Last year was a busy yet transitional period for Denmark’s AP Møller-Mærsk (APMM) and with its annual numbers due on Thursday – the day after Hapag-Lloyd reports its preliminary results – the spotlight will be on a plethora of upcoming challenges and opportunities, perhaps, more than on trailing figures.

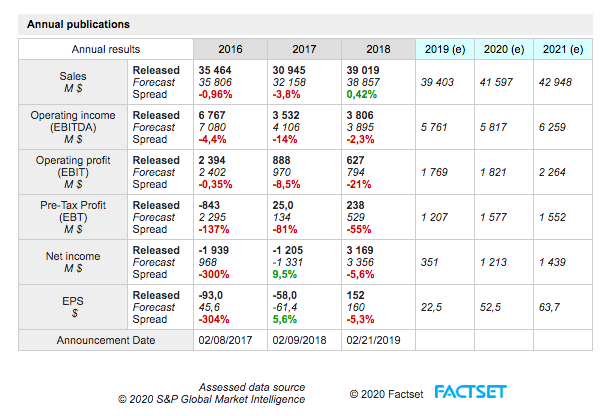

The table below shows what to expect, particularly in terms of top line and ebitda, according to S&P Global Market Intelligence.

(Source marketscreener)

Annual group sales are forecast at over $39bn, broadly in line with 2018 levels, and Ebitda at the high end ($5.8bn) of the guidance range in October, which alongside a better than expected third-quarter performance helped the shares defy the law of gravity until early December. But it didn’t last long.

(At Dkr8,600, the stock currently hovers around the levels it hit on 21 October, when the new ebitda guidance was indeed released)

Estimates for the P&L lines below ebitda are a bit of a leap of faith and ought to be taken with a pinch of salt given several, typical adjustments that have to be made throughout the carrier’s P&L and in light of its performance in the first nine months (9M ’19) of the year…

(Source APMM)

… however, what’s clear is that APMM isn’t growing, although growth is a stated goal through to 2023.

Pillars – what’s core and what’s not

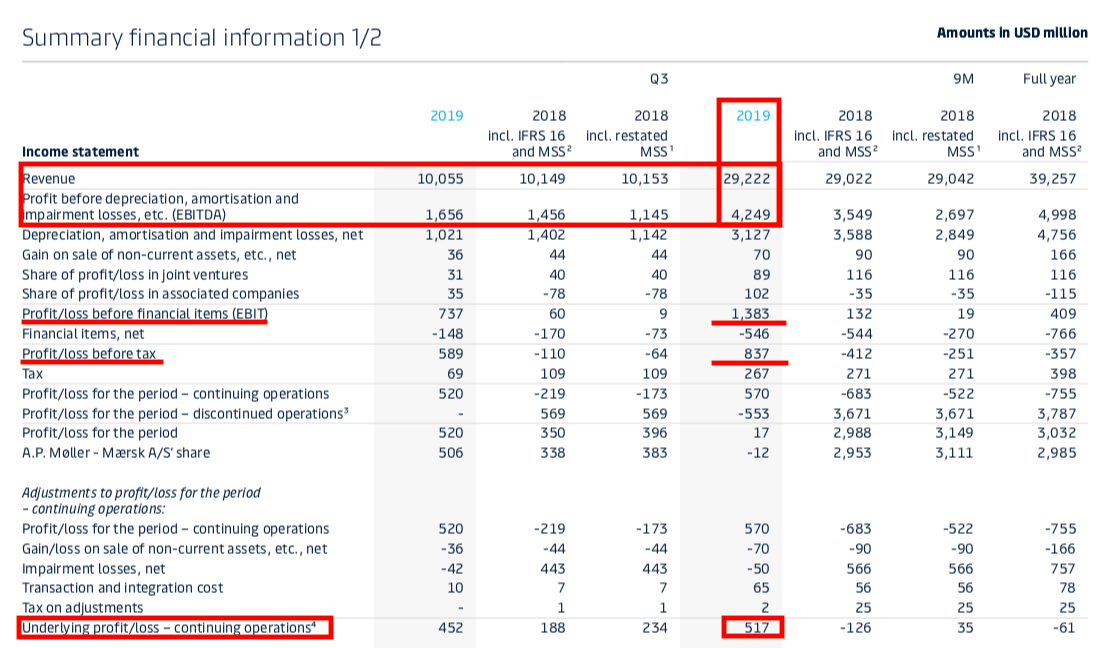

One key element is represented by the underlying profitability of its four units, with its core ocean division sporting a 15.3% ebitda margin and ebitda of $3.2bn in 9m ’19, hence representing three-quarters of group ebitda – assuming the same split for the year, ocean ebitda will likely be in the region of $4.3bn.

