It has been a rough year for the air cargo industry overall and prospects for a rebound in 2020 are murky because experts say the direction of economic and policy variables remains so unclear.

The downturn started 12 months ago and 2019 is shaping up as the worst year since the end of the financial crisis. Air cargo traffic is expected to contract 3.3% for the full year, with international traffic down about 3.8%, as shippers cope with a global economic slowdown, trade wars, uncertainty over Brexit, sharp drops in automotive shipments and political unrest in places such as Hong Kong. Average freight rates are down 8% to $1.77 per kilogram, according to the International Air Transport Association (IATA).

Nonetheless, on Dec. 11 IATA, which represents nearly 300 airlines, gave an upbeat forecast for 2% growth and slightly better yields next year.

Most industry professionals aren’t willing to go that far yet, especially with signs for a bleak first quarter.

“With today’s uncertainties on the global economy and the challenges we are facing as an industry when it comes to sustainability, for example, it is more difficult than ever to make any projections.The 2% growth is for sure possible, but that would be a rather more optimistic scenario, we think,” Steven Polmans, chairman of The International Air Cargo Association, said in an email.

TIACA represents all segments of the supply chain, including logistics companies.

Research firm Oxford Economics says it now expects global growth to bottom out in the first quarter and slowly pick up to a modest 2.5% for 2020 as governments loosen monetary policy. Others peg next year’s GDP at, or slightly below, the International Monetary Fund’s projected 3% growth in 2019.

IATA has a reputation as an optimistic forecaster, although predicting annual air cargo demand is not easy. Last December, after a strong 2018, the trade group forecast 2019 air cargo growth of 3.7% year-over-year compared to -3.3% – a seven-point swing, according to Jesse Cohen, FreighWaves’ in-house air cargo market expert.

Not everything in IATA’s outlook was rosy. The report said per unit revenue per ton-mile will shrink 3% next year, an improvement from the 5% decline in 2019, and total cargo revenues will slip 1.1% to $101 billion. Average freight rates are expected to drop another 11 cents per kilogram to $1.66, despite the improved volume expectation.

Besides, the airfreight market isn’t monolithic. Certain pockets are doing well, with performance varying by commodity, trade lane and time of year.

International e-commerce, for example, has been a bright spot for many carriers and freight forwarders.

At Chicago-based SEKO Logistics, traditional business-to-business airfreight, especially from China to the U.S., is lower this year, but offset by increases in cross-border shipments for online consumer orders out of China to the U.S., Europe and Africa, said Brian Bourke, vice president of marketing. Overall, SEKO’s airfreight business in the past year is down less than 1%, he added.

Another growth area is exports from Vietnam, Cambodia and Malaysia to the U.S., which have replaced a significant portion of supply from China in recent years as manufacturers shift production to avoid the Trump administration tariffs on Chinese imports as well as rising labor costs in China. Companies are also transshipping partially made goods from China to nearby countries, where final touches are applied before re-export. Illegal transshipment – when finished goods in China are routed through another country and the shipping documents are changed to show the transit point as the country of origin – also contributes to the shift in transport volumes.

But the shifting origin of goods doesn’t change the overall fact that Asia-Pacific trade by air was down about 6% for the first three quarters this year.

Holiday hangover

An indication of weak volumes around the corner is the fact that the peak shipping season typically seen in ocean and air transportation was much shorter and inconsistent than normal in 2019, with volatile demand and rates, logistics executives say.

