Nucor (NUE) is a must-watch stock. Even if you don’t own any shares, I still recommend you follow the stock as America’s largest steel producer is a valuable source of information. The company just reported its fourth quarter results. The good news is that sales and earnings came in higher than expected. The bad news is that the company continues to be in a steep economic decline. The stock price is currently selling off after starting to price in higher economic growth in 2019. I’m not turning bearish, but a lot needs to happen to prevent this stock from breaking down. I expect this to succeed but risks remain elevated until the economy starts to gain upside momentum.

Source: Nucor

Q4 Was An Ugly End Of An Ugly Year

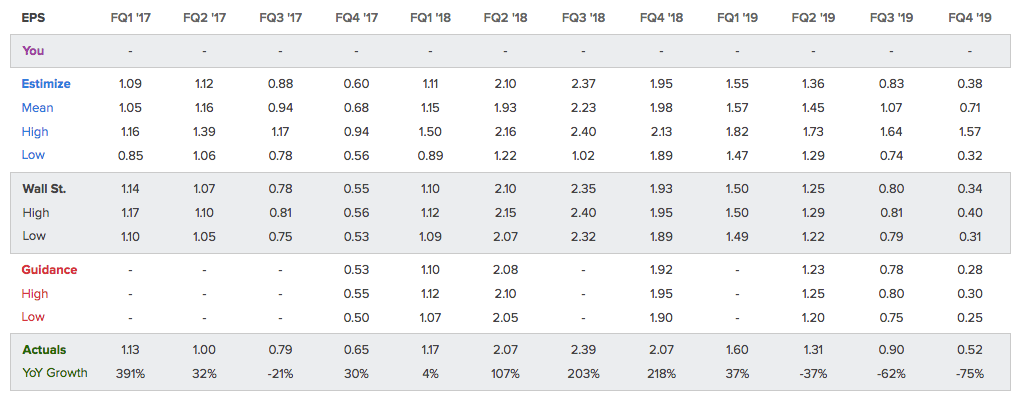

Below is the perfect example of what happens to a cyclical steel company when economic growth is down. In the fourth quarter of 2018, economic growth in the US peaked after a very strong run since the start of 2016. This was a few months after the global economy peaked at the start of 2018. Trade uncertainties and deleveraging in China were major drivers behind this slowing cycle. As you can see, higher economic growth resulted in triple-digit adjusted EPS growth in 2017 and 2018. The slowing trend has accelerated in the fourth quarter, pushing adjusted EPS growth down to $0.52. This is well-above expectations of $0.34 but 75% lower compared to the prior-year quarter when EPS was up 218% to $2.07.

Source: Estimize

Source: Estimize

In this case, weakness started at the very top. Total sales reached $5.1 billion. That’s a decline of 18.5% compared to the prior-year quarter. It also marks the third consecutive quarterly sales decline. Gross profit declined by 60.9%. That’s the worst number since the fourth quarter of 2015 when gross profit fell by 116.2%. Gross margin also hit a new low of 8.5%.

