Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Jet Freight Logistics Limited (NSE:JETFREIGHT) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

Check out our latest analysis for Jet Freight Logistics

What Is Jet Freight Logistics’s Net Debt?

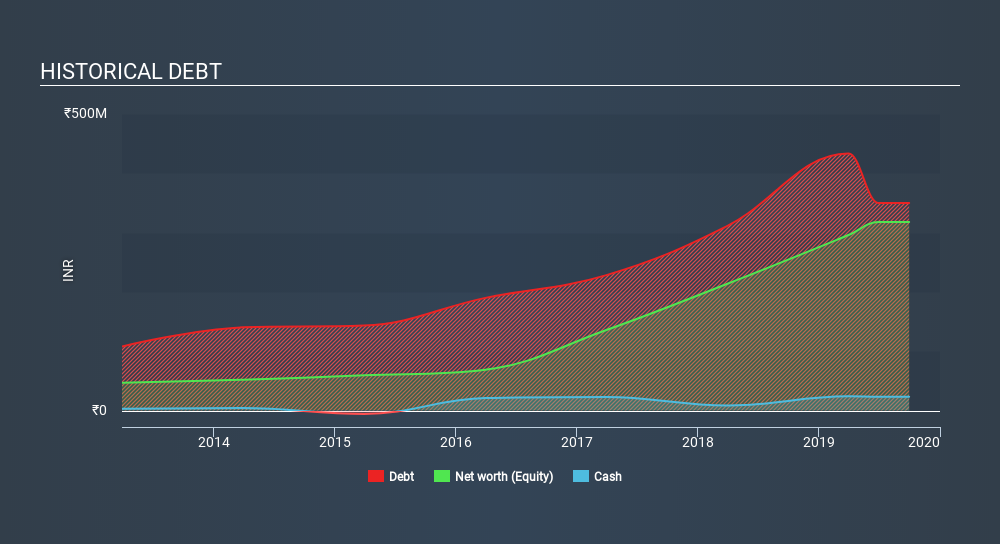

You can click the graphic below for the historical numbers, but it shows that Jet Freight Logistics had ₹349.8m of debt in September 2019, down from ₹433.2m, one year before. However, because it has a cash reserve of ₹23.2m, its net debt is less, at about ₹326.7m.

A Look At Jet Freight Logistics’s Liabilities

According to the last reported balance sheet, Jet Freight Logistics had liabilities of ₹548.1m due within 12 months, and liabilities of ₹106.8m due beyond 12 months. On the other hand, it had cash of ₹23.2m and ₹659.7m worth of receivables due within a year. So it actually has ₹27.9m more liquid assets than total liabilities.

This short term liquidity is a sign that Jet Freight Logistics could probably pay off its debt with ease, as its balance sheet is far from stretched.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Jet Freight Logistics has net debt worth 2.4 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 3.2 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. We saw Jet Freight Logistics grow its EBIT by 7.7% in the last twelve months. Whilst that hardly knocks our socks off it is a positive when it comes to debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can’t view debt in total isolation; since Jet Freight Logistics will need earnings to service that debt. So if you’re keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Jet Freight Logistics burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Jet Freight Logistics’s conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to to handle its total liabilities isn’t too shabby at all. Looking at all the angles mentioned above, it does seem to us that Jet Freight Logistics is a somewhat risky investment as a result of its debt. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you’ve also come to that realization, you’re in luck, because today you can view this interactive graph of Jet Freight Logistics’s earnings per share history for free.

At the end of the day, it’s often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It’s free.

If you spot an error that warrants correction, please contact the editor at [email protected]. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

Discounted cash flow calculation for every stock

Simply Wall St does a detailed discounted cash flow calculation every 6 hours for every stock on the market, so if you want to find the intrinsic value of any company just search here. It’s FREE.