Market forces rained on the parade of Rush Factory Oyj (HEL:RUSH) shareholders today, when the covering analyst downgraded their forecasts for this year. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business. The stock price has risen 5.0% to €0.83 over the past week. It will be interesting to see if this downgrade motivates investors to start selling their holdings.

Following the downgrade, the consensus from lone analyst covering Rush Factory Oyj is for revenues of €2.8m in 2020, implying a substantial 31% decline in sales compared to the last 12 months. Statutory earnings per share are supposed to plummet 83% to €0.02 in the same period. Previously, the analyst had been modelling revenues of €3.9m and earnings per share (EPS) of €0.11 in 2020. Indeed, we can see that the analyst is a lot more bearish about Rush Factory Oyj’s prospects, administering a sizeable cut to revenue estimates and slashing their EPS estimates to boot.

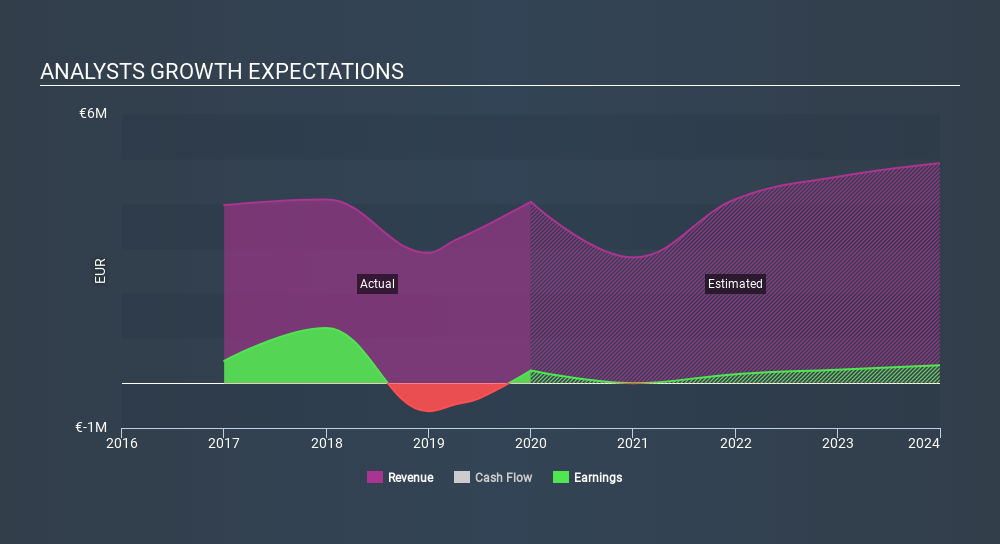

View our latest analysis for Rush Factory Oyj

It’ll come as no surprise then, to learn that the analyst has cut their price target 33% to €0.80.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. One more thing stood out to us about these estimates, and it’s the idea that Rush Factory Oyj’sdecline is expected to accelerate, with revenues forecast to fall 31% next year, topping off a historical decline of 4.5% a year over the past three years. Compare this against analyst estimates for companies in the wider industry, which suggest that revenues (in aggregate) are expected to grow 9.0% next year. So while a broad number of companies are forecast to decline, unfortunately Rush Factory Oyj is expected to see its sales affected worse than other companies in the industry.

The Bottom Line

The most important thing to take away is that the analyst cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

There might be good reason for analyst bearishness towards Rush Factory Oyj, like dilutive stock issuance over the past year. Learn more, and discover the 3 other flags we’ve identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you spot an error that warrants correction, please contact the editor at [email protected]. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

The easiest way to discover new investment ideas

Save hours of research when discovering your next investment with Simply Wall St. Looking for companies potentially undervalued based on their future cash flows? Or maybe you’re looking for sustainable dividend payers or high growth potential stocks. Customise your search to easily find new investment opportunities that match your investment goals. And the best thing about it? It’s FREE. Click here to learn more.