da-kuk/E+ via Getty Images

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 7th, 2022.

High Income Securities Fund (NYSE:PCF) is an interesting fund that is managed by Bulldog Investors. It came about in a similar way that Saba Capital had taken over Saba Capital Income & Opportunities Fund (BRW), which was previously a Voya fund. Essentially, the activists here pushed the previous fund sponsors to abandon these funds. This isn’t necessarily a negative, but it does mean that current shareholders at the time would be invested in a different fund going forward.

For PCF, it was formerly known as Putnam High Income Securities Fund until the name change in 2018 dropped the “Putnam” portion. Since then, Bulldog Investors has essentially transformed it into a fairly attractive multi-asset investing fund. The investments in other closed-end funds mean they offer plenty of diversification. It also means that investors can get discounts on discounts. That’s an important part of what makes PCF particularly interesting at this time.

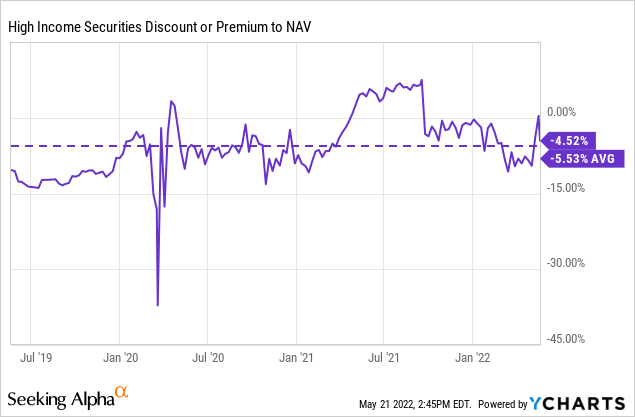

When we last touched on this fund, it was trading at a premium. That takes some of the appeal away from this fund as discounts on discounts also translates into fees on fees. So getting a discount on this fund takes some of that sting away.

Besides the general CEF widening we’ve been experiencing in this 2022 down market, they had quickly lost their premium due to a rights offering. Stanford Chemist went more in-depth on that topic. It ultimately led to the dilution of the NAV, and it made the fund significantly larger. They raised over $67.2 million by issuing an additional 8,042,590 shares. That might not seem like so much, but the fund had only around $88 million in total managed assets the last time we covered it.

The Basics

- 1-Year Z-score: -0.69

- Discount: 4.52%

- Distribution Yield: 11.51%

- Expense Ratio: 0.84%

- Leverage: N/A

- Managed Assets: $144.8 million

- Structure: Perpetual

PCF’s investment objective is to “provide high current income as a primary objective and capital appreciation as a secondary objective.” The fund intends to achieve this by investing “under normal circumstances, at least 80% of its net assets in discounted securities of income-oriented closed-end investment companies, business development companies, fixed income securities, including debt instruments, convertible securities, preferred stocks, and special purpose acquisition companies. The fund also invests in high-yielding non-convertible securities with the potential for capital appreciation.”

Something about these activist-managed funds is that the managers seem to have a sleeve of SPACs involved. I don’t think it is negative when you have some SPAC exposure. However, they often carry such a significant number that it doesn’t do very much for the NAV even when they might get a breakout SPAC. Instead, the appeal here seems to be a place to essentially park some cash that shouldn’t come with much downside risk.

At this time, the fund doesn’t utilize any borrowings, but the underlying investments do. So there are still some elevated risks via their underlying holdings.

Additionally, the expense ratio here is worth pointing out. With their last Semi-Annual Report, it comes in quite low. This could be due to the fund becoming significantly larger. However, I would caution that we could see this rise as the last three years saw the expense ratio at 1.57%, 1.89% and 1.18%, respectively.

Ideally, we would see this lower expense ratio going forward since it does hold a plethora of other CEFs. Those will have their own expense ratios, too, of course. That can push the expenses on a fund up to 3 or 4% in some cases.

Performance – Discount Presents Itself

Through 2022 so far, most investments have been down. That is no different with PCF. Although, on a NAV basis, the fund has been holding up relatively well. A bright spot that is likely due, in part, to that SPAC exposure.

