In Buffett and Munger’s terms, a business has a moat if it is able to withstand attack from competition to achieve and maintain superior performance.

Some business moats stand out very prominently and are not hard to find. Apple (NASDAQ:AAPL) and Coca-Cola (KO) have brand goodwill that gives them powerful pricing power. They take cheap commodity ingredients, create a brand name product and sell the resulting “mix” at multiples of the cost to produce. Nike (NKE) has a brand-type of moat too. All of these companies outsource their production and focus on maintaining and growing their brand power through design and innovation.

Another type of moat stems from market structure. Some near-monopolies, like Google (GOOG) (NASDAQ:GOOGL) and Facebook (FB), enjoy very robust pricing power from their respective dominant positions in search and social networking. Regulatory attention is another “sign” that we are seeing a moat, although not a very encouraging sign for obvious reasons.

There are two other types of moats that I understand and look for, and there may be others. These come from a business having a clear cost advantage – the low-cost producer – or it having a high customer loyalty/engagement or switching cost. As for a cost advantage moat, it can be underpinned by favorable geographic position or by a process that is intellectually protected or by many other factors. The key is that whatever it is, it cannot be easily copied. Saudi Aramco (ARMCO) may be a good example. This company has single digit per-barrel cost of production. Putting its governance issues aside, it will maintain its relative return advantage because its low cost comes from the geography of its reserves, which are unique.

The final type of moat comes from customer engagement or high switching cost for the customer. Some companies seem very adept at generating great connections with customers. Nike and Apple moats may have some elements of this. Costco (COST) is a great example of a company that has managed to delight customers to create loyalty in one of the toughest fields there is; brick and mortar retail. Germany’s SAP (SAP) would have a high switching cost moat, because of the very high cost, time and risk involved in implementing a new ERP software at a large enterprise.

Businesses with moats like these are expensive to buy. If opportunities open up due to stock market crashes, these businesses should be bought, they are nearly impossible to replace. At other times, I like to look for smaller, less obvious “potential moat” businesses and track them, usually purchasing a modest position and look for further evidence of a moat’s existence to increase allocation or exit. One such business is Expeditors International of Washington, Inc. (EXPD).

Is there a moat in the business?

The most important clue a business may have a moat is a high and sustainable level of return on equity. In addition, such returns need to be “real” and not a mirage caused by increasing leverage. An average company can manufacture good returns on equity by funding growth with debt, especially when interest rates are low. Obviously, there is a limit to this, debt capacity is finite and high gearing raises the risk for all security holders in the process. Just look at shale oil companies today for an extreme example of what can happen when debt-fueled growth goes too far.

High returns are an invitation for competition. This is the method by which capitalism signals the need for capacity addition. It brings back returns to the equilibrium level, a level where return is considered only “fair.” Sustainably high returns are therefore uncommon and serve as evidence that something interesting might be going on.

In the case of Expeditors, before we see the returns, I will briefly introduce the business, as it is not very widely followed. The company is in the “airfreight and logistics” sector. It is a service company, with a small asset footprint and high headcount. Its two freight businesses (air and ocean) do the same thing. They buy large blocks (bulk) of freight space at a lower cost and then sell freight to its retail customers. It also serves as a freight forwarder, simply the logistics service of moving the package from origin to destination on both air and ocean customers. Its other business, unrelated to freight, is customs brokerage and clearance on behalf of customers. Here the company acts as an agent to process goods through customs advising on documentation, valuation, appropriate classification, arranging inspections, etc.

The company is no startup; it has been around for more than 40 years. In its long history, it has experienced many cycles and management makes it a key a point of their business plan to remain a “non-asset” freight provider. They are naturally “short freight” and free from the punishing under/oversupply cycles that recurrently hit ship-owners or regulatory and fuel cost pressure that affect airlines.

This asset-light balance sheet allows the company to run with no debt. This is important because we know debt may distort return. In businesses with some debt, it is enough to check that it is not increasing in relative terms (but there may still be some distortion in time depending on which way interest rates move). No such worries for Expeditors, and the balance sheet is pristine.

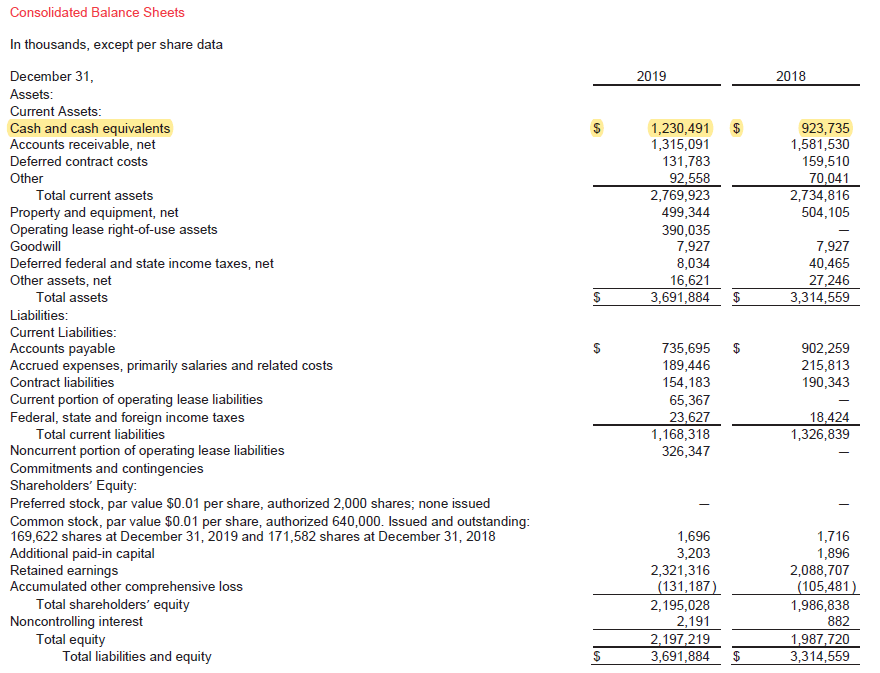

(Source: 10-k)

Note the +$1Bln in cash. I will comment further on this. For now, just remember the size of the cash reserve and note the empty space after “current liabilities” where term debt is usually presented. There is no debt on this balance sheet at all.

