Galeanu Mihai/iStock via Getty Images

Introduction

Following five painful years with three separate distribution reductions, the outlook for a return to distribution growth was finally looking up for Plains All American Pipeline (NASDAQ:PAA) during late 2021, as my previous article discussed. Thankfully their management recently announced an intention to increase their distributions that if approved by the board, stands to lift their distribution yield to a high 8.05%. This article provides a follow-up analysis that reviews their subsequently released fourth quarter of 2021 results and more importantly, their guidance for 2022 that excitingly now sees a new era of distribution growth beginning.

Executive Summary & Ratings

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Author

*Instead of simply assessing distribution coverage through distributable cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and also best captures the true impact upon their financial position.

Detailed Analysis

Author

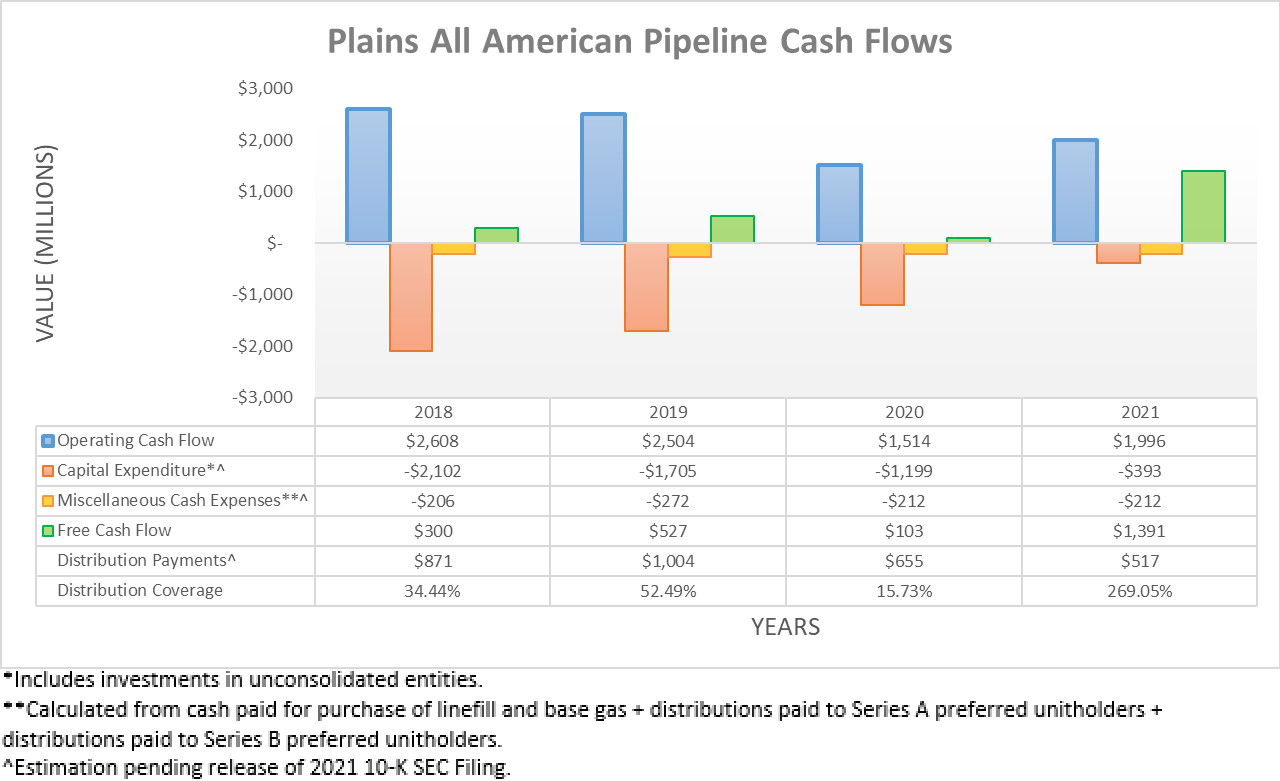

Now that 2021 sits in the rear-view mirror, it shows that their cash flow performance continued recovering throughout the fourth quarter of 2021 and ultimately ended the year at $1.996b, thereby representing a very impressive 31.84% increase year-on-year versus their previous result of $1.514b during 2020. This actually marks a very surprising improvement versus the lacklustre outlook earlier in 2021 that was discussed within my other article, whereby their operating cash flow was expected to suffer during 2021 versus 2020 due to their original guidance for the former seeing their adjusted EBITDA at only $2.15b, which would have been down 16.01% year-on-year versus their result of $2.56b during 2020, as per slide nine of their fourth quarter of 2020 results presentation.

