LightCounting releases its State of the Optical Communications Industry Report

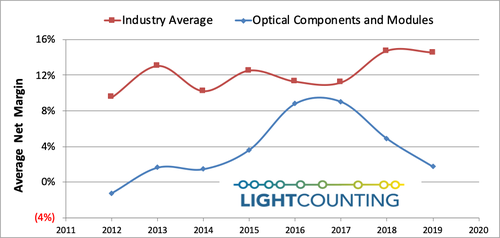

While the profitability of optical component and module vendors was the lowest across the communications industry supply chain for the last 15 years, it improved in 2016-2017, as shown below. The average profit margin of OC suppliers reached 9% in 2016-2017, but fell to 4% in 2018 and 1% in 2019, even though demand for optical transceivers and modules was very strong in those years. Profits of all other types of companies in the industry improved in the last two years, so what is the problem with optics? This is the main question addressed by our State of the Optical Communications Industry report.

In the report we suggest that the main problem with the optical components and modules business is that it is a tiny part of a very large industry. Size matters when it comes to negotiating pricing. Sharp price declines for many optical products and especially for 100GbE transceivers erased profits in 2018-2019. In contrast supply shortages of some 100GbE products helped to sustain prices in 2016-2017 and resulted in improved supplier profitability. This is not the first time that profits of the suppliers picked up when their products were in short supply. Shortages started again in the end of 2019, as demand for optics picked up sharply. The shortages were intensified by COVID-19 disruptions in the first half of 2020, triggering a new spike in orders.

Large customers are concerned with the small size of their optics suppliers and they are terrified of shortages. Each time there is a shortage, customers buy more products than needed and then cancel their orders abruptly as they realize that the shortages are gone and their inventories are very high. This leads to sharp fluctuations in demand.

The decline in demand for 100GbE transceivers in the second half of 2018 is the latest illustration of this cycle. The sudden drop in demand accelerated price declines and reduced profitability of suppliers in both 2018 and 2019.

Lack of confidence in optics suppliers is one of the reasons for Cisco’s acquisition of Silicon Photonics (SiP) start-ups Lightwire and Luxtera in the past, and Acacia in 2019. Ciena, FiberHome, Juniper, Huawei and ZTE are investing in internal manufacturing of optical components and modules also. Most recently, Nokia acquired Elenion (a SiP start up) in early 2020.

An even stronger motivation for bringing the optics in-house, is that it is becoming an ever-larger portion of the bill of materials of optical transport equipment, switches and routers. Limitations in the performance of the optics is often a barrier to innovation in networking and switching hardware.

LightCounting’s State of the Industry reportprovides a holistic analysis of the global communications industry, during a period of unprecedented growth in demand for broadband connectivity and the rise of Cloud companies. It examines business strategies of traditional telecom service providers and Cloud companies, as well as their suppliers of networking equipment and optical/ electronic components.

A detailed analysis of revenue growth and profitability across different levels of the industry supply chain in 2010-2019 is used to identify challenges and opportunities for the future. The report also includes a review of the latest mergers and acquisitions and their impact on the market landscape, the rise of Chinese suppliers of optical and networking hardware over the last decade, and the most recent developments in the China-U.S. trade war.

More information on the report is available at: http://lightcounting.com/products/sotir/