The company has not made material of material acquisitions. Accordingly, we find no significant goodwill or intangible assets on the balance sheet. Management actually states in its business plan discussion that it has strong preference for organic growth. We have seen there is no debt; let’s check if the company has needed additional capital through time to grow or maintain its business (either from retained earnings or issuance of shares).

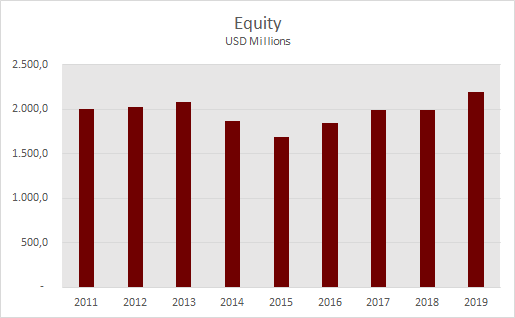

Below is the picture of the equity balance for the last nine years, the answer is clear; the business ran on $2 Bln in equity in 2011 and it runs on $2.2 Bln today, no outside funding has been required.

(Source: Author)

This situation is convenient because it allows us to look directly at cash the business has thrown off and ignore accounting net income commonly used as a numerator in return equations (NI/assets, NI/equity, etc.). Because we can see the business has grown without need of debt or increasing retained earnings, and because we know it does not have any material PP&E to replace, then cash paid is a direct measure of return.

It is rare that you can skip the income statement and just look at cash flow and the balance sheet. Taking cash distributions as return would not be possible if we saw cash payments being made while capex is deferred and depreciation ignored (such a business is effectively in liquidation) or debt increasing to fund payments to shareholders (a type of financial engineering).

This is how distributions look for the nine-year period:

(Source: Author)

The average of these nine distributions is approximately $550m/year. Through the period, equity has averaged just short of $2 Bln, as noted previously, resulting in an average rate of return of 28%. Very acceptable but still not particularly impressive. At this point, I ask you to recall the balance sheet and the cash balance of +$1 Bln. The cash in the balance sheet contributes very little (only interest) to the $550m average payout, yet it “inflates” equity on a dollar-for-dollar basis.

To see the “real” return on equity, I will adjust years 2018 and 2019 to take out the cash.

|

US$ million |

2019 |

2018 |

|

|

Cash on hand |

a |

$1,230 |

$924 |

|

Earned interest (at 1%) |

b |

$12 |

$9 |

|

Dividends and buybacks |

c |

$560 |

$805 |

|

Adjusted div and buybacks |

c – b = d |

$548 |

$796 |

|

Equity |

e |

$2,195 |

$1,987 |

|

Adjusted Equity |

e – a = f |

$965 |

$1,063 |

|

Adjusted Return on Equity |

d – f |

57% |

75% |

(Source: Author)

Taking out the cash allows us to see the true equity employed in the business and its productivity. What remains is a clean picture of the business and its returns. In my view, this level of adjusted return on equity (which is sustained through the backward-looking period) is indicative of a moat hidden within Expeditors.

There is another point to make here. With so fantastic returns, why does Expeditors distribute every dollar the business throws off rather than reinvest it? The reason may be they are unable to find a way to grow and maintain the same returns. This speaks very highly of management, and it takes discipline to invest in only truly value-creating initiatives and release the rest.

A note of caution. It is always possible that returns are temporarily high due to some particular industry condition. It is useful to look at peers and try to see if things are moving in a similar direction and magnitude at other companies. However, good comparables are not always available. An analysis of returns needs to consider the business cycle and use a normalized or long-term average approach rather than point-in-time values to eliminate noise from particular prosperous moments.

What type of moat is it?

I do not see the brand giving the company significant pricing power. As far as I can tell, the moat probably consists of a combination of market structure and customer loyalty. On the market side, this is an $8 Bln revenue company, giving it weight with freight purchases from a cyclical industry in a weaker financial position. On the customer side, loyalty may be more of a factor in the customs brokerage business as opposed to Freight. Freight rates are a commodity, but service value added is higher in the specialized customs brokerage business. Switching costs may be higher as well due to the knowledge/learning curve acquired on specific customer supply practices.

Further weight to the “customer service” side comes from the process the company uses to delegate authority to its district offices and branches. The company allows them to run rather independently with regard to customer decisions, with full responsibility for customer retention at this level. This is matched with a carefully designed incentive structures so that managers behave as business owners of their particular branch. This may be part of the secret sauce.

Conclusion

Finding an under the radar stock with a moat is a valuable thing. Expeditors is not cheap, at around $75/share, it trades at about 20x earnings which makes it hard to call it a value play. However, in relative terms, it is much cheaper than the other businesses mentioned here. My approach is to monitor and buy dips whenever they occur.

Of course, we can never really prove the existence of a moat. Like so much in investing and markets, we need to move between degrees of certainty and probabilities. However, we can borrow from the scientific method to give some structure to our search for moats. In this particular case, the hypothesis, which rests on the observation of permanently high returns, is that there is a moat existing within the business at Expeditors. So far, I have to believe this hypothesis is true, not because I can point clearly to the moat, but simply because I am not been able to prove it does not exist.

Disclosure: I am/we are long EXPD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.