Belgium listed Ontex (OTC:ONXYY) has a history of successfully growing the private label diaper market in Europe. Since 2017 it’s share price has, however, halved from highs and is now below the initial IPO price. The main drivers of this troublesome period are, in my view, a troublesome acquisition in Brazil in 2017 and raw material price increases, especially in fluff, that accounts for half of raw materials. I believe that the headwinds from both effects are over with stabilization being reached in Brazil and with raw materials turning into a margin improving tailwind. My adjusted EBITDA estimates for 4Q19F and 2020F indicate that consensus is 5% and 10% too low, respectively. Shares currently trades on a 12x NTM consensus P/E while less indebted and troubled peers are at 18x. With some positive signals from peers and a management outlook for 2020 imminent, there is a turnaround opportunity in Ontex.

Ontex – A Maker of Diaper Products

Diaper maker Ontex (RIC: Ontex.BR, Bloomberg: ONTEX BB, ADR: ONXYY) is a Belgian personal products company with €1.3bn (US$1.4bn) market capitalization and over 10,000 employees. They focus on disposable personal hygiene products in baby care, feminine care and adult care as well as the healthcare segment. Products include baby diapers, tampons, wet wipes and incontinence products. The company has focused on international expansion in growth countries like Russia, Mexico, Ethiopia and Brazil with a strategy on own and private label brands. Europe is still the most important region for the company.

Source: Company

Source: Company

The European diaper market has not been an easy one in the past. In 2012, Kimberly-Clark Corp. (NYSE:KMB) took the decision to stop selling its Huggies diapers in much of Western and Central Europe. The rationale then given was to leave low-profit businesses in that region.

One reason why Ontex has been able to do well in the past and why Kimberly-Clark has struggled has been the strong growth of the private label market in Europe. Ontex sells its own brands, especially in the emerging markets, but is the largest maker in Europe of private label products for large retailers like Tesco, Carrefour, Metro or Lidl.

Ontex’s strategy after its IPO was based on a three-pronged approach moving it into areas beyond private label:

- Grow outside of Western Europe.

- Increase branded business.

- Expand presence in Adult Incontinence.

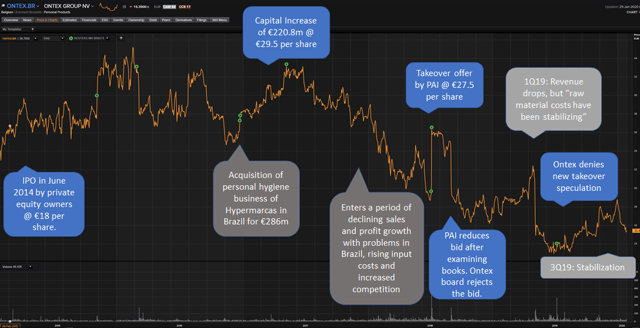

Current Share Price is Below The IPO Price

Ontex’s share price history is less than stellar. The company was listed in June 2014 at €18 per share with generally good like-for-like growth and rising margins propelling shares to over €30 before a problematic period set in.

Source: Reuters, author comments

Source: Reuters, author comments

The troubles for Ontex started with the acquisition of the personal hygiene business of Hypermarcas in Brazil. In addition to some external headwinds, the integration revealed a ‘push’ sale culture and unrecorded trade spending. Manufacturing lines were dated and safety and IT efforts lacking. A lot of effort was spent to remedy these issues over 2017-2018.

From 2018 onwards, Ontex experienced a troublesome period where it was impacted by three issues:

- Declining like-for-like sales due and increased competition.

- Decreasing margins due to rising input costs and trouble integrating the Brazilian acquisition.

- A rejection of a takeover by PAI as the board viewed a decreased bid after examination of the company books as undervaluing the company.