Thanks to their considerably lower capital expenditure, they finally produced enough free cash flow to completely cover their distribution payments for the first year ever and in fact, it actually landed at 269.05% and thus provided very strong coverage and thus well above their very weak 15.73% to 52.49% coverage throughout 2018-2020. When looking ahead at their guidance for 2022, thankfully this fundamental shift appears set to continue, albeit with one slight negative caveat, as the graph included below displays.

Plains All American Pipeline Fourth Quarter Of 2021 Results Presentation

When looking at their guidance for 2022 cash flow performance, it shows that they are forecasting that their operating cash flow will increase to circa $2.1b, which represents a modest increase of circa 5% year-on-year versus 2021. Although positive, the slight negative caveat is their distributions to non-controlling interests, which are forecast to increase significantly from virtually nothing during 2021 to several hundred million dollars, based upon their approximate relative scale to other known variables since no exact guidance appears to have been provided. These appear to be coming about due to management rearranging their business segments to “Crude Oil” and “NGL” versus their three previous business segments that were “Transportation”, “Facilities” and “Supply & Logistics”, thereby affecting how various joint ventures are reported within their financial statements, as per the commentary from management included below.

“To open my portion of the call, I will share a few comments on our new crude oil and NGL reporting segments as well as the treatment of non-controlling interests within our reporting. Our new segments are reflective of how we view and run our integrated crude oil and NGL systems, aggregating supply from producers, delivering to end market demand and all the steps in between. We believe the new segments will provide better visibility and transparency into the drivers of our overall business and reduce intersegment activity.”

-Plains All American Pipeline Q4 2021 Conference Call.

Their management went on to discuss various relating details regarding this topic during their fourth quarter of 2021 results conference call that readers can review themselves if interested, as they would be unnecessarily longwinded to include within this article. At the end of the day, the exact accounting principles behind the scenes are not necessarily of the highest importance for investors, rather the bottom line implications are more important and put simply, these distributions to non-controlling interests weigh down the actual operating cash flow that is attributable to their unitholders.

This situation means that whilst their operating cash flow is forecast to increase by circa 5% year-on-year during 2022, after these estimated distributions to non-controlling interests are removed, it effectively becomes only circa $1.9b and thus in a practical sense, would be down circa 5% year-on-year. Whilst less than stellar, at least they should still have ample free cash flow to cover their distribution payments since even after subtracting their forecast net capital expenditure guidance of $485m, it still leaves approximately $1.4b or more aptly, it leaves approximately $1.2b of estimated free cash flow for 2022 after subtracting their preferred distributions of $198m per annum. Since their distribution payments only amounted to $517m during 2021, this should obviously not only see their very strong coverage continue during 2022 at over 200% but also provide scope to easily fund their intended upcoming higher distributions, as per the commentary from management included below.

“Based on the progress we’ve made to-date and our expectation of generating meaningful cash flow over the next number of years, we intend to recommend to our Board an increase in our annualized distribution of $0.15 per common unit, which, based on our guidance, maintains the capacity for continued discretionary repurchase activity.”

-Plains All American Pipeline Q4 2021 Conference Call (previously linked).

Whilst it technically remains possible that their board does not approve the higher distributions, this seems very unlikely in my view given that an exact amount has already been publicized. If their annual distributions increase by $0.15 per unit, it would represent a very solid 20.83% increase to their current annual distributions of $0.72 per unit. This will obviously not subtract significantly from their distribution coverage because at over 200%, it could theoretically handle their distributions being doubled and thus even if their cash flow performance never increases in future years, there are still prospects to see further distribution growth in the coming years.

