sarkophoto/iStock via Getty Images

I recently wrote articles on two of my largest positions, Enterprise Products Partners (EPD) and Magellan Midstream Partners (MMP). They are also MLPs providing transportation and storage services for natural resources. If you are curious about the big picture for pipelines and some of the K-1 form nuances, those would be good articles to read. I am bullish on MPLX (MPLX), but I decided that those two MLPs were a better fit for me, and the K-1 forms required for MLP investors means that owning more than a couple can be a real pain when tax season rolls around.

Investment Thesis

MPLX is one of the energy stocks that has been out of favor for years. It is one of the lesser known publicly traded MLPs. Trading under 7x cash flows and a 9% yield means investors only need a little price appreciation to see double digit returns. In my opinion, it will only take a couple years for MPLX to head towards $40 a share. Investors can expect continued distribution increases, buybacks, and potentially special distributions moving forward.

The Business

MPLX is a master limited partnership (MLP) that earns its revenues transporting and storing crude oil, natural gas, and other refined petroleum products. Investors can expect relatively stable revenues that are not exposed to price fluctuations of the underlying natural resources.

Investors should be aware that MPLX’s parent company, Marathon Petroleum (MPC), is a large unitholder in MPLX. In my opinion, I find a distribution cut highly unlikely despite the high current yield. Management has been focused on unitholder returns, which was proven by the recent special distribution and significant ongoing buyback program.

Investor Presentation

MPLX isn’t going to act like some volatile tech stock that has the potential to 10x, but that might be exactly what investors are looking for right now. Investors that like buying for fair value or less and receiving company profits in the form of dividends or distributions might find MPLX to be a good addition to a portfolio.

Valuation

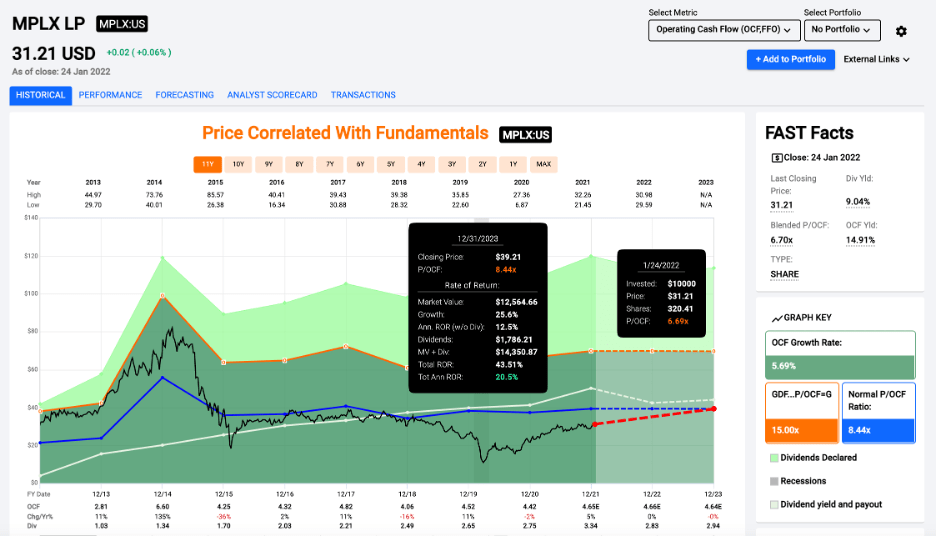

MPLX certainly qualifies as cheap, with a price to cash flow multiple of 6.7x. This is lower than average for the industry, and I wouldn’t be surprised to see the multiple return to 8x or 9x in the next couple years. Investors buying at current prices would easily see double digit returns when you factor in the 9% yield.

Price to Cash Flows fastgraphs.com

I owned MPLX starting in early 2021 and sold after the recent special distribution. You might be asking why I would sell if I’m bullish on MPLX. The first reason was to reduce the number of K-1 forms I would have to file for 2022. The second was the ability to take gains and reinvest the proceeds in EPD around $22, which is currently my largest holding. My MPLX position wasn’t large enough to justify holding, and I was able to add to one of my highest conviction positions.

Just because I prefer EPD and MMP doesn’t mean investors should write off MPLX. There might be reasons that investors prefer MPLX, but I decided I could add to EPD and eliminate a K-1 form for next year’s taxes. Investors looking for more yield at an attractive valuation are likely to find that MPLX will provide double digit returns for at least a couple years.

The Distribution & Buybacks

MPLX has a reasonable current valuation, and they have been focused on stepping up the unitholder return program. Late in 2020, MPLX announced a $1B buyback program. By the end of Q3 2021, there was $497M remaining on the buyback authorization, and 17.6M units were repurchased in the first nine months of 2021 at an average cost of $26.79.

Buybacks are great, but investors in MLPs are typically attracted by one thing: large tax advantaged distributions. MPLX’s current yield is just over 9%, and it has been increased for 8 years straight. For income investors, this is enough to make the clouds part and the angels sing. We are currently stuck in the yield desert as investors, but MPLX is a high yield that has been able to sustain its large payout through different market conditions.

The growth has been slowing down over the last three to four years, with the special distribution of $0.575 being the exception to the rule. Investors should not be expecting rapid distribution growth, but MPLX has been able to maintain the payout with a reasonable payout ratio, so I would be genuinely surprised by a distribution cut. I wouldn’t be surprised to see future special distributions as well.

Conclusion

MPLX is an appealing choice for investors looking for current income with the potential for continued distribution increases and a price appreciation kicker. Like other MLPs, I think MPLX is undervalued and is likely to head for $40 a share in the next couple years. Investors interested in getting paid to wait could see double digit returns from MPLX. As long as you are fine with MPC’s relationship with MPLX as the parent company, MPLX could be a good way to add some midstream exposure to your portfolio.