The recent Iran conflict reminds us of the importance of having top notch intelligent defense systems in place. Of course, there are many other potential threats in the world that create this need. The United States and our allies need to remain a step ahead of potential threats. Leidos (LDOS) plays a key role in providing the smart defense systems that we need to combat potential threats.

Leidos has plenty of growth ahead as the need for ongoing defense upgrades are likely to be needed for the foreseeable future.

Leidos is a smaller, lesser known defense company. However, the company is an important part of the United States’ overall defense strategy. Leidos has defense solutions that cover land, sea, air, space, and cyberspace. The company offers intelligence systems, command & control, and logistics solutions. The need for ongoing updates to our defense systems increases the likelihood for Leidos to experience continued backlog and revenue growth.

Leidos’ Recent Acquisition of Dynetics

Leidos announced in December 2019 that they intend to acquire Dynetics for $1.65 billion in cash. Dynetics is a privately owned industry-leading applied research and national security solutions company. Dynetics produces about $450 million of revenue annually, which Leidos’ will being earning upon the completion of the acquisition.

The addition of Dynetics is expected to increase Leidos’ capabilities for rapid prototyping and agile system integration/production. Dynetics will help in the following areas: advanced sensors, autonomy, hypersonics, and space solutions. This provides a complimentary fit to Leidos’ defense and civil businesses.

The acquisition is expected to close in Q1 2020. Therefore, Leidos can benefit from at least three quarters of revenue and EBITDA generated from Dynetics this year.

Leidos’ Growing Backlog to Drive Future Growth

Leidos’ total backlog increased 17.7% to $23.9 billion in the first 9 months of 2019. This will help drive future revenue growth as the orders are produced and delivered to customers.

Leidos most recently received a new contract worth $6.5 billion for a 5-year base period with the potential for a longer time period. This contract is to help the Defense Information Systems Agency with operating, maintaining, and securing military telecommunications infrastructure. This is a modernization of the network that connects government leaders to military personnel.

It is important for this system to be highly secure, reliable, and efficient. That is where Leidos’ engineering expertise comes into play to make this possible.

Leidos also secured a $4 billion contract earlier in December 2019 along with Parson Government Services & Centerra Group to provide the U.S. Department of Energy a variety of services at the Hanford Site. The contract has a base period of 5 years with a potential option period of 3 years and another option period of 2 years. The following services will be rendered under the contract: land management, security and emergency services, IT, hazardous material management, infrastructure upgrades/maintenance, and new infrastructure.

In September, the company was awarded a $445 million contract for IT support, cybersecurity, engineering, and telecommunication services for the Air Force’s headquarters. This contract runs through September 2024. Leidos beat out two other competitors to remain the incumbent provider for these services.

Those are just some examples of recent contract wins which Leidos is awarded on a regular basis. Some contracts are smaller, but the important thing is that Leidos gets a steady amount on a regular basis. This led to the company’s growing backlog, which has a good chance of turning into revenue growth.

Leidos’ Competitive Advantages

Leidos’ continued success is driven by the following four factors: customer relationships, technical differentiation, key personnel, and past performance. These are the keys that Leidos believes will scale their business for future growth.

Understanding customer needs and solving them is the key to customer relationships. Leidos employs a lot of knowledgeable engineers and experts to deliver on what customers are demanding. Maintaining long-term commitments to customers’ missions helps strengthen those relationships which builds trust – increasing the chance for Leidos to get repeat business.

On technical differentiation, Leidos has the Leidos Innovations Center. This is the company’s R&D efforts for innovative technology and solutions. The technologies involved with this include: advanced computing, artificial intelligence [AI], machine learning [ML], sensing, processing, and getting solutions from the laboratory into actual operations for customers.

Leidos is using AI/ML to help customers effectively use their increased amount of data for new opportunities, efficiencies, and insights. This means protecting cyber data from attacks, finding new ways to fight cancer, and improving the safety and efficiency of airspace.

The company also uses a strategic partnership program which unites Leidos’ key suppliers to leverage their strengths for new technological milestones. This works as a brainstorming of experts, leveraging the supplier base to ensure that customers are getting the best solutions.

The key personnel factor is Leidos’ collection of experts, military veterans, top secret, cleared employees that help develop and deliver effective solutions to customers. The company offers a technical career track for employees, which helps to increase retention and drive Leidos’ growth.

The past performance is a competitive advantage because excellent customer relationships and the delivery of effective solutions gave Leidos a strong positive reputation in the industry. This helps in retaining existing customers and gaining new ones.

Leidos: A Company with Strong Positive Cash Flow

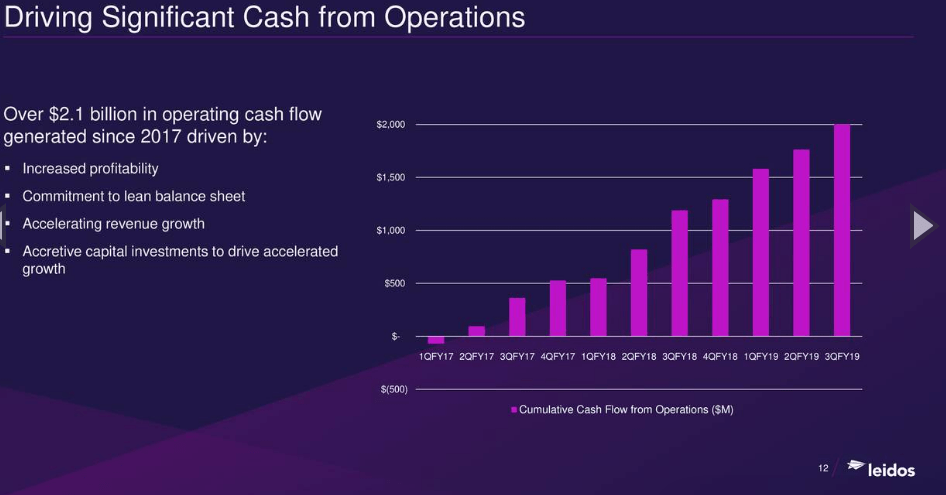

Leidos obtains significant cash from operations. Over the past 12 months, Leidos had $927 million in operating cash flow. This is a 21% increase as compared to the $768 million generated in 2018. Operating cash flow has been increasing at double digit rates over the past few years.