Author

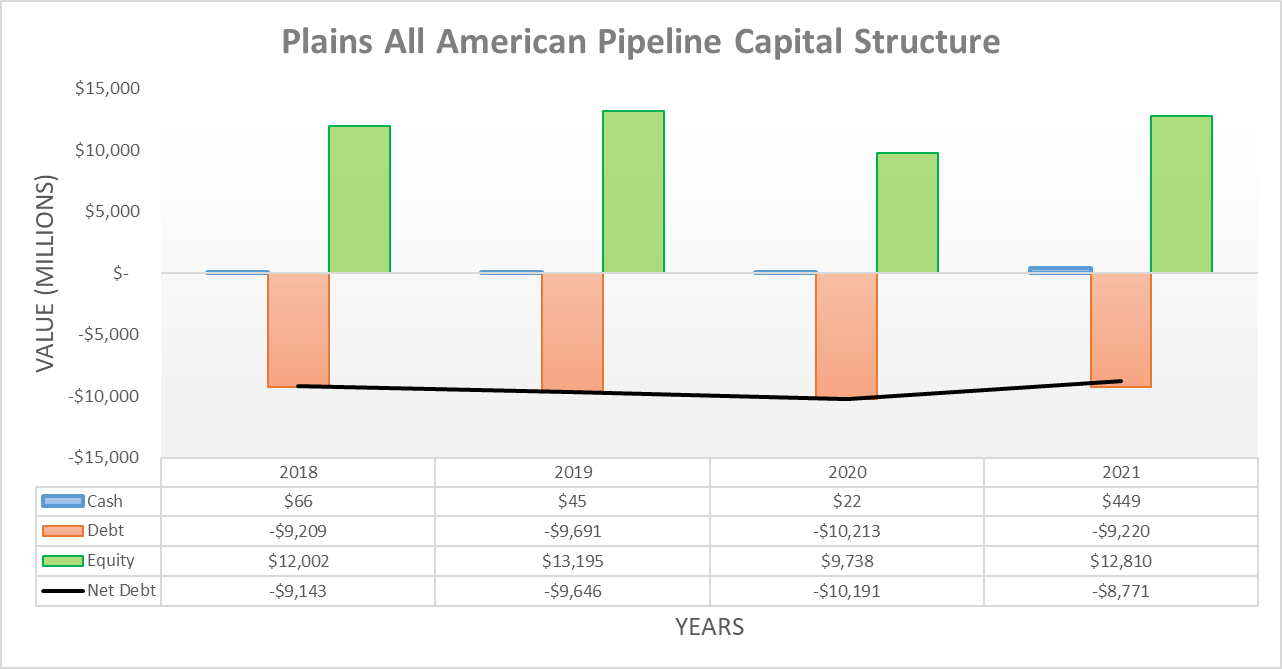

Thanks to their continued recovering cash flow performance during the fourth quarter of 2021, their net debt continued sliding lower and ended the year at $8.771b, which is down versus its previous level of $9.005b at the end of the third quarter and thus now sees a solid decrease of 13.93% year-on-year versus its level of $10.191b at the end of 2020. When looking ahead, their previously discussed guidance for 2022 also indicates that approximately 75% of their estimated $700m of free cash flow after distribution payments and divestitures will be directed towards deleveraging, which amounts to approximately $525m and thus 2022 should see a decent decrease of circa 6% year-on-year versus the end of 2021.