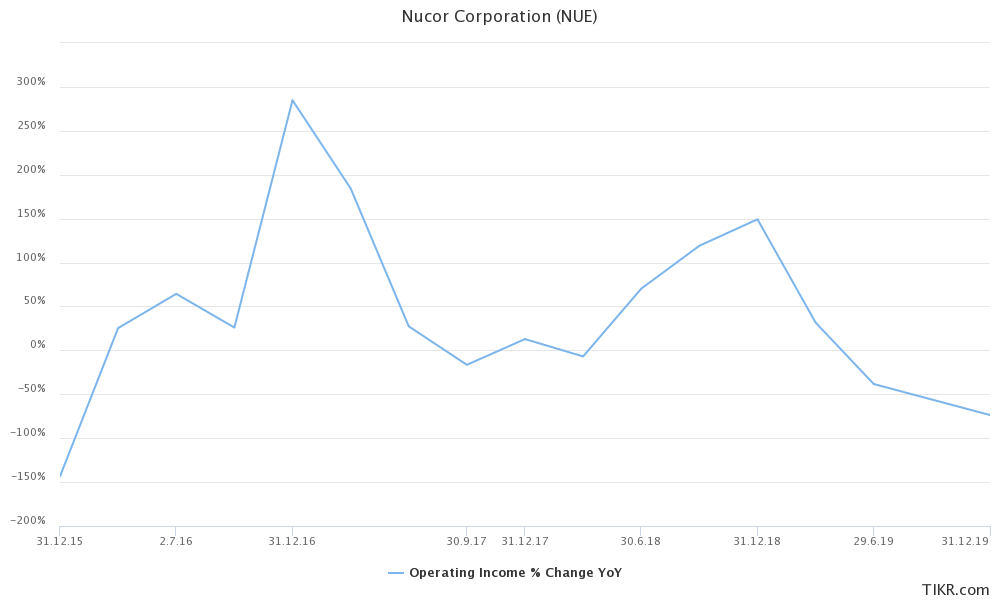

Operating income fell by 73.6%. Almost needless to say, this too is the third consecutive decline and a multi-year low as the graph below shows quite well. The business cycle that started to accelerate at the start of 2016 has officially resulted in contraction after a number of strong years.

Source: TIKR.com

Source: TIKR.com

The fourth quarter weakness was mainly a result of lower steel prices. Domestic scrap metal prices rose markedly and sheet, plate, structural and bar mills all implemented price increases. Moreover, losses in the company’s raw materials segment significantly increased in the fourth quarter as a result of planned outages at the Louisiana DRI plant. Note that these outages were planned as I discussed in my previous article.

Results from Nucor’s raw material segment declined due to a further margin decline at the company’s DRI (direct reduced iron) operations. Adding to that, the Louisiana DRI facility had a planned outage in early September, which is expected to continue until mid-November.

Overall, a lot was already expected. At the start of this article, I showed you a massive earnings decline. This decline was ugly but still way above expectations. That’s a benefit a company like Nucor had. Sales are somewhat predictable as the company has a very cyclical pattern and is on the mid term more dependent on the business environment instead of company growth measures.

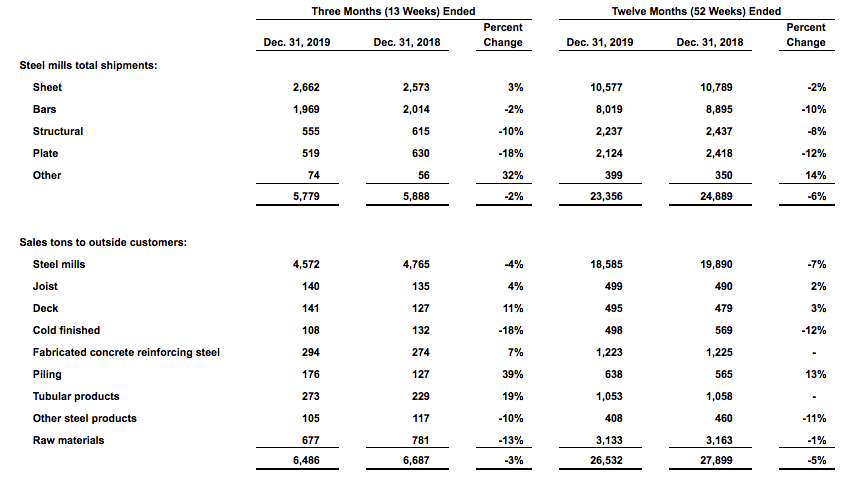

That said, total shipments from steel mills were down 2% in the fourth quarter. On a full-year basis, shipments were down 6%. Shipments to customers were down 3% with pretty much contraction in all major segments.

Source: Nucor Q4/2019 Earnings Release

Source: Nucor Q4/2019 Earnings Release

With all of this in mind, I have to give Nucor credit. Yes, the company suffers when the economy is down. Nonetheless, the company continues to find ways to improve its business in the long term. For example, we are not dealing with an overleveraged steel producer here that desperately needs higher prices in order to survive.