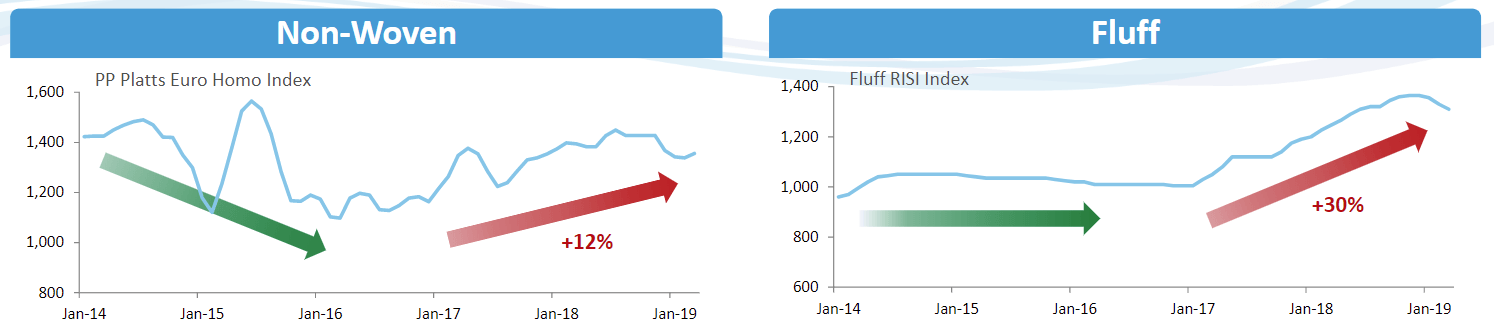

Raw Materials Turning from a Headwind to a Tailwind

Ontex mainly uses fluff, super-absorbers and non-woven fabrics as raw materials. Raw materials and packaging costs account for up to 80% of Ontex cost of sales or conversely 57% of sales. Fluff/pulp makes up 49% of their raw materials and has been a source of major headache for the company. I assume that the peaks in raw materials have been seen in December 2018 and that declines are starting to benefit Ontex from 2Q19 onwards.

Source: Company

Source: Company

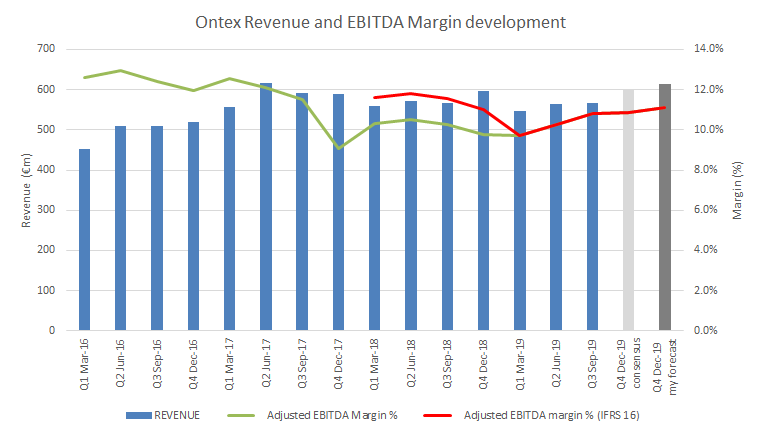

Consensus seems too low for 4Q19F and 2020F

My revenue estimate for Ontex 4Q19 is 3% higher than Reuters’ consensus and implies 3.2% yoy growth, and my adjusted EBITDA estimate implying a 11.1% margin vs 9.8% a year-ago is 5% higher than consensus.

Source: Reuters, author assumptions

Source: Reuters, author assumptions

Beyond positive tailwinds from raw material prices and a weakening euro, there is anecdotal evidence by peers supportive to Ontex.

Swedish peer Essity (OTCPK:ESSYY) is a spin-off from Swedish forestry company SCA which is active in personal care (i.e., diapers and similar business to Ontex) and tissues. Essity reported quite positive for personal care in 4Q19 vs. 4Q18. They saw positive organic net sales growth of 2.5%, coming both from volume and mix with contribution from higher volumes, higher prices, better mix, cost savings and also from lower raw material costs.

Kimberly-Clark commented in their 4Q19 conference call that “organic sales increased 20% in Eastern Europe and high single digits in Brazil”. The company did not specify if the growth in Brazil was underlying market growth or, what is more likely, price increases. Growth in Brazil would, however, be supportive for Ontex.