Author

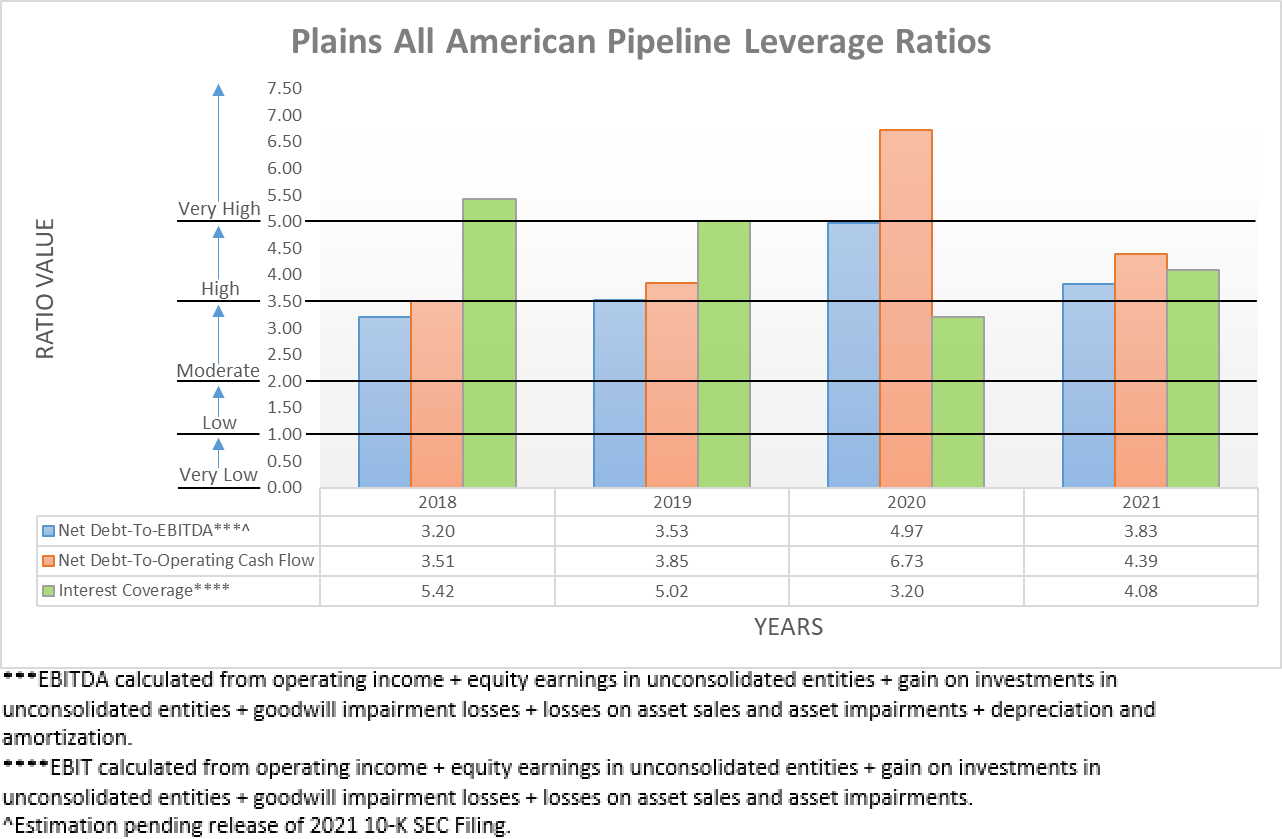

After seeing their net debt decrease throughout the fourth quarter of 2021, it was only natural to see their leverage decrease in tandem with their net debt-to-EBITDA and net debt-to-operating cash flow now sitting at 3.83 and 4.39 respectively, thereby down from their previous results at the end of the third quarter of 4.26 and 4.73 respectively. Whilst they are still within the high territory of between 3.51 and 5.00, at least they are no longer floating around the very high territory like at the end of 2020 when their respective results were 4.97 and 6.73.

When looking ahead, their leverage should continue heading lower during 2022, although since their accrual-based earnings guidance for 2022 sees their adjusted EBITDA coming in at $2.2b and thus essentially flat versus their result of $2.196b during 2021, it leaves any deleveraging reliant upon lower net debt. Since their guidance implies that their net debt will only decrease by circa 6% year-on-year during 2022, the difference to their leverage will be comparable. Whilst it would be preferable to see more significant deleveraging, their high leverage is not necessarily problematic nor impedes their ability to increase their distributions given the stable nature of the midstream industry, especially with their net debt-to-EBITDA already sitting within the lower half of the high territory.

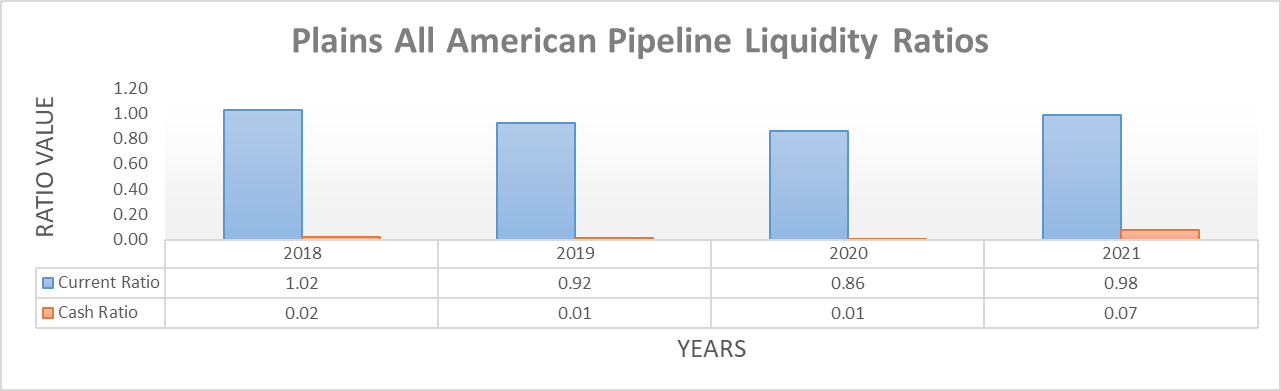

Upon looking elsewhere, their liquidity has not changed materially following the fourth quarter of 2021 with their respective current and cash ratios of 0.98 and 0.07 only seeing a slight improvement versus their previous respective results of 0.90 and 0.04. Naturally, this means that their liquidity is still adequate and thus given the lack of changes, it would be redundant to reassess this aspect in detail but if any new readers are interested, please refer to my first previously linked article.

Author

Conclusion

Whilst their essentially flat guidance for 2022 is anything but ground-breaking nor stellar, thankfully it nevertheless still sees their distributions increasing by slightly over 20% whilst they also deleverage slightly further. This still makes for a desirable combination for income investors and thus with their distributions beginning a new era of growth thanks to their very strong coverage, it should be no surprise that I believe maintaining my buy rating to be appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Plains All American Pipeline’s SEC filings, all calculated figures were performed by the author.