Justin Paget/DigitalVision via Getty Images

Peloton (NASDAQ:PTON) is one of those names which earned a sky high valuation out of the gate. The pandemic provided accelerated secular tailwinds and sent the stock soaring even further. At some point you might begin to wonder if you’d ever be able to buy a story stock like this, but after facing both supply chain issues and a broader tech crash, the stock suddenly finds itself trading below pre-pandemic levels. Trading at just 6.5x subscription revenues, the stock is now legitimately buyable on a fundamental basis without much premium being assigned to the long term growth story.

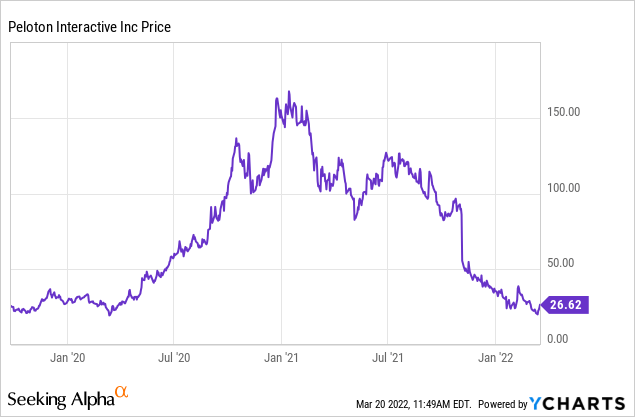

Peloton Stock Price

At one point, PTON traded higher than $160 per share.

YCharts

Since then, the bubble has popped, and then some, as the stock now finds itself trading below pre-pandemic levels. Clearly, the pandemic benefited the company, making this observation highly curious. While one could make the argument that the stock was richly valued before the pandemic, the decline still reflects substantial pessimism regarding the future growth prospects of the company. Excessive pessimism can lead to opportunity.

What is Peloton?

Just to make sure we are all up to speed, PTON is a “connected fitness” company which means it aims to connect technology with fitness. PTON is most well-known for its bikes but it also offers treadmills and general fitness classes.

Peloton 2020 Investor Day Presentation

I have heard the common criticism that PTON is just an “iPad on a bike.” In my view such commentary is unfair and misses the point. PTON is aiming to become the preeminent company in fitness, something like the “Apple of connected fitness.” PTON’s moat currently stems from its world class instructor lineup. While it may not be so difficult to compete with similar products, if you want to work out with the best instructors, you need to be at Peloton.

Peloton 2020 Investor Day Presentation

Peloton Financials

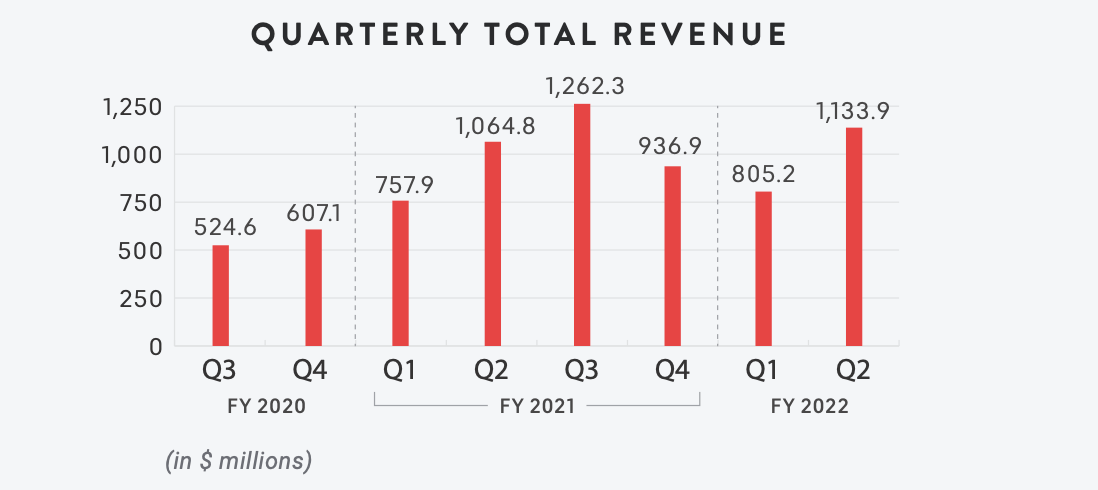

After seeing revenue grow at a 172% rate in Q4 FY20 and 141% rate in Q3 FY21, growth slowed to 6% in the latest quarter.

Peloton FY22 Q2 Shareholder Letter

The company blamed the slowdown on the ongoing supply chain issues, which has prevented the company from fulfilling orders so quickly.

