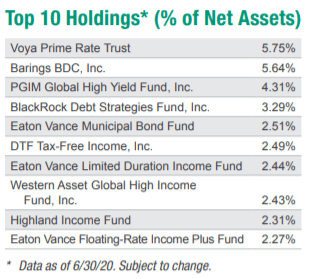

The fund last reported its top 10 holdings as of 6/30/2020 in the Fact Sheet. This can differ a bit since it updated asset allocations and CEF classifications. At that time, it still had 21.27% in CEFs classified as bank loans. So, over the last month, this portion has increased. With that out of the way, we can take a look at those CEFs last reported in its top ten.

(Source – Fact Sheet)

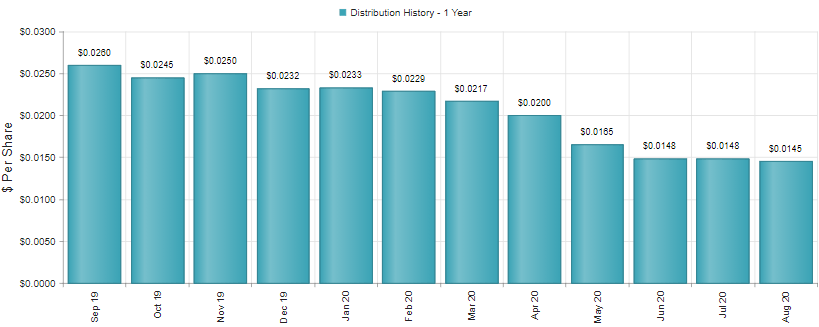

Voya Prime Rate Trust (NYSE:PPR) comes in at the top of the list at 5.75%. PPR trades at a nearly 8% discount. Which isn’t actually as steep as some of the other senior loan funds out there. With PPR, we can see quite clearly what lower rates have meant for the fund’s distribution.

(Source – CEFConnect)

While the fund made small adjustments month to month, starting in March, it started quite an aggressive downtrend of cuts. Since then, it has flattened back out again.

PPR also has some activists in the fund, Saba Capital owns nearly 21% of the outstanding shares. In fact, Saba has gained control of the whole Board of Trustees for PPR. Shareholders also voted in favor of a proposal for a 40% tender offer. That would be quite huge and is the primary reason that PPR’s discount is trading where it is. Though that still leaves quite a significant amount of upside for investors in PPR, which includes RIV.

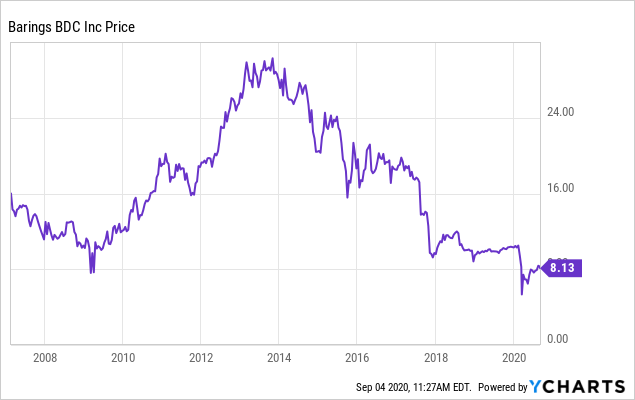

Its second-largest holding is Barings BDC (NYSE:BBDC). It is an externally managed BDC “that primarily makes debt investments in middle-market companies.” Barings more broadly manages over $346 billion in various funds and offerings, making it a rather respected firm.

Most BDCs have been struggling through 2020. Since they generally back small- to medium-sized businesses, that puts them right in the territory that has been mostly struggling due to pandemic-related issues. That is whether it be supply chain disruptions or just plain not being able to operate during lockdowns. Though it appears BBDC has been struggling for several years before the latest events.

The latest news from BBDC though is that it is merging with another BDC – MVC Capital (NYSE:MVC). Presumably, RIV managers see this as a good thing as they have taken their position from around 3% to 5.64%. The merged BDC will have more than $1.2 billion in investments.

BBDC’s latest earnings report saw NII of $0.14 marking a drop from $0.15 the prior year. The small decrease was sheltered by a significant drop in total operating expenses; primarily the decreases were from interest and other financing fees, plus general and administrative expenses decreased some. The total investment income was a drop of 17.7% from Q2 the prior year.

Besides the merger that BBDC is involved with, the discount on this BDC is also quite extreme. In that June 30th earnings release, NAV per share was $10.23. As of the latest close, the market price was $8.14. That puts the discount at a steep 20.43% discount – if the NAV hasn’t moved since. As virtually everything has appreciated over the last couple of months, it would seem appropriate that BBDC’s NAV has risen since too.

Conclusion

RIV’s most alluring feature is the high distribution yields that it has offered investors for a considerable amount of time since its launch. This can be a huge benefit for income investors. It has now announced through the end of the year as well, leaving investors with four months without having to worry about any surprises. With that being said, the high distribution has resulted in some of the fund’s erosion over the last few years.

These high distributions have also meant that investors have historically bid the price up to premiums or near par levels. That is the case now, with RIV at a slight premium. Though, if you can get this fund at a discount, it is worth adding it to your portfolio in a high-income sleeve.

The fund managers haven’t been shy about rights offerings. This can be frustrating for investors who don’t like the short-term volatility that can result from these events. With that being said, it can also create some opportunities to trade around them. One could also just sell the rights they have received if they are transferable – almost like creating your special distribution.

Overall, RIV’s high-double-digit yield isn’t a “free lunch.” It hasn’t been able to earn it thus far. I believe that makes it more appropriate for a high-income portion of your investment portfolio. Appropriate in a higher-risk category as NAV can continue to erode – though ROs can potentially kick that can down the road if it is accretive.

Profitable CEF and ETF income and arbitrage ideas

At the CEF/ETF Income Laboratory, we manage ~8%-yielding closed-end fund (CEF) and exchange-traded fund (ETF) portfolios to make income investing easy for you. Check out what our members have to say about our service.

At the CEF/ETF Income Laboratory, we manage ~8%-yielding closed-end fund (CEF) and exchange-traded fund (ETF) portfolios to make income investing easy for you. Check out what our members have to say about our service.

To see all that our exclusive membership has to offer, sign up for a free trial by clicking on the button below!

Disclosure: I am/we are long FOF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.