Dividend growth investing is a popular and largely successful approach to generating wealth over long periods of time. We will be spotlighting numerous dividend up-and-comers to identify the best “dividend growth stocks of tomorrow.” Today we take a bite out of The Cheesecake Factory Incorporated (CAKE). We find a lot for investors to like as the company is fundamentally strong, pays a strong dividend, and offers investors a margin of safety via an attractive valuation.

The Cheesecake Factory is a restaurant owner/operating company that operates its namesake restaurant brand in the US and internationally (via license), as well as a couple of smaller subsidiaries in North Italia and Fox Concepts. In total, the company owns approximately 292 total locations in the United States and Canada. There are 24 Cheesecake Factory locations in other parts of the world that operate under a licensing agreement.

The Cheesecake Factory is a restaurant owner/operating company that operates its namesake restaurant brand in the US and internationally (via license), as well as a couple of smaller subsidiaries in North Italia and Fox Concepts. In total, the company owns approximately 292 total locations in the United States and Canada. There are 24 Cheesecake Factory locations in other parts of the world that operate under a licensing agreement.

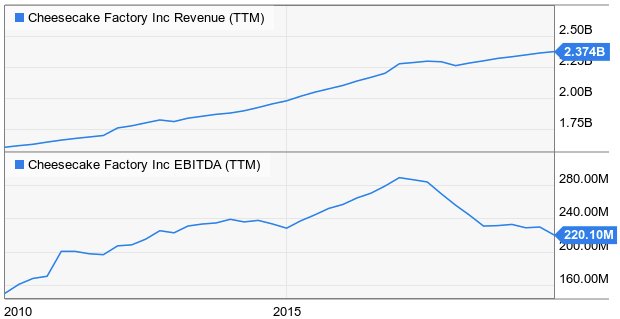

The Cheesecake Factory is a mature restaurant concept, it has been around since 1972. Over the past decade, the business has grown modestly. Revenues have grown at a CAGR of 4.01%, while EBITDA has grown at a CAGR of 3.01% over the same time period.

Source: YCharts

Source: YCharts

Fundamentals

To better evaluate The Cheesecake Factory as a business model, we need to take a closer look at the operating metrics behind the company.

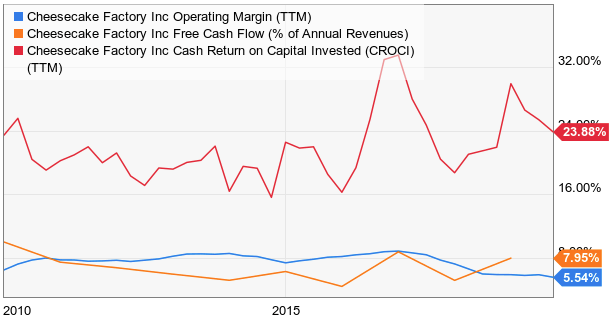

We review operating margins to make sure the company is consistently profitable. We also want to invest in companies with strong cash flow streams, so we look at the conversion rate of revenue to free cash flow. Lastly, we want to see that management is effectively deploying the company’s financial resources, so we review the cash rate of return on invested capital (CROCI). We will do all of these using three benchmarks:

- Operating Margin – Consistent/expanding margins over time

- FCF Conversion – Convert at least 10% of sales into FCF

- CROCI – Generate at least 11-12% rate of return on invested capital

Source: YCharts

Source: YCharts

The restaurant business is extremely competitive – especially casual dining where you have competition from a plethora of both national and local competitors. In addition, you have cost pressures from labor and commodity prices. Cheesecake Factory has seen its operating margin slip in recent years, a trend that we hope to see stabilize and rebound. A mix of pricing, off-location sales (food sold through delivery services such as Grubhub (NYSE:GRUB) for example) and new restaurant concepts (North Italia and Fox acquisitions) can all impact this. Because of the slim margins, FCF conversion sits below our desired benchmark. On the plus side, the company is able to generate strong returns on invested capital, a sign of strong management.

