Having fallen from the end of 2021 to the start of 2022, polysilicon prices have slowly but steadily increased for eleven consecutive weeks. In contrast to the hopes many expressed of a significant price fall in Q1, we are left wondering whether prices can exceed the $42.4 average transaction price seen in November 2021.

Prices are about as high as they can be before wafer manufacturers refuse to buy, with 90% of polysilicon sales occurring within long-term contracts based off monthly price negotiations. Most likely there will be a price decline in Q3, followed by another upward blip in Q4, but the tension of supply and demand has ultimately resulted in the same price now as in the middle of last year. The price within China is currently $39 per kilogram and will most likely remain above $31 this year, before returning to more normal levels in the course of 2023.

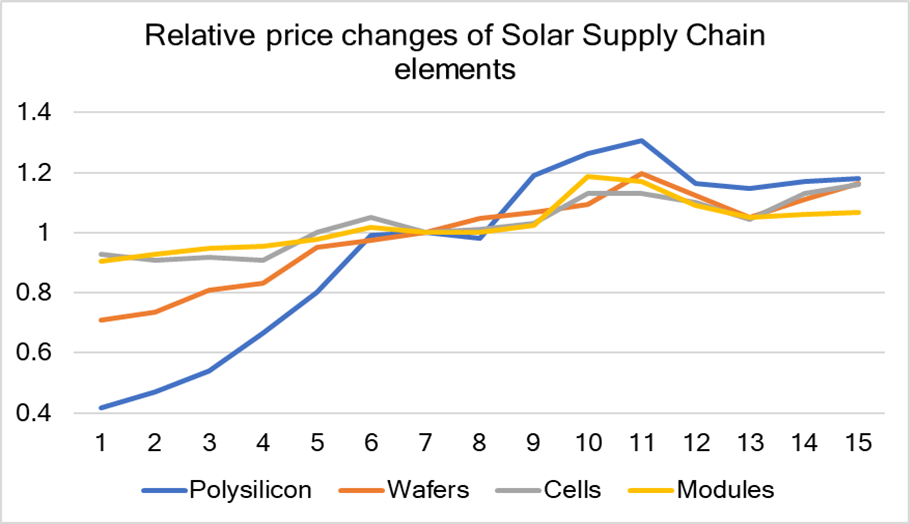

Now is as good a time as any to examine the past year’s prices in each segment of the solar supply chain, to see how costs have been passed onto wafers, cells, and modules. The following data is compiled from a mixture of Chinese sources and covers 210mm wafers, cells and modules.

If we normalize all of these figures to their respective values in July, we can see how the different supply chain elements have reacted to polysilicon price changes – and logically enough you can see that the polysilicon price changes in a given month take one or two months to percolate through to module prices. Whether module manufacturers will lower their prices so rapidly as polysilicon prices return to normality in 2023 is another matter – they will probably not have the luxury of doing so, but they may feel they have to regain some losses incurred from the upstream segment, which would add a few months’ delay.

In our polysilicon manufacturing forecast we predicted 721,600 tons of world polysilicon output in 2022, rising to a million tons in 2023 – but this figure could be exceeded depending on how fast the new factories are commissioned and ramped up.

New estimates from the Silicon Industry Association and other Chinese sources predict over 800,000 tons, perhaps as much as 850,000 tons this year. The huge profit currently turned per kilogram of the material will motivate the sector to construct and ramp up factories as swiftly as possible – and to conduct maintenance in existing facilities as promptly as possible: and the same can be said for restoration work after any floods or earthquakes which may interrupt activities in these factories. The Chinese leadership has ordered new solar development strategy and so it’s also hard to imagine that the polysilicon industry will be molested much by political decisions such as coronavirus lockdowns or emissions-motivated power consumption control orders.

In the first two months of the year 110,000 tons were produced within China, with 100,000 tons expected to be imported in the course of the year (non-Chinese silicon wafer production is negligible, if we count as Chinese the factories located in Indochina and owned by Chinese corporations) – so that points to a guaranteed 760,000 tons prior to the activation and ramping up of new polysilicon factories throughout this year. There’s at least 340,000 tons of new production capacity nominally being commissioned this year, possibly 700,000 tons, but the ramping process requires at least 6 months.

If global supply reaches not 721,600 but 850,000 tons of polysilicon this year, that is enough for an extra 40 GW of photovoltaics to be made – which would see module prices come down seriously in mid-2023 rather than early 2024.

Module prices of $297 per kW are up 20% from their lowest historical point in June 2020. Falling back to $240 per kW by 2025 is guaranteed to happen. There will then be further decline from various minor improvements such as a few % efficiency gain, larger cells and module sizes, and manufacturing efficiency improvements. The two biggest future cost declines for silicon PV are switching polysilicon from Siemens Process to (FBR) granular, which will take a decade to be half-done and heterojunction technology adoption.

Switching to FBR reduces production costs by $12 per kW – so 5% from the 2020 module cost number. Heterojunction adoption improves silicon PV efficiency from 23% to 24% based on current performances, or from 24% to 26% if considering expected near-future performance. That represents 10% cost decline per Watt – but then it costs more to manufacture and is seen as coexisting with less-efficient TOPCON for the foreseeable future.

In other words, once the polysilicon price falls back to historical levels, we will be faced with the reality that almost all of the easy and huge cost declines for silicon PV modules have already occurred. A cost of $200 per kW is achievable, but from that point on it’s up to other semiconductors such as perovskite, CdTe, and CIGS, often in tandem setups, to pick up the slack.

A couple of minor improvements can be seen cropping up in the past year in the cost reporting for wafers. Figures are being produced for a new, larger wafer size – 218mm, slightly increased from the 210mm and 182mm sizes which were the big new categories in 2020 and will be over 50% market share in 2022. Wafer thickness has declined from 175 nanometers to 170 and now 165 nanometers in the past year, an expected measure to use less polysilicon – and some manufacturers are even beginning to produce 155 nanometer wafers. That’s a 15% decline in polysilicon usage, without which the downstream prices in this article’s graph would’ve been significantly higher, but as with other technological improvements to Silicon PV, it has already been pushed close to the absolute limit.

According to statistics collated in the Chinese media, there will be up to 500 GW of solar wafer manufacturing capacity in the world by the end of this year, although some portion of it is going to be ignored due to being relatively outdated in its technology.