onurdongel/iStock via Getty Images

Elevator Pitch

I raise my investment rating for Plug Power Inc.’s (PLUG) shares from a Hold to a Buy. My prior initiation article for Plug Power was published on September 30, 2021.

I focus on Plug Power’s outlook this year in this latest article. I see increased revenue and narrower operating losses for PLUG in 2022, and its current valuations are attractive as compared to peers. This is why I have turned bullish on the name.

Where Is PLUG Stock Headed In 2022?

Heading into 2022, PLUG stock is expected to deliver higher revenue and narrower losses.

Market consensus sees Plug Power’s top line expanding by +80% YoY from $499 million in fiscal 2021 to $899 million in FY 2022, according to sell-side financial estimates sourced from S&P Capital IQ. Wall Street also forecasts that PLUG’s losses at the non-GAAP adjusted EBITDA level will narrow from -$180 million last year to -$17 million in the current year.

The sell-side analysts’ financial forecasts are in line with management guidance.

In the company’s most recent Q3 2021 shareholder letter, Plug Power highlighted that it was “raising revenue guidance for 2022 given acquisitions and commercial traction to $900 million-$925 million.” The sell-side’s consensus 2022 revenue forecast ($899 million) is at the lower end of the company’s top-line guidance.

Although PLUG did not provide EBITDA guidance for 2022, the company had earlier set a target of achieving positive non-GAAP adjusted EBITDA of $250 million in 2024. Wall Street’s consensus 2024 adjusted EBITDA estimate is even higher at $320 million.

In my opinion, the market’s revenue and EBITDA expectations for Plug Power this year are realistic.

Plug Power indicated at the company’s Q3 2021 earnings call that its expected $925 million (upper end of guidance) revenue for 2022 will be comprised of $600 million from material handling, $150 million in electrolyzer sales, $100 million from M&A, and $75 million generated by new markets.

PLUG recently secured five new clients for its material handling business, which it noted was “well ahead of target” in its third-quarter shareholder letter. Separately, Plug Power ventured into the electrolyzer business in mid-2020 when it acquired Giner ELX, which it refers to as a company with “one of the most experienced teams in the world in Proton Exchange Membrane (PEM) electrolysis.” PLUG is targeting electrolyzer sales in excess of 100MW to support its $150 million electrolyzer revenue guidance.

