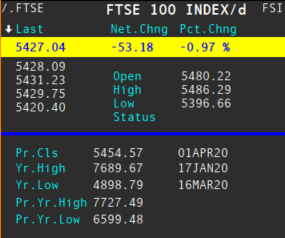

It was Friedrich Nietzsche who wrote, “Well the years start coming and they don’t stop coming”, probably. We’ll check later. In the meantime we can but note that it’s a Friday, apparently, which amid the ceaseless tide of red numbers and constricted circumstances means we can at least look forward to two days of looking at fewer red numbers. Here’s what midsession looks like:

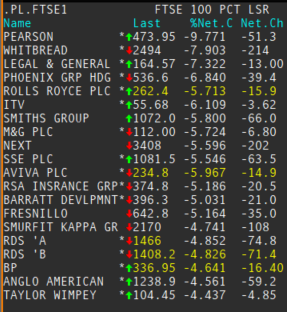

Pearson, then, and Morgan Stanley’s put a pin in all that distance-learning hype that had put a floor under the stock in recent weeks. People still need to go places, MoSt says under the headline, “Financially sound, structurally challenged and valuation not attractive”:

Disruption to Global Assessment: In its new divisional breakdown, Global Assessment is Pearson’s largest 2019 EBITA contributor at 36% of the total. It is also the most affected by Covid 19 disruption as physical test centres close. Pearson anticipates a c£30m per month EBITA impact pre cost saves in Assessment plus a potential c£30m EBITA hit in US Student Assessment. We assume a circa four-month disruption with an unalleviated £150m EBITA impact in 2020, mainly recovered in 2021.

Accelerated US HEC decline? We think the structurally weak US Higher Education Courseware will be impacted by disrupted US college enrolment and financial pressure on personal budgets impacting discretionary purchases of college textbooks. We forecast declines of 25%/15% in 2020/21 US HEC organic revenue. We don’t subscribe to the thesis that higher US unemployment is positive for college enrolment. There may be some modest benefits in Pearson’s virtual schools/college businesses, Connections and OPM from Covid 19 disruption.

EBITA forecasts drop by 38%/16% (£188m/£76m) in 2020/21. With the cancelled share buy back, our EPS forecasts drop 44%/21%. Organic revenue growth is -10 % in 2020 (-4% ex US HEC, impacted by Global Assessment) and +3% in 2021. We have group organic revenue growth at just c1% pa 2022-24 reflecting continued US HEC declines (group organic growth is c3.3% pa 2022-24 ex US HEC). EPS growth is -6% pa 2019-24e. Balance sheet/liquidity well placed: At end-February 2020, Pearson had c£1bn of liquidity, since enhanced by the £530m proceeds of the PRH sale. Its RCF has a <4x ND/E pre IFRS 16 ND/E covenant. We have Pearson ND/E on this basis at 0.1x at end 2020. Pearson has suspended its £350m buy back with £167m spent but is going ahead with the payment of the 2019 final dividend (13.5p, cost c£104m).

EW: PT reduced to 500p: The DCF based target drops 20% to 500p, at which level Pearson trades at c14x 2021 EPS and a FCF yield of 6%. By 2024 these multiples are c12x/8.5%, still not attractive. Pearson has some defensive merits at present, but uncertainty remains with the impending change of CEO and given we think the structural challenges (34% print at least, untested growth models) are substantial. The sound financial position offsets these issues for the moment, but Pearson will likely lag any market recovery, in our view.

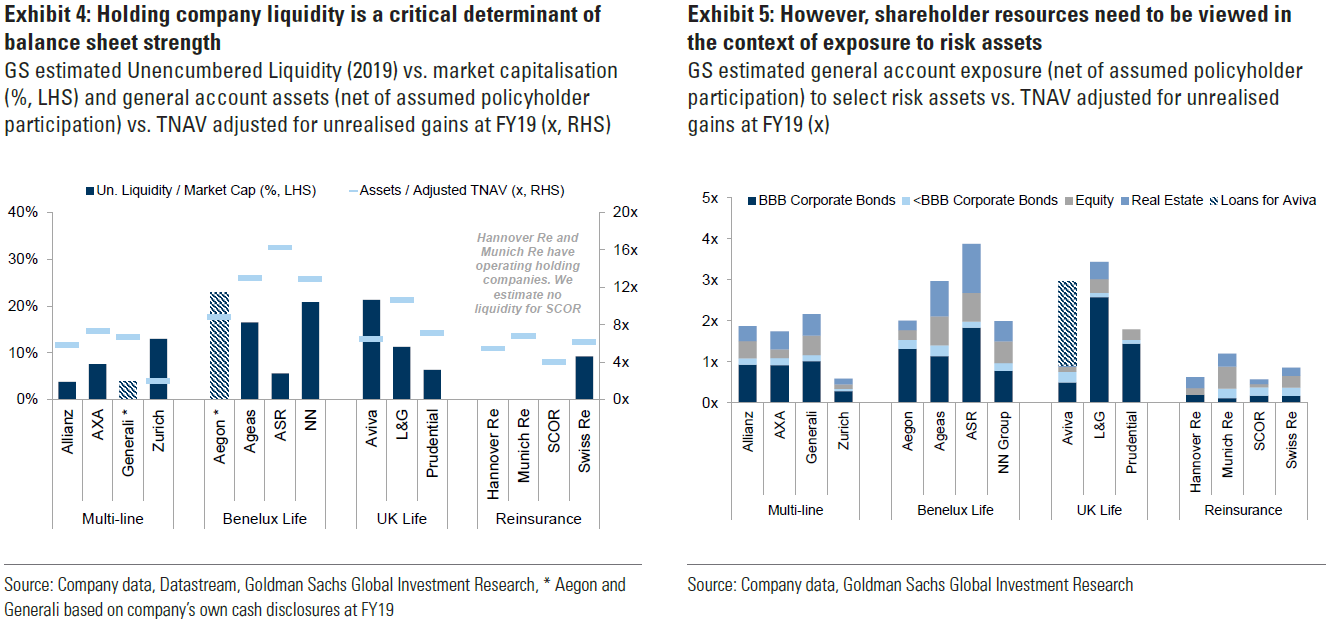

Europe’s insurers are getting hit quite hard on pressure to cut dividends. The European Insurance and Occupational Pensions Authority (EIOPA) said late on Thursday that temporary suspensions were essential to ensure robust capital reserves, which the EU has said looks a good plan. But opinions otherwise are split. BaFin has called for financial institutions to refrain from share buybacks but said dividend policies were up to the insurer. The Dutch regulator said the EIOPA was bang on, while the Norwegian FSA had already called for a ban on dividends/buybacks last month. The BoE’s PRA added this morning that it expects “firms to be prudent in deciding on dividend payments or variable remuneration in view of the elevated levels of uncertainty presented by coronavirus and its impact on the global economy.” The regional stuff is important because, unlike banks, the subsidiaries of insurance companies are supervised by local regulators in each country of operation. Here’s Goldman:

Simplistically consolidated (group) solvency has a more limited meaning in an economic crisis. Each subsidiary of a group needs to be independently capitalized, ultimately summing up to the group solvency ratio (adjusting for debt, intra-group transactions and diversification). Each local regulator will ensure obligations to their local policyholders are met, irrespective of an insurance group’s need. If these conditions are not met (capital, risk etc.) then dividend restrictions or capital injections could occur at a subsidiary-by-subsidiary level.

The ability of individual operating entities to remit capital/dividends will be dependent on local constraints. With capital market conditions becoming increasingly challenging, local regulators may become more prudent, meaning the ability of insurers to sustain remittances could become difficult. As a result, the greater the reliance of an insurance group on any one subsidiary, the more concentrated its exposure to regulatory intervention.

Of the European insurers only Unipol and CNP have voided regular dividends so far. Swiss Re and Munich Re have already suspended buybacks but Allianz is on the wires saying it has no intention to do anything. Here’s Barclays:

[R]esilient solvency ratios and better balance sheet/cash flow management suggest there are no material financial constraints to dividend paying ability of European insurers at this stage, so we’ve anticipated any potential dividend suspensions to be driven by regulatory pressures and/or limited visibility in the post-COVID world. EIOPA’s statement yesterday, following various somewhat mixed positions so far from national regulators, officially opens the ‘negotiation’ table – we expect a few days of intense discussions between European insurers and their respective domestic regulators. We note that for insurers this is really being presented as a “deferral” of dividends; markets need to get much worse for capital to be at risk, but it appears increasingly likely a number of insures may have to postpone 2019 dividend decisions into 2H 2020. Interestingly, BaFin has distanced itself from EIOPA’s statement, commenting it intends to take a more case-by-case approach as it doesn’t see the need for a blanket ban on dividends at this stage. Munich Re (OW) and Allianz (EW) have both already commented in the past few weeks they intend to stick to their ordinary dividends. Core defensive insurance OW include Zurich and Tryg that have already paid dividends and Munich Re that intends to stick to its ordinary dividend, underpinned by one of the strongest balance sheets in the industry and, we would expect, supported by its home regulator.

And some charts on the piecemeal thing from Goldman:

Ok, so what else? Stifel upgrades travel cafe operator SSP post last week’s cash box fundraising:

‘When will travel restrictions be lifted?, and what sort of recovery should be expected once they are?’, remain the million dollar questions. Sadly, we don’t have the million dollar answers. Airline industry body IATA forecasts a gradual capacity recovery in Q3, down 33% globally compared to down 65% for Q2. In Europe, which accounts for two-thirds of SSP’s revenue (inc. UK), IATA forecasts Q3 capacity down 45% vs. down 90% in Q2. We expect passenger demand to lag capacity as business and consumer confidence is bruised this summer, whilst the perceived risk of getting ill or disrupted lingers. For SSP we assume revenue for the June quarter is down 90% and down 70% in the September quarter, which compares to -80% in SSP’s own ‘very pessimistic scenario’. We cut FY20 revenue by 44%, arriving at an EBIT loss of £152m based on 30% profit drop through in H2. Our FY21 estimates reflects a partial recovery, with revenue and EBIT down 16% and 26%, respectively.

SSP has moved quickly to conserve cash, reigning in costs, capex and suspending dividends. In particular, minimum rent guarantees have largely been overridden so that concession fees (20% of sales) become a variable cost; whilst labour costs (29% of sales) will benefit from job protection schemes in some of SSP’s major markets. On that basis our cash burn analysis is consistent with the £15m-£20m per month cited by management. SSP has also acted quickly to tap equity and debt markets to protect liquidity in a worst case scenario, raising gross proceeds of £216m from an equity placing (19.3% of shares in issue), agreeing a new committed bank facility of £112.5m and successfully accessing the UK government’s Covid Corporate Financing Facility (CCFF). We expect net debt to increase from £483m at September 2019 to £767m in September 2020, driven by a material working capital outflow (next to no sales but still paying suppliers). This suggests liquidity headroom of £125m against committed facilities, i.e. another seven months cash burn to April 2021 and considerably longer when the CCFF is included. By September 2021 we forecast ND/EBITDA of 1.9x, within SSP’s medium-term parameters of 1.5x-2x.

Since the IPO in 2014, SSP has delivered strong total shareholder returns (TSR) based on structural market growth, strong execution (sales growth + margin expansion) and ad hoc shareholder returns on top of the ordinary dividend. The disruption facing airlines and airports at the moment has become so severe that a quick recovery to a pre-COVID-19 world is unrealistic. The debate has moved to what shape of global recession and recovery might be expected, with critical implications for the aviation and airports industries. The ‘structural market growth’ aspect of the investment case is therefore on hold, as is the potential for ad hoc shareholder returns as SSP looks to rebuild its financial strength and credit metrics. We assume the dividend is passed this year but is reinstated in FY21 based on a 40% payout. Historically, the EV/EBITDA multiple has averaged 10x (12M forward), for the most part in a 9-12x range. We reset our TP to 400p (from 550p), applying a 9x multiple to FY21 EBITDA. With 48% upside potential, we move to Buy from Hold.

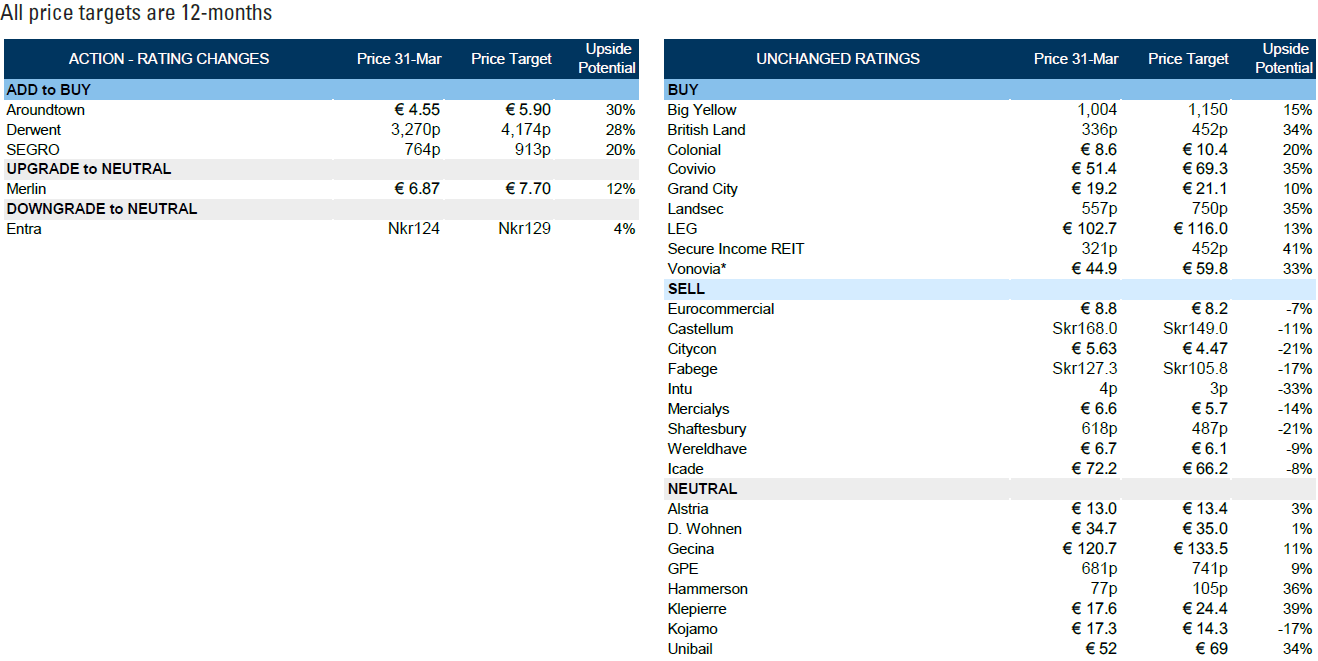

And Goldman Sachs has a big Reit note out upgrading various things:

The gist of which is:

Following the significant de-rating and some names underperforming the sector vs. the broader European market, we believe German residential, select UK alternative and select office landlords are best positioned to be resilient in the current environment, and also offer attractive valuations. We see headwinds for retail landlords, both in terms of underlying trading and balance sheet resilience. … We believe the underperformance has been led by parts of the sector, mostly retail and hotel-exposed stocks, which are substantially negatively impacted by lockdowns and store closures in relation to COVID-19, and are down as much as 50-60%. On the other hand, residential and alternative landlords under our coverage have been most resilient, reflecting the very specific nature of this correction.

Given the 35% correction of our coverage since the YTD peak mid February, we see opportunities as we consider (all Buy-rated):

(a) Structural winners which should outperform even in an extended shutdown: Vonovia, LEG; Grand City (all in the residential space).

(b) High quality names which may see some limited negative impact, but we expect will recover quickly post stabilsation: Colonial, Derwent (up to Buy from Neutral), SEGRO (up to Buy from Neutral), Big Yellow (Office, UK ‘Alts’).

(c) Oversold names with good quality businesses, which we think will recover in the short-to-medium term once the environment stabilises: Aroundtown (reinstate at Buy), Covivio, Secure Income (remove from CL) (Hotels).

(d) Stocks with some retail exposure, but also with large office businesses and depressed valuations: British Land, Landsec (UK ‘diversified’).

• Updates to follow. Requests, complaints and so on can go in the comment box. For FTAV unfiltered, the Telegram Markets Live chat group offers crowdsourced moment-by-moment commentary.