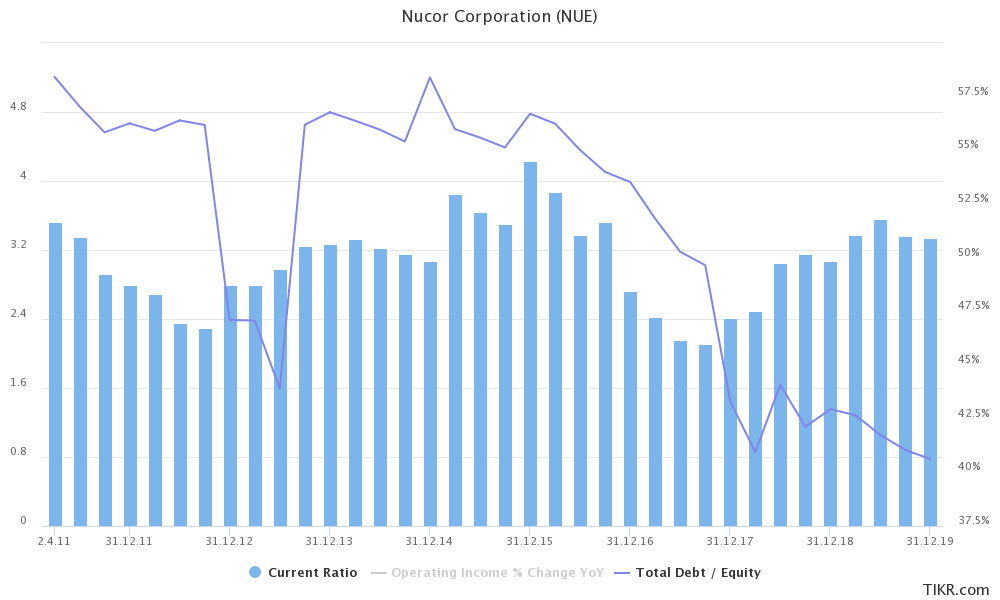

Total assets continued to improve to $18.3 billion from $17.9 billion in the prior year. Meanwhile, total liabilities further fell to $7.6 billion. While liquidity (as displayed by the current ratio) always has been high, we are witnessing that total debt as a percentage of total equity and liabilities has declined to 40%. The company is doing an outstanding job reducing debt after investors were hit by both elevated debt levels and rapidly declining commodity prices in 2015.

Source: TIKR.com

Source: TIKR.com

2020 Is Expected To Be Stronger

Nucor expects first quarter earnings to be higher than fourth quarter earnings of 2019. Earnings in the steel mills segment are expected to increase due to higher expected volumes. Nucor also expects a more stable pricing environment in 2020 after a severe inventory destocking that took place in 2019. On top of that, management expects an improvement in pricing for raw materials.

My point of view is that Nucor’s expectations are realistic. Future regional business expectations have been improving for three straight months and should go positive rather sooner than later. I expect this to turn into growth acceleration in the first half of this year. Historically speaking, this should lead to higher commodity prices and a return of traders who are willing to buy cyclical stocks like Nucor.

Source: Author’s Spreadsheets (Raw Data: Regional Fed Manufacturing Surveys)

Takeaway

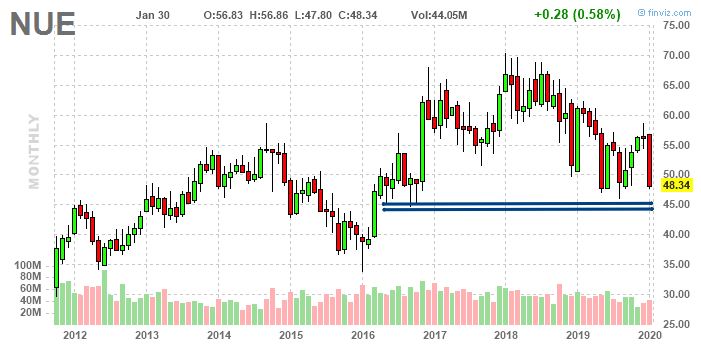

Currently, Nucor is trading at 12.4x next year’s earnings and a dividend yield of 3.4%. The valuation is attractive and the dividend yield is interesting. Nonetheless, both are meaningless in case the economy does not improve. In that case, I expect the stock to break down lower to $30 per share in 2020. However, as I’m bullish on the economy, I expect support at $45 to hold for now. Unfortunately, there’s another factor at play right now. The ongoing worries regarding the coronavirus are very unpredictable and could cause additional short-term volatility. I’m therefore not too focused on technical buying points. I consider Nucor to be a good buy if the economy is indeed able to bottom. Yes, Q4 was bad. But that was expected. What matters now is that the company is getting some fundamental support to back its 2020 outlook.

Source: FINVIZ

Source: FINVIZ

Stay tuned!

Thank you very much for reading my article. Feel free to click on the “Like” button and don’t forget to share your opinion in the comment section down below! My long-term investments are stated in my Seeking Alpha biography.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This article serves the sole purpose of adding value to the research process. Always take care of your own risk management and asset allocation.