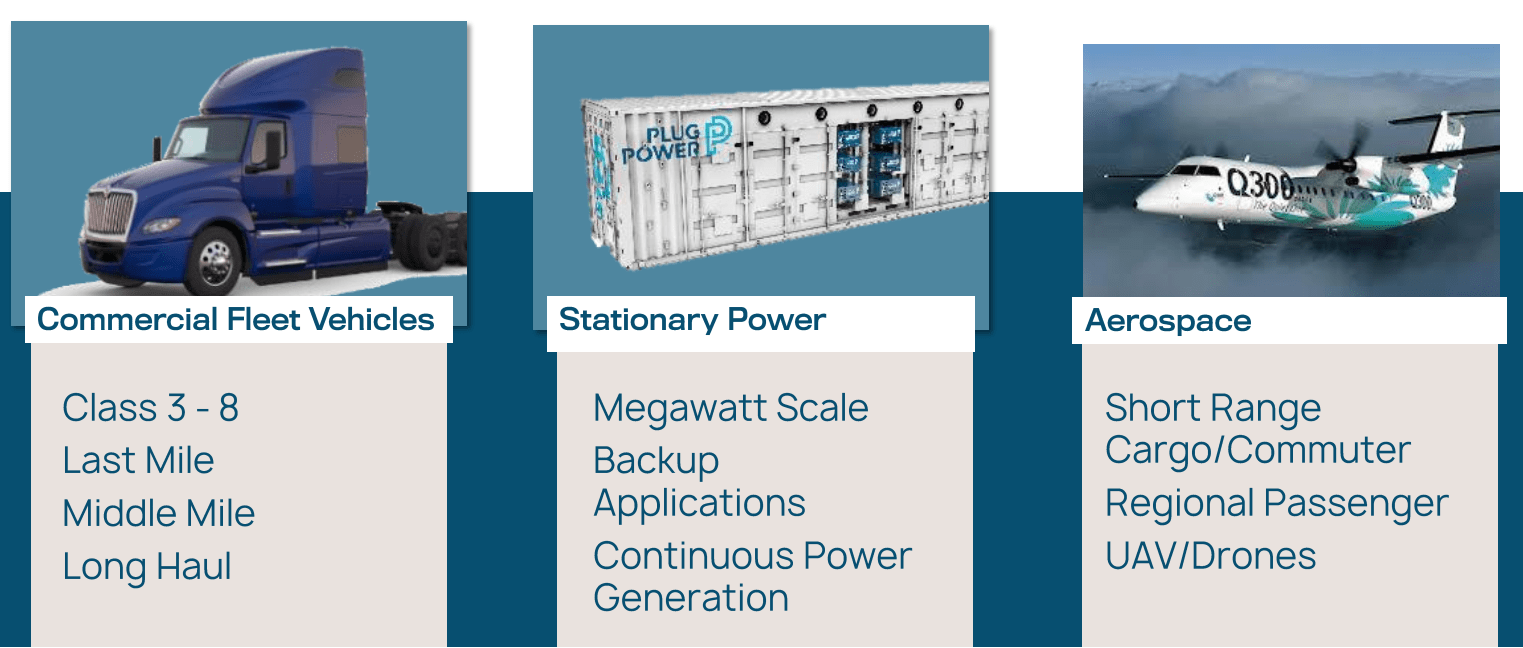

Inorganic growth and new markets are also key drivers of Plug Power’s expected +80% jump in revenue this year. Plug Power bought out Applied Cryo Technologies on November 23, 2021, which it describes as a “provider of technology, equipment and services for the transportation, storage and distribution of liquefied hydrogen.” PLUG subsequently concluded the acquisition of Frames Group on December 9, 2021, which was called “a leader in turnkey systems integration for the energy sector” in its media release. Also, Plug Power has found new market applications for what it refers to as its “ProGen platform of modular fuel cell engines”, as per the chart below.

New Market Applications For PLUG

In terms of narrowing operating losses, the key driver is Plug Power’s guidance that “Q4 2022 hydrogen costs” are expected to be “over 20% lower than Q4 2021” as indicated in its Q3 2021 shareholder letter. At its Q3 2021 results briefing, PLUG also highlighted that “we plan to have about four of these hydrogen plants basically being commissioned” by end-2022. This explains why there is expected to be a “meaningful margin improvement from Q4 of this year (2021) to Q4 2022.”

Is PLUG Stock Expected To Rise?

PLUG’s stock price is expected to rise in the near term, as there is a high probability of the company raising this year’s revenue guidance again soon.

As highlighted earlier, Plug Power’s stock price reached a new five-month high of $44.55 as of November 19, 2021. This came 10 days after PLUG released its Q3 2021 results and increased its 2022 top-line guidance as outlined in the preceding section.

There is a very good chance that PLUG’s revenue could surprise on the upside this year, and the key factor is electrolyzer sales.

Plug Power noted at the company’s third-quarter investor call that its 2022 electrolyzer revenue “could be more” than its current $150 million guidance. The company’s confidence in higher-than-expected electrolyzer lies with its knowledge of “the deal flow and the activities we have going on” as per its comments at the recent Q3 briefing.

Specifically, PLUG revealed earlier in mid-October 2021 that it “signed a letter of intent for a 50-50 joint venture to build a Gigafactory in Queensland, Australia” with “Fortescue Future Industries Pty Ltd.” As this transaction has not been completed, it has yet to be factored into Plug Power’s 2022 revenue guidance of $900 million-$925 million and electrolyzer sales amounting to $150 million.

What Is Plug Power Stock’s Price Target?

Plug Power last traded at $23.91 as of January 13, 2021. The average Wall Street analyst target price for Plug Power is $46.63 at the time of writing, and this suggests a capital appreciation potential of +95% for the company’s shares which appears to be supported by PLUG’s relative valuations.

On a relative valuation basis, Plug Power’s consensus forward FY 2023 Enterprise Value-to-Revenue multiple of 8.8 times is the lowest among its peers, despite the fact that its expected top-line expansion and gross profitability in the next two years are comparable with that of its peers.

Peer Valuation Comparison For Plug Power

| Stock | Consensus Forward One Year Enterprise Value-to-Revenue Multiple | Consensus Forward Two Years Enterprise Value-to-Revenue Multiple | Consensus Forward One Year Revenue Growth Rate | Consensus Forward Two Years Revenue Growth Rate | Consensus Forward One Year Gross Profit Margin | Consensus Forward Two Years Gross Profit Margin |

| Plug Power | 12.8 | 8.8 | +80.2% | +52.4% | 15.1% | 21.7% |

| FuelCell Energy, Inc. (FCEL) | 12.2 | 10.1 | +109.9% | +20.9% | 9.4% | 14.0% |

| Ballard Power Systems Inc. (BLDP) | 17.7 | 12.2 | +24.7% | +53.2% | 18.4% | 20.9% |

Source: S&P Capital IQ

In conclusion, I think there is a meaningful upside for PLUG at current price levels. Plug Power should be able to see an expansion of its forward Enterprise Value-to-Revenue multiples into the mid-teens at the very least, for a company growing its top line at more than +50% and showing signs of improved profitability.

Is PLUG Stock A Buy, Sell, Or Hold?

PLUG stock is a Buy, as its valuations should re-rate on higher sales and narrower losses at the EBITDA level this year. A short-term catalyst is a potential rise in the company’s FY 2022 revenue guidance associated with higher-than-expected electrolyzer sales linked to the proposed joint venture with Fortescue Future Industries.