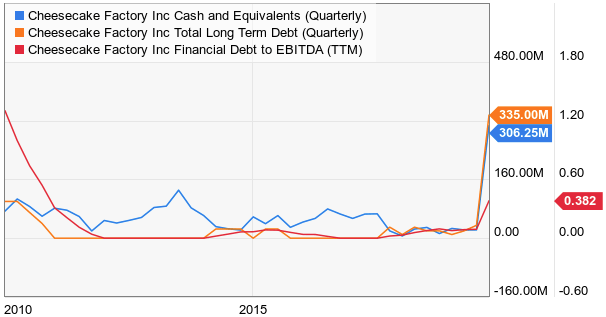

Aside from operations, the balance sheet is another crucial factor when evaluating a company. Too much debt can restrict cash flows, as well as expose investors to risk in the event that the business suffers an unexpected downturn.

Source: YCharts

Source: YCharts

The Cheesecake Factory has done a great job maintaining its balance sheet. The company’s leverage ratio of 0.38X EBITDA is well below our 2.5X cautionary threshold. The company’s cash balance will change upon the next quarterly update because $308 million of that is being used to fund the Fox acquisitions that closed in October.

Dividends And Buybacks

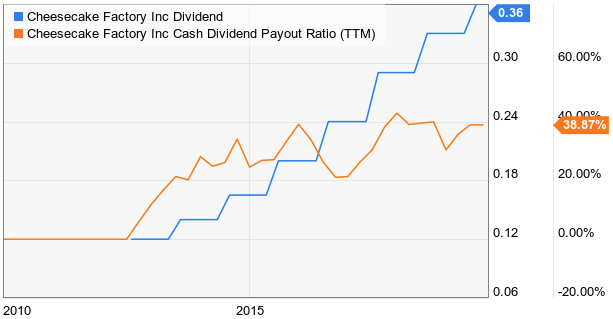

The Cheesecake Factory began paying a dividend in 2012, and it has raised its dividend each year since then. This brings the company’s dividend growth streak to eight years. The dividend is paid out each quarter, and totals an annual sum to shareholders of $1.44. The current yield of 3.32% makes the stock a solid income play. To compare, 10-year US Treasuries are offering just 1.83%.

Source: YCharts

Source: YCharts

Given the dividend’s young age, it makes sense that its growth rate would be pretty strong. Over the past five years, the payout has grown at a CAGR of 19.0%. While the most recent increase of 9.1% indicates that growth momentum is clearly slowing, the dividend’s current payout ratio of 39% indicates further room to grow at a rate that surpasses inflation.

Source: YCharts

Source: YCharts

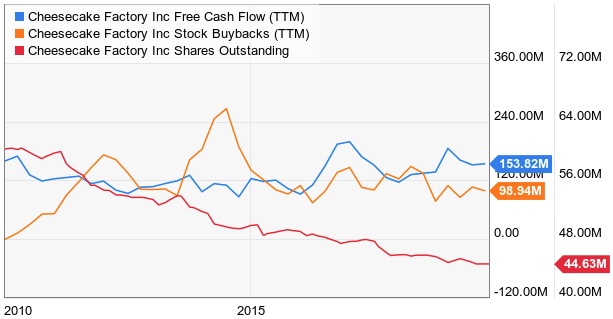

An additional factor in how Cheesecake Factory spends its cash is shareholder buybacks, which management has demonstrated a commitment to over time. As a result, the share count has dwindled from 65 million, to just under 45 million over the past decade. This 30% reduction in shares has helped boost EPS growth.

Growth Opportunities And Risks

The restaurant business is very competitive, so achieving sustained growth over time can be a challenge. The levers that a company such as Cheesecake Factory must pull are multi-faceted. One such lever to pull is expansion. This is pretty straightforward as the more locations you cover, the more of the market you have exposure to. There are currently just over 200 Cheesecake Factory locations in the United States. The company sees about 300 total locations in the US market over the long term.