Even when the fund is battling discount widening in the CEF space overall. Several weeks ago, I touched on how much discounts have widened YTD over the last year. When discounts widen, their sleeve of CEFs will also experience this widening and be reflected in PCF’s NAV.

In general, the widening we have been experiencing in CEFs overall is due to greater volatility. This is an observation we’ve seen in every market sell-off. Additionally, valuations were getting quite tight in 2021; this is a bit of an unraveling of that now too.

PCF’s discount is only trading slightly above its three-year average. I believe that makes it a much more interesting candidate than where it had been through 2021 at a premium.

They report the NAV weekly. Here is the latest daily NAV posted at the time of writing.

PCF NAV (Bulldog Investors)

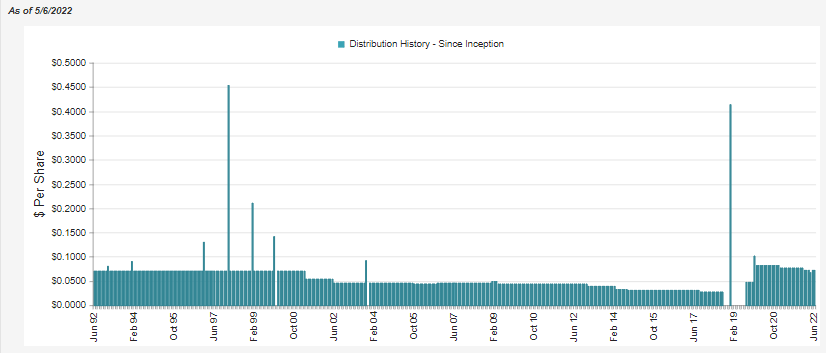

Distribution – 10% Managed Plan

The fund runs with a 10% managed distribution plan that resets annually. That is, if the fund earns the payout or not since it is a target base on the NAV at the end of the year.

Under the Fund’s managed distribution plan, the Fund intends to make monthly distributions to common stockholders at an annual rate of 10% (or 0.8333% per month) for 2022, based on the net asset value of $8.75 of the Fund’s common shares as of December 31, 2021.

Since the fund began this distribution policy, it, unfortunately, has only been cut. Although, it means the fund is always paying a fairly high distribution yield to shareholders. This seems to be a more appropriate holding in the high-income sleeve of one’s portfolio and not the consistent/stable income sleeve.

PCF Distribution History (CEFConnect)

I believe that managed distribution plans are great for the simple fact it makes them predictable. You know exactly what you will get and when it will adjust.

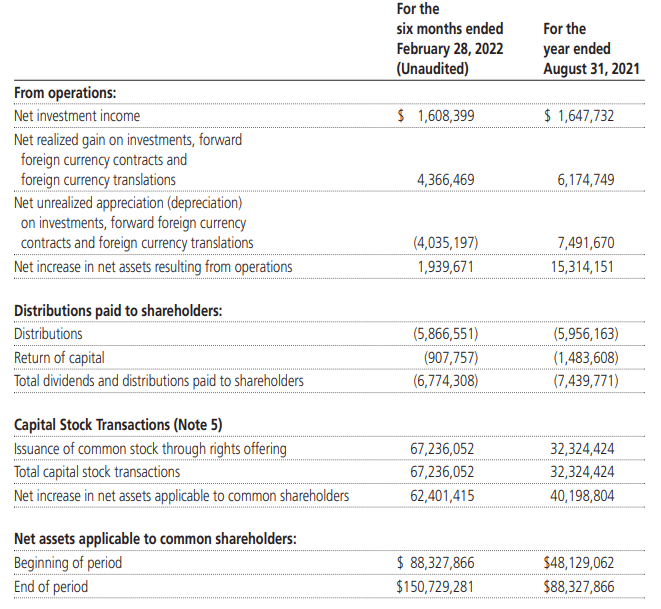

We can take a look at the coverage for the distribution. However, this is one of those cases where it doesn’t really matter. They will be paying that managed plan at 10%, regardless.

