Thesis

Recessionary fears have been whisked off of investor minds like a bad dream. No sector is immune to challenging macroeconomic conditions, but the transports bear the brunt of a slowdown.

This subjects the transports to cyclical concerns as risk-averse investors may choose to avoid the sector entirely. Along with cyclical concerns, the transport sector is generally highlighted by low growth and high leverage. But the efficient movement of goods from one place to another is a backbone of the economy. Dow Theory is a questionably reliable technical indicator, but more importantly is symbolic of the underlying driver of economic activity. The transportation industry has an intimate understanding of the risk-on and risk-off thinking behind investment spending decisions that drive economic activity.

Regardless of how far the pendulum swings in the direction of a service-driven economy, there will always be goods to move and opportunity to cut waste throughout supply chains. One business doing just that is XPO Logistics (XPO).

Data by YCharts

Data by YCharts

In a typical fashion of “throwing the baby out with the bath water,” XPO cratered in late-2018 from company-specific issues covered in my previous articles here and here, along with concern over XPO’s debt level as the Fed tightened. While macro technicals change daily, good businesses do not. XPO Logistics has the highest of quality management teams at the wheel, along with a strong business model built around a desirable structure to provide investors with excess returns over the long term. Since Brad Jacobs’ private equity firm acquired a majority stake in the business in 2011, revenue has grown by 100x. With XPO’s track record, current direction, and positive future outlook, I am confident in owning XPO Logistics and believe it will be a high compounder over the long term.

Cash Is King

We’ve been in an industrial recession for over a year. – Brad Jacobs

Jacobs has cited tariffs as the primary cause of the challenging environment for the industrials. The lose-lose dynamics surrounding tariffs slowing the global economy are well documented and will hopefully reach resolution. While the playing field has been negatively impacted, the players have not been. They are simply forced to move a bit slower. Like a football player on a snowy field opposed to dry ground on a bright sunny day.

XPO has done just that. Revenue and cash flow has fallen slightly, but remains strong. XPO’s gains have come on the income statement, as efficiency-driven advances have improved operating margins up towards 6%, up from 3% just two quarters ago. The chart below is much more impressive when considering the tight freight market that lasted into 2018 compared with current tariff caused weakness.

Data by YCharts

Data by YCharts

Operating cash flow is down from 1.1 billion in 2018 to 1 billion over the trailing 12 months. While obviously a decline is negative, XPO still has a billion dollars to do whatever it chooses with. At a 7.5x cash flow multiple, XPO is cheaper than J.B. Hunt (JBHT) at 10x and Old Dominion (ODFL) at nearly 16x. XPO also has a much clearer path to growth and expansion.

XPO is even cheap on a historical basis. The company ended 2017 at a 14x cash flow multiple, but investors did get a chance to buy at the dirt cheap multiple of 5.5x at the conclusion of 2018. Even with a very reasonable 10x multiple, the stock has 30% upside from the current levels without any growth, which won’t be the case when M&A activity resumes. Cash flow is a good indicator of business strength, but Capex is also important to consider.

In the past, XPO has done a brilliant job of allocating its capital. Management is careful, sensitive, and prudent when considering how it uses its cash, especially in relation to potential macro pitfalls.

And now you’re seeing the business, in our case, be able to generate positive year-over-year comps, even beats, in a slow economy. In supply chain specifically, there is an interesting phenomenon of what happened in the great financial crisis in the largest of the four contract logistics companies that we bought, New Breed, where their EBITDA actually went up and up substantially in 2008 and 2009. So, we’ll see what type of recession we have and when we have it, but so far, so good. – Q3 Earnings Call

Jacobs has previously stated that XPO expects free cash flow to grow during a recessionary period as the company trims growth CapEx. In Warren Buffett’s classic examination of “owner earnings,” Buffett distinguishes the difference between maintenance CapEx and growth CapEx.

…less the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume. (If the business requires additional working capital to maintain its competitive position and unit volume, the increment also should be included… – Warren Buffett

On a previous call, it was mentioned XPO’s maintenance Capex to be in the range of $200-225 million, or just under 40% of the company’s total Capex for FY2018. The company used the additional spending to grow the business and also saw income from disposal of assets. The company chose to deploy its free cash flow to pay down some debt, but mostly to execute a perfectly timed share buyback program.

Whether or not share buybacks increase intrinsic value can be debated. For valuation purpose, XPO gobbling up nearly a quarter of the shares makes a huge difference in shareholder value. For instance, let’s assume Citi’s $200 share price forecast comes true. With the current 92 million shares outstanding, XPO’s market capitalization would be $18.4 billion. With the previous 127 million share count, an $18.4 billion market cap would result in a $145 stock price. The difference to investor portfolios is a gain of 144% over 77%; I’d prefer the former. The logic is quite simple, I now own a greater portion of XPO’s future cash flows.

Operational Improvements

Understanding XPO’s strong cash flow generation and management’s track record of value creating activities should be enough to excite investors. We also must understand where we expect the business to go into the future.

As mentioned, XPO has seen meaningful margin expansion and productivity improvements as a result of its technological initiatives. While the notion that “every business is a tech company” is becoming somewhat cliche, XPO has the margins to prove it. The company is focused on optimizing labor costs, LTL improvements, and automation.