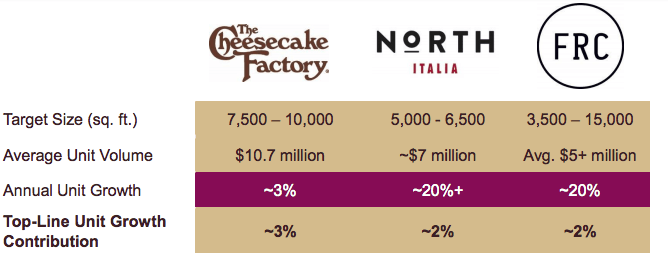

In addition to expansion of its flagship brand, the company recently acquired Fox Restaurant Concepts for $353 million, as well as North Italia for $130 million (after an initial investment of $44 million for a minority stake).

Source: The Cheesecake Factory Incorporated

Source: The Cheesecake Factory Incorporated

The addition of North Italia gives the company some diversity in its offerings, as the brand dabbles in up-scale Italian food. Meanwhile, FRC is a brand incubator that can potentially give Cheesecake Factory upside with emerging intellectual property down the road.

The industry as a whole has felt the impact of innovation through the emergence of to-go ordering services such as Grubhub and Uber Eats (NYSE:UBER). To-go orders now account for 14% of total Cheesecake Factory revenues. Providing a digital access point to the brand should help expand reach, as well as provide more business without impacting seating capacity at restaurants.

The largest threats to Cheesecake Factory are simply economic factors and competition. Like many casual chains, a recession would impact the business as eating out is one of the first budgetary items to go when consumers begin feeling the financial strain. When it comes to competitors, we like the draw that cheesecake provides as a differentiator. Cheesecake Factory’s claim to fame (cheesecake) is a niche item that many people choose the Cheesecake Factory for a meal because of the desire to have cheesecake for dessert.

Valuation

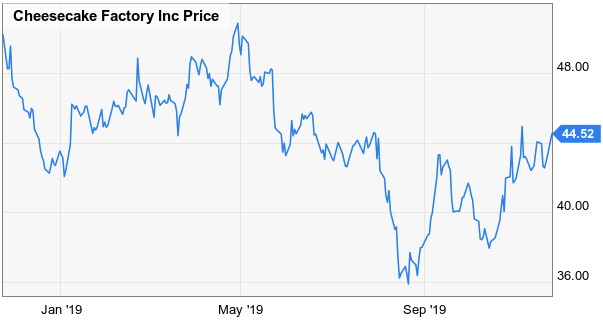

At above $44 per share, Cheesecake Factory’s stock is hovering in the middle of its 52-week range ($35-$51).

Source: YCharts

Source: YCharts

Analysts are currently projecting the company to earn approximately $2.63 per share for the full fiscal year. The resulting earnings multiple of 16.92X is a 19% discount to the stock’s 10-year median PE ratio of 21.01X.

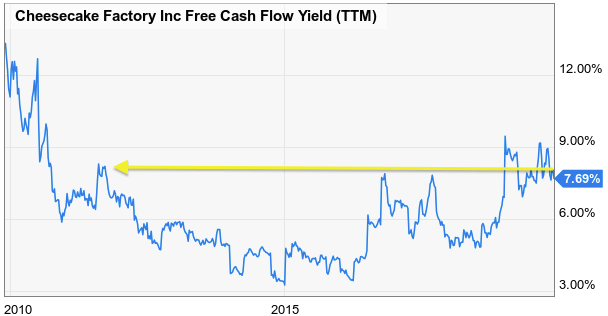

To gain additional perspective on this, we will look at the stock’s FCF yield. This allows us to use cash streams as a measure of valuation. The stock’s current FCF yield of 7.69% is towards the high end of its 10-year range.

Source: YCharts

Source: YCharts

Based on the stock’s discount to historical norms from both an earnings and FCF standpoint, we feel that the stock is attractively priced at its current share price.

Wrapping Up

With the addition of North Italia and FRC, we feel that Cheesecake Factory has solid growth potential in the years to come. The Cheesecake Factory brand is mature, yet there is room for domestic expansion (as well as an international frontier should Cheesecake Factory ever decide to aggressively enter it). The company’s stellar balance sheet and strong dividend yield are also attractive features of the stock. When you combine this with a margin of safety, Cheesecake Factory appears to be a good long-term story to be told in the years ahead.

If you enjoyed this article and wish to receive updates on our latest research, click “Follow” next to my name at the top of this article.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.