PCF Semi-Annual Report (Bulldog Investors)

We can see that they will rely on capital gains to a fairly larger degree to earn the distribution. Net investment income had increased quite dramatically from their prior fiscal year-end. The figure we see above, the $1.6 million, is only for six months. This would seem to be largely driven by the substantial jump in assets due to the rights offering and then that capital subsequently being put to work.

We can also see that in fiscal 2021, they had conducted a rights offering, raising capital at that time too.

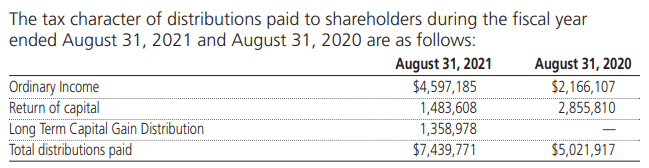

For tax purposes, the last two years show quite a difference.

PCF Semi-Annual Report (Bulldog Investors)

That can make it difficult to estimate what the tax classifications going forward could be. This is true of any fund, but sometimes we get a general sort of consistency from others. This implies that if you are in a situation where you are sensitive to even small tax changes, this fund might just be best held in a tax-sheltered account to reduce any risks.

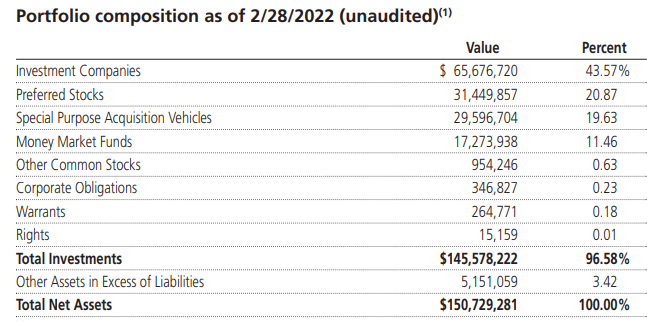

PCF’s Portfolio

CEFConnect lists that PCF carries a total of 170 holdings. One thing I find interesting about this is that the portfolio was most weighted towards investment companies (CEFs/BDCs) and preferred stocks. SPACs were a fairly large weighting too.

PCF Portfolio Composition (Bulldog Investors)

When you look through the entire list of holdings, though, they certainly carry a larger number of SPAC positions relative to the other categories. They are simply in just lower weightings for the most part. That’s why I believe that these SPAC allocations are more a place to park cash rather than actually expect performance.

After the cash position, their largest holding at the time of this report was in FS KKR Capital Corp (FSK). It came to a nearly 5.4% weighting. This is a business development company that had made quite the transformation last year. They had merged with their other BDC that they had managed.

FSK itself is one of those investments that are discounted from its own NAV. They reported a $27.17 NAV at the end of 2021. Based on the current market price, that would give us a 22.56% discount. That seems quite substantial, but we will have to look to the new quarterly NAV update to better look at where it might be now. They are supposed to be reporting on May 9th, so we only have to wait a couple of days in this case.

The second-largest position was in Steel Partners Holding LP (SPLP). This is the preferred holding from that name that came with a dividend rate of 6% (SPLP.PA). It is currently trading below par, increasing the yield to 6.32%.

From there, we have Highland Income Fund (HFRO). This is certainly an interesting fund that seems to get a lot of discussions. One of the reasons is that it is one of the deepest discounted CEFs there is. However, this is generally for a good reason, as the fund’s management has a questionable history. The latest was an attempt to convert to a diversified holding company from a CEF. They eventually withdrew the proposal.

Conclusion

PCF is an interesting fund now that it’s in discount territory. Many of its underlying holdings are also trading at discounts on top of this, which adds to the appeal. 2022 has widened out a lot of discounts in the CEF space due to the volatility. The fund holds FSK and HFRO in its top holdings, which I wouldn’t necessarily put in my portfolio after looking at them previously. However, the fund is much more than just these two names. PCF could be a great fund to provide plenty of diversification through one purchase. At the same time, the managed 10% distribution plan should mean it remains a higher-paying fund.