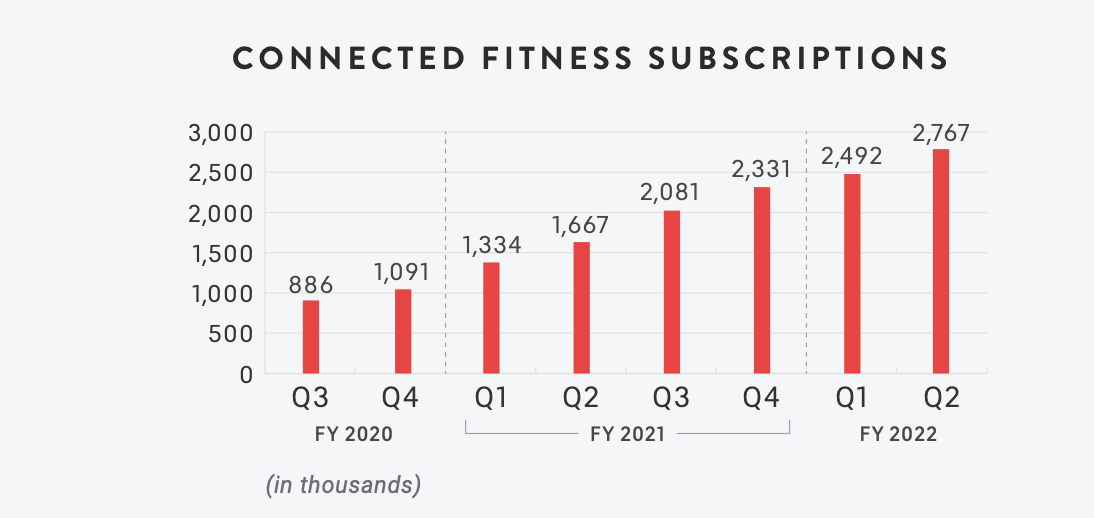

In my view, investors should focus on the subscription side of the business. While the company does get an 11.5% gross margin on product sales, the real margins are in the subscription side of the business, where the company earns software-like 63% gross margins. We can see below that PTON has continued to grow its subscriber base at a steady clip.

Peloton FY22 Q2 Shareholder Letter

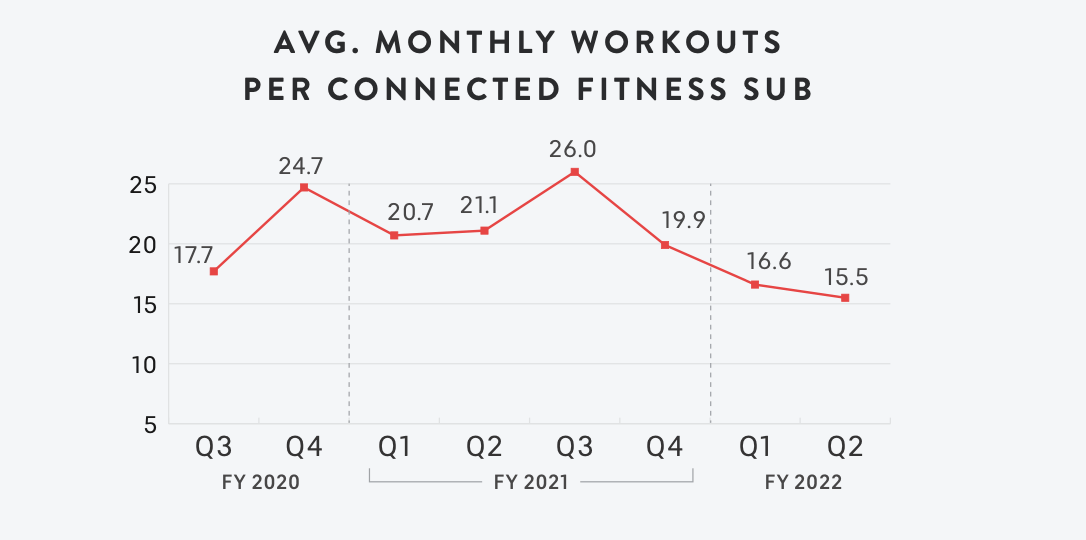

Potentially worrisome is that average monthly workout per subscriber has declined from a peak of 26 only 3 quarters ago to 15.5 in the latest quarter.

Peloton FY22 Q2 Shareholder Letter

The decline makes sense due to people going back to in-person gyms, but this is a critical metric as it can be a predictor of future churn. 12-month retention stood at 92% which was still strong for now.

Is Peloton Stock A Buy, Sell, or Hold?

It can be hard to value PTON due to the low margins on product sales, so one way to look at it is to simply ignore product sales. Wall Street has done this for other similar business models where the company aims to sell a low margin product in order to earn a high margin recurring revenue stream – Roku (ROKU) is another example. PTON earned $337.5 million in subscription revenue in the latest quarter. The stock trades at 6.5x that number annualized.

As of the latest quarter, PTON had $1.6 billion of cash versus $847 million of 0% yielding convertible notes (conversion price of $239.23) due 2026. That represents a net cash position of around 10%, even though the debt effectively represents 0% yielding debt for the next 4 years. PTON has guided for $125 million in adjusted EBITDA loss in the next quarter, raising the possibility that there may be another capital raise over the next 12 months.

On the conference call, management guided for stronger margins and cash flows moving forward as the company winds down its inventory balance. I expect the pandemic-related supply chain issues to be a short term issue and resolvable over time. I can see the company returning to 20% growth or better once those issues are resolved. If we assume that the company can achieve 30% long-term net margins based on subscription revenues alone, then the stock is trading at around 21x long term earnings power, representing a highly conservative 1x price to earnings growth ratio (‘PEG ratio’). If PTON can get its groove back, then I can see the stock trading up to at least a 1.5x PEG ratio, representing 50% upside from multiple expansion alone.

The key risks here are if PTON is unable to sustain market share moving forward or if the company sees churn rates elevate higher. Regarding churn rates, I am not so worried about this risk because it seems likely that once one has spent $1,500 or so on a Peloton bike, they’d want to keep a subscription to justify that cost. Further, PTON is disrupting an industry that has historically not seen much technological disruption. I expect the digital and at-home secular growth tailwinds of the fitness industry to be long lasting, with PTON being a clear leader. Investors should watch out to see if competitors like Apple (AAPL) are able to steal market share from the connected fitness market, but for now that risk looks overblown as PTON is much more focused on this market.

I rate the stock a buy due to the conservative valuation based only on subscription revenues. The stock is of higher risk due to the near-term cash flow issues, but longer term I can see this being a big winner.