While its push in Logistics & Services (L&S) has been widely advertised, thin margins there and ebidta at just about 6% of ocean’s ebitda in 9M ’19 speak volumes about the contribution of the asset-light unit to the group’s profits.

Consider that on an annualised basis, $6bn of revenues means that its L&S size is bang in line with that of a freight forwarder, Panalpina, before it was taken over by DSV, although its L&S ebitda margin is 4.5% against Panalpina’s sub-3%.

(Source APMM)

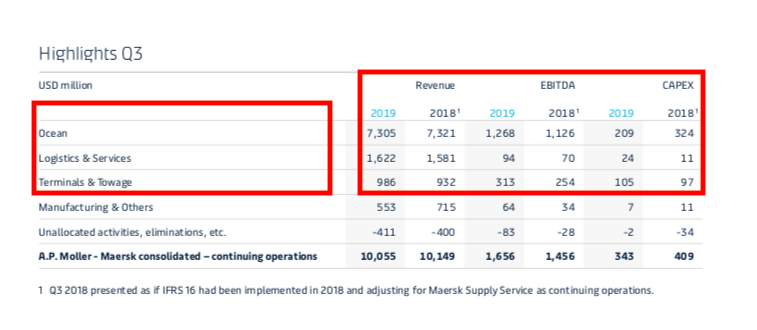

While it doesn’t look like APMM intends to monetise L&S – there was no growth there, as its 9M ’19 results suggest, although Q3 ’19 trends were stronger (see the table below, with capex down in ocean but up elsewhere) – market talk is that options are gauged for Terminals & Towage (T&T), which is significantly more capital intensive than L&S but obviously sports heftier underlying margins and is a rather decent profit pool.

(Source APMM)

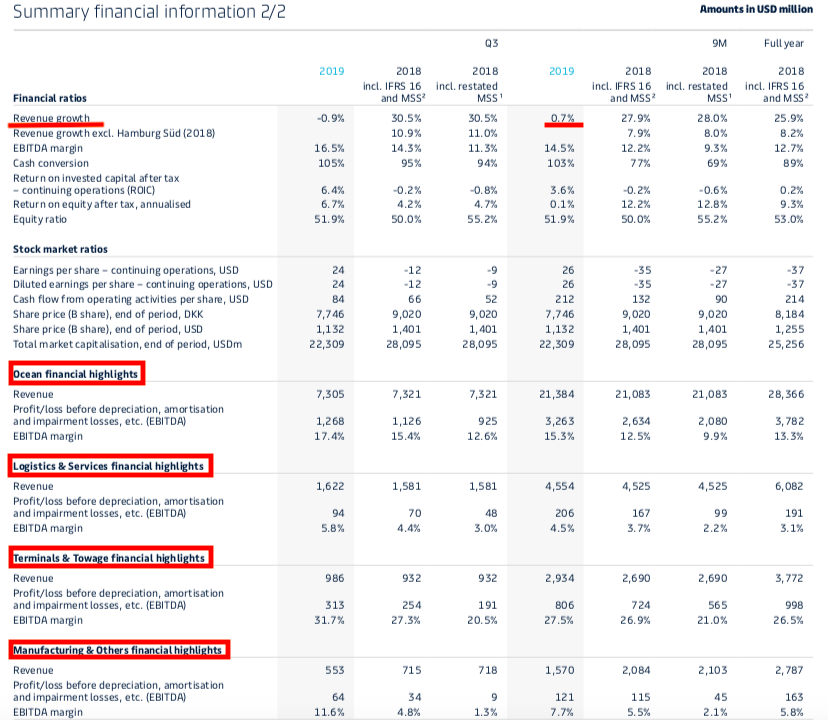

T&T is trickier than others though, strategically, and there are signs that the gateway terminals business could be crucial in its next corporate steps, particularly if APMM wants to become lighter there in terms of capex needs. Performance has been solid, with a 9% revenue growth leading to an ebitda growth of 11.3% in 9M ’19, and margins expanded in the third quarter, despite trends that point to rising labour costs which were offset by lower selling, general and administrative expenses.

A partial spin-off while retaining control of the unit would make a lot of sense if the investment is liquid enough in terms of free float, regardless of the latest news concerning the de-listing of DP World.

CEO Søren Skou recently told CNBC that the ‘phase one’ of the trade deal between the US and China is unlikely to improve flagging volumes at sea any time soon, but APMM and its competitors need more profitable – rather than higher – volumes while managing capacity and adding end-to-end products, trying to prop up rates. Unless, that is, APMM goes for market share, but that is a luxury it can hardly afford, given its finances, I reckon.

Debt in 2019 was lower than one year earlier, but saying it is safely out of the woods would be overstating a financial situation that remains more tied to the cycle than APMM wants it to be, and that’s also reflected in its credit rating that remains just above the investment grade threshold, although the group is committed to it “and will take the required measures to defend our investment grade rating”.

