SINGAPORE (ICIS)–A supply glut caused by an

influx of deep-sea butadiene (BD) supply from

Europe and the US is expected to weigh on the

Asian BD market in the near term.

About 150,000 tonnes of BD from Europe and the

US have been heading to Asia since early this

year, with large volumes arriving in the second

quarter and more expected to arrive in July and

August.

“There are also available regional cargoes from

southeast Asia and Japan for July delivery, on

top of the deep-sea cargoes coming, so buyers

are in no rush to commit,” a trader said.

“But the arbitrage window may be closing soon

as demand starts to pick up in Europe and the

US,” another trader said.

The influx of deep-sea BD from the EU and the

US to Asia was triggered by fallout from the

coronavirus pandemic, which has battered the

global automotive industry, disrupted supply,

and crippled demand.

BD is a feedstock for synthetic rubber (SR),

including styrene butadiene rubber (SBR) and

polybutadiene rubber (PBR), which are mainly

used as raw materials in the production of

tyres for the automotive industry.

The shortfall of BD in Asia, due to the planned

and unplanned outages, also prompted EU and US

suppliers and traders to channel their surplus

spot material to Asia.

Taiwan’s Formosa Petrochemical Corp (FPCC) is

shutting down its No 3 cracker and 176,000

tonne/year BD extraction unit for a 45-day

maintenance shutdown in mid-August.

A major cracker operator in South Korea, Lotte

Chemical, is also expected to extend the

shutdown of its cracker and 150,000 tonne/year

BD unit till October, after it shut in early

March due to a fire.

In southeast Asia, Malaysia’s Pengerang

Refining and Petrochemical’s (PRefChem)’s

185,000 tonne/year BD unit has been offline

since mid-March following a fire at the

complex.

In the meantime, Chinese spot appetite has

declined due to the softening local downstream

synthetic rubber market.

“Buyers are holding back as the Chinese

domestic market is softening, and they are also

cautious due to the rising US-China tensions,”

a trader said.

However, Asian BD producers were unwilling to

unload BD below $400/tonne CFR (cost and

freight) northeast (NE) Asia for spot

shipments, given that their margins have been

wiped out by the recent surge in the feedstock

naphtha price.

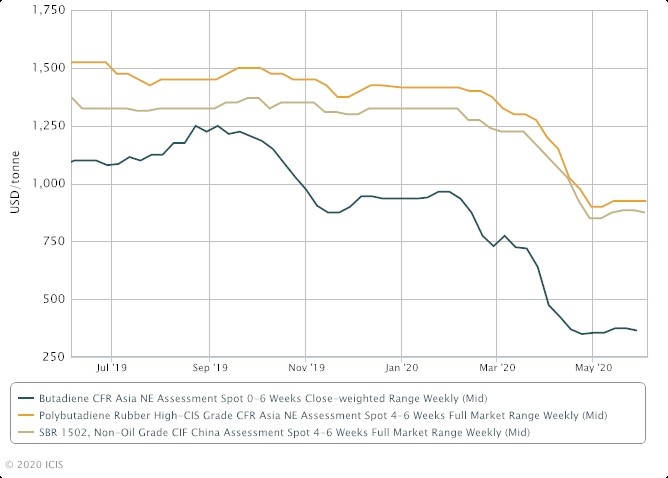

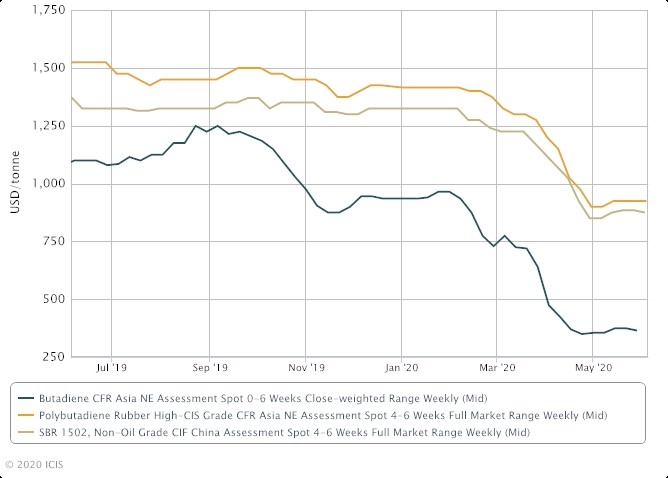

On 29 May, ICIS BD spot price averaged

$365/tonne CFR NE Asia, while the naphtha price

was at $345/tonne CFR Japan at noon on 5 June,

ICIS data showed.

“There are no margins. With naphtha nearly the

same price as BD, it is not sustainable for BD

to remain below $400,” a BD supplier said.

Focus article by Helen Yan

Visit the ICIS

automotive topic page for

analysis of the impact on chemical markets and

links to latest news

Visit the ICIS Coronavirus

topic page for analysis of the impact

on chemical markets and links to latest

news.