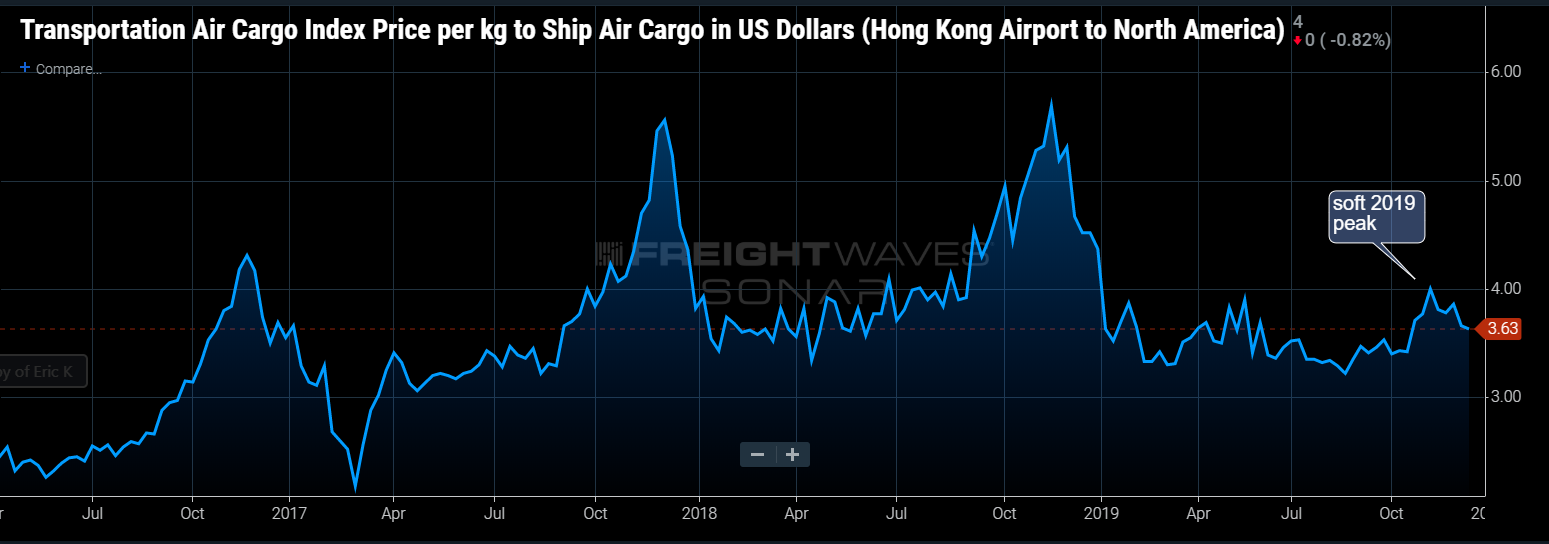

Volumes have increased in the fourth quarter compared to earlier this year, but were down 28% year-over-year in November on the Hong Kong-North American trade lane, according to the The Air Freight Index Co., which benchmarks pricing for the air cargo industry. Then again, last year was a record for airfreight out of Asia.

The weak peak in air can be partially blamed on the ocean container market, said Carlo De Atouguia, chief operating officer of Los Angeles-based forwarder Western Overseas Corp. With overall trade flat in 2019, and many retailers pre-ordering to avoid pending U.S. tariffs on Chinese goods, there wasn’t a capacity crunch this year. Instead, shippers opted for the less expensive water mode because they realized that they could get non-perishable products to market in time without using airfreight, he said.

Western, a smaller forwarder, manages about 140 tons per year by air out of China to the U.S.

Several freight agents said there was a surge of air volumes from mid-October until the first week of December.

Tech-enabled forwarder Flexport had strong business in November coming out of south China, utilizing all of its capacity on its private air service and block space agreements on a number of carriers both to the Americas and Europe, Neel Shah, global head of airfreight, said via email. The chartered 747-400, operated by Atlas Air and painted with Flexport’s logo, was operating three times a week between Hong Kong and Los Angeles, as of early December.

However, the market softened considerably after Thanksgiving and there wasn’t a surge of volume, as some expected, to beat an impending Dec. 15 deadline for new U.S. tariffs on China, Shah said.

(The 15% tariff on about $160 billion of Chinese goods was scratched on Friday, Dec. 12, after the U.S. and China agreed on the first stage of a larger trade deal. The U.S. also agreed to cut by half the 15% tariff rate it imposed Sept. 1 on $120 billion of Chinese goods, while China agreed not to impose new retaliatory tariffs and to buy more U.S.products and services.)

European and U.S-based forwarders say airfreight rates are already dropping as Christmas demand dries up. They predict that soft market conditions could extend into February because a very early Chinese New Year, which begins Jan. 26, makes it unlikely manufacturers will ramp up production for a short period before shutting factories for the nearly two-week celebration.

The sharp transition to low-season demand in January and February sets up a difficult situation for airlines to manage, explained FreightWaves’ expert Cohen. Rates typically drop in the first quarter and a bigger drop could be in order if peak season is already depressed.

“The prices for airfreight are already coming down and that usually doesn’t happen because all the way through Chinese New Year you usually are paying a premium for airfreight because space is so tight,” De Atouguia said.

The soft market out of China will continue through mid-January, then drop further, predicted Luca Ferrera, regional chief for cargo-partner, a full-service logistics provider based in Vienna, Austria.

Hong Kong’s Cathay Pacific Airways is encouraged about January business, given the condensed shipping season, because it is receiving “quite a large number of requests for space,” Fred Ruggiero, vice president of cargo Americas, said.

SEKO Logistics’ Bourke said near-term shipping volumes could depend on post-holiday inventory levels for retailers that shipped ahead to beat U.S. tariffs on Chinese and European goods.

“How much inventory overhang there is, how much restocking needs to be done, remains to be seen,” he said. Also unclear, he added, is whether the shortened time period between Christmas and the Chinese New Year results in a larger flurry of shipping activity, or less, than in years past.

“And if you know what the administration is going to do about trade and tariffs, please let us know,” Bourke said.

Despite the tentative detente between the U.S. and China, tariffs still remain a known unknown in terms of their impact on future trade volumes. Lower tariffs will likely stimulate more purchases from China, all things being equal. But President Trump has proven mercurial and could change his mind if he feels provoked by China on some other issue. No detailed paperwork on the U.S.-China agreement has been publicly released yet. It was still being translated after the announcement, probably won’t be signed until the first week of January and then will take another 30 days to go into effect. The two sides have been close to firm agreements before, only to have talks unravel.

Meanwhile, U.S. tariffs of 25% on a $250 billion list of Chinese goods will remain in place as leverage as the U.S. negotiates for broader, structural changes in Chinese trade practices it considers unfair.

For some, uncertainty doesn’t mean business won’t be good. The New York/New Jersey Freight Forwarders and Brokers Association believes IATA’s forecast is realistic, Vice President of Exports, Jeanette Gioia, said in an email. In fact, with a few forecasts of 3% global GDP growth over the next couple years, continued expansion of e-commerce and potential reduction in trade tensions, “the 2% rate could be exceeded.”

(Jim Smith contributed to this story)