As it plans to keep ocean-related capex at minimum levels well below range this year and next, packaging some good and bad assets with good assets and looking at options for its manufacturing unit could be necessary to preserve returns.

Value hunt

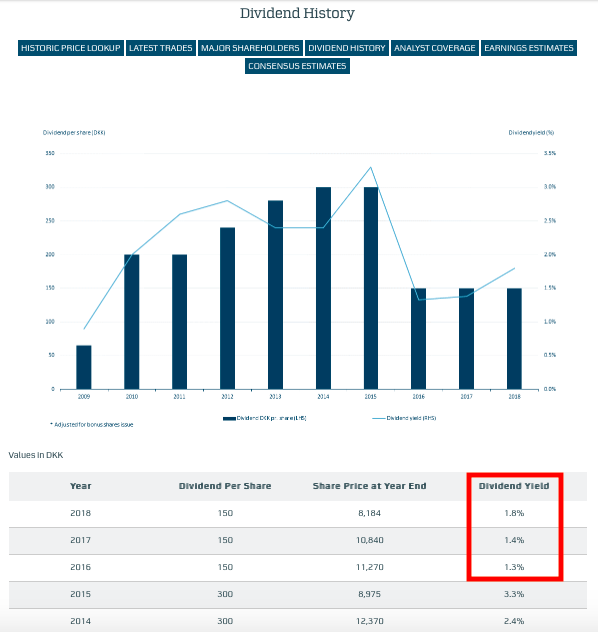

Then take the dividends, which have not been particularly appealing in the past three years, implying a ~ 1.5% yield well below the 2010-2015 reference period, when APMM was… significantly more diversified than currently!

Which invites the question: why wait to bulk up? And why shrink in the first place?

It’s the beauty and curse of corporate strategy.

While the group will likely end up just short of $40bn in sales in 2019, the mid-term target is to add about $8bn in revenues to its 2019 and 2018 base case in order to be as big as before the separation of its energy assets.

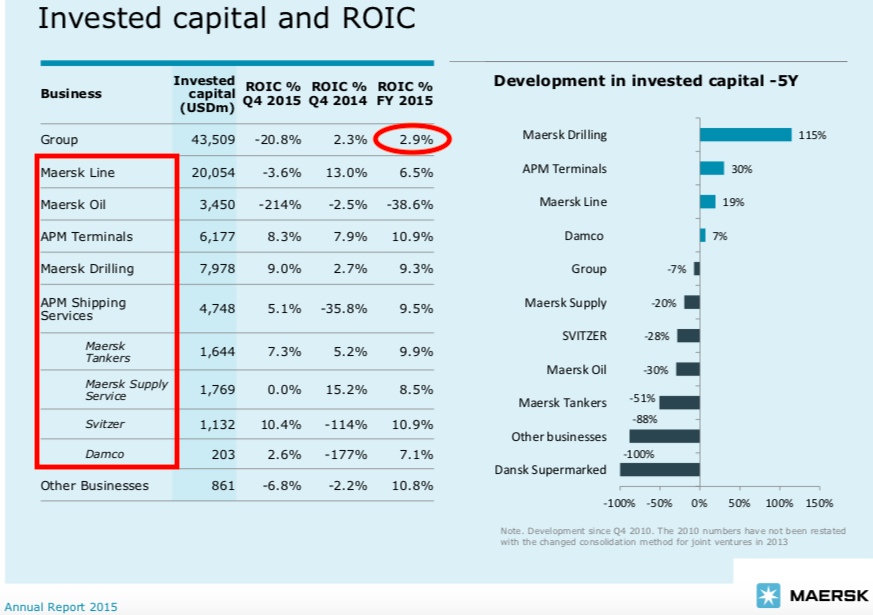

Hence, the sales target might be about $47bn (2014 levels here), when it consolidated a slew of assets that it sold off over time – although in isolation it has little meaning, consider that the ROIC in 2015 was 2.9% versus only 3.6% in the first nine months of 2019, despite all the changes.

Finally, the buybacks.

The group started to repurchase stock in late May 2019…

(Source APMM)

… having spent $941m so far (out of a total authorised amount of up to $1.5bn) for its shares to hit a multi-year low in August, then rally hard and then fall, to stand now some 18% above the levels where it traded at the announcement date in May last year.

Admittedly, share repurchases have provided some protection against downside risk, but other exogenous factors played a part too as is often the case for listed companies. With the “second phase” of the buyback programme drawing to an end it’d be safe to expect more questions about capital allocation as soon as this week – at a time when the kindest remark from senior trade sources is about “very challenging times” ahead in ocean, its core business, as you’d expect.