During its 3Q19 release, management guidance for FY19 was for “Broadly stable sales at constant currencies, with top-line growth in developing markets and lower revenue in developed markets” and “Stable Adjusted EBITDA at constant currencies”. I do not forecast any sales growth in 2019F and my adjusted EBITDA estimate for 2019F is slightly higher than 10.2% realized in 2018.

Source: Reuters, author assumptions

Source: Reuters, author assumptions

The main driver of my positive view on 2020F is an assumption that raw material costs, particularly for fluff, will significantly decline.

My assumption for what could be attained in 2020 is 2% revenue growth (in line with the consensus growth forecast) and a 12.5% adjusted EBITDA margin. This would mean an adjusted EBITDA estimate of €292.4m that would be 10% higher than current Reuters consensus.

The margin improvement assumption is also supported by the company’s own initiatives. As part of Ontex’s T2G program launched in May 2019, more than 1,900 value creation initiatives are to be implemented by end of 2021 and start to deliver results as of 1H20. Ontex also aims to improve efficiency and shift to high-growth products as part of the transformation plan aiming ultimately to lift margins by 125-175 bps vs. 2018.

Other assumptions for 2020F:

- Stabilization and modest improvement in Brazil.

- Declining raw material prices affect to a greater degree than in 2019.

- Margins are likely to improve, but price decreases need to be passed on to clients due to decreasing raw materials costs.

Source: Company, Reuters, author assumptions

Source: Company, Reuters, author assumptions

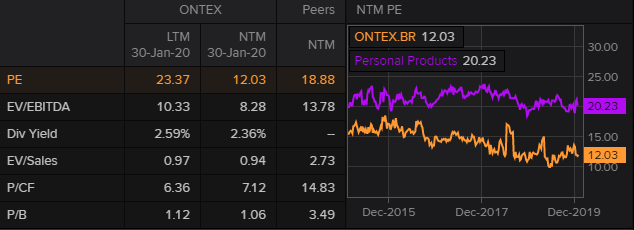

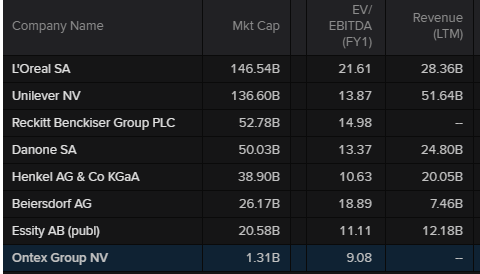

Supportive Peer Valuation

Source: Reuters, Note: LTM (Last Twelve Months), NTM (Next Twelve Months)

Source: Reuters, Note: LTM (Last Twelve Months), NTM (Next Twelve Months)

Source: Reuters, Note: Current market cap and financials in euros

Company Specific Risks

- Net debt stood at €875.7m at September 30, 2019. Net debt/last twelve months Adjusted EBITDA was a high of 3.7x.

- Raw material and Foreign Exchange could impact adversely as the company lacks pricing power.

- Competitive pressures from larger or more aggressive peers and large retail clients.

- Further surprises, as happened in Brazil, from integrating acquisitions. Ontex has been acquisitive in the past acquiring incontinence companies Lille Healthcare in France (2011) and Serentity in Italy (2013), as well as expanded internationally with Mabe in Mexico (2016) and Hypermarcas diaper business in Brazil (2017). 41% of its total assets are goodwill and impairments could affect results and equity.

- Management credibility is low after years of poor performance.

- Possibility of a bid as attempts have been made before.

Disclosure: I am/we are long ONXXF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: My firm is long Ontex on Euronext Belgium.

Disclaimer

Information provided here is not a solicitation to buy or sell any security, or a solicitation of any offer to buy or sell the securities mentioned herein. Data is for illustrative purposes only and even if believed to be factual and up-to-date the accuracy of the data cannot be guaranteed. Narrative and analytics are not tailored to individual portfolio needs nor investment objectives. Readers should always engage in further research and consider as appropriate consulting professional advice before making any investment decisions. Information provided here should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change.