Leidos has been increasing their net income margin by driving down SG&A and operating expenses. The company had a 5-yr. average net income margin of only 2.58%. However, this increased to 6.25% in the past 12 months. That’s a great demonstration of driving down expenses.

Revenue and earnings growth are expected to continue to grow in 2020. Consensus estimates show that revenue is expected to increase by 5.55%, while earnings are expected to increase by about 8% in 2020. These consensus estimates have been increasing over the past three months. So, the actual end results could be higher as the company’s offerings are seeing strong demand.

Leidos’ Valuation: Reasonable

Leidos’ valuation looks reasonable in this stage of the bull market. The broader market as measured by the S&P 500 (SPY) is trading with a forward PE of 20. Leidos is trading below that with a forward PE of 18.6. Here’s how Leidos stacks up with their competitiors:

| Leidos | Booz Allen (BAH) | CACI (CACI) | L3Harris (LHX) | Raytheon (RTN) | ||

| Forward PE | 18.9 | 22 | 19.4 | 19.5 | 17.5 | |

| Price/Sales | 1.34 | 1.56 | 1.3 | 5.09 | 2.21 |

source: Yahoo! Finance

Leidos is trading slightly below the average forward PE of 19.5 for these five companies. They are also trading below the average price/sales ratio of 2.3. This looks like a fair and reasonable valuation level in this stage of the bull market. However, we’ll have to keep an eye on the overall market as a correction can happen at any time on profit taking at the S&P 500’s (SPY) high above average valuation level with a forward PE of 20 (long-term average is 15.78).

Long-Term Investment Outlook for Leidos

The dangers that we face in the world probably aren’t going away anytime soon. There are always likely to be various threats and conflicts in the world. This includes for the IT related solutions that Leidos provides.

Defense systems need to be increasingly intelligent. We have to protect computer systems just as much as we need to protect our military bases, businesses, and homes. Leidos is a key provider of defense solutions to help combat the current and future threats that our nation faces.

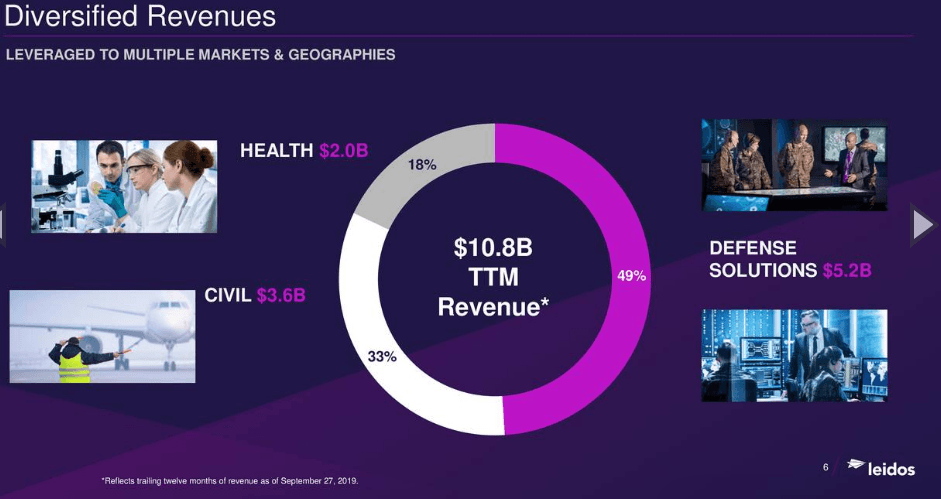

I like that the company is diversified beyond the defense business. Leidos derives the other half of their revenue from their civil and health business segments. We’ll have to keep an eye on growth in those segments. All three segments are growing, but the Health segment posted a large 14.4% gain in revenue for Q3 2019. This was higher than the Defense segment’s gain of 8.3% and the Civil segment’s 10.4% increase.

Keep an eye on how Leidos scales up all three segments. It is possible that the Health segment becomes a larger portion of total revenue over time. Leidos’ solutions for managed health services are likely to see strong demand as healthcare becomes more digitized.

With continued strong earnings growth, Leidos’ stock has a good chance of doubling within approximately 5 years. This can be driven by PE expansion along with earnings growth that is expected to average about 8% to 10% per year (consensus).

The 2020s will see the transformation of the economy during the 4th Industrial Revolution. We are also running head first into a wave of demographic and debt driven problems that will need solving. A cautious, but forward looking approach, will be required to thrive in what could be a lost investing decade for many, much like 2000-2009.

Benefit from the insights of Kirk Spano, Dividend Sleuth and David Zanoni. Get exclusive investment ideas based upon in-depth and up close research that few others do.

Sign-up now for a free trial and 20% first year discount.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. Business relationship disclosure: The article was written by David Zanoni for Kirk Spano’s Margin of Safety Investing service [MoSI].

Additional disclosure: The article is for informational purposes only (not a solicitation to buy or sell stocks). David is not a registered investment adviser. Kirk Spano is an RIA. Investors should do their own research or consult a financial adviser to determine what investments are appropriate for their individual situation. This article expresses my opinions and I cannot guarantee that the information/results will be accurate. Investing in stocks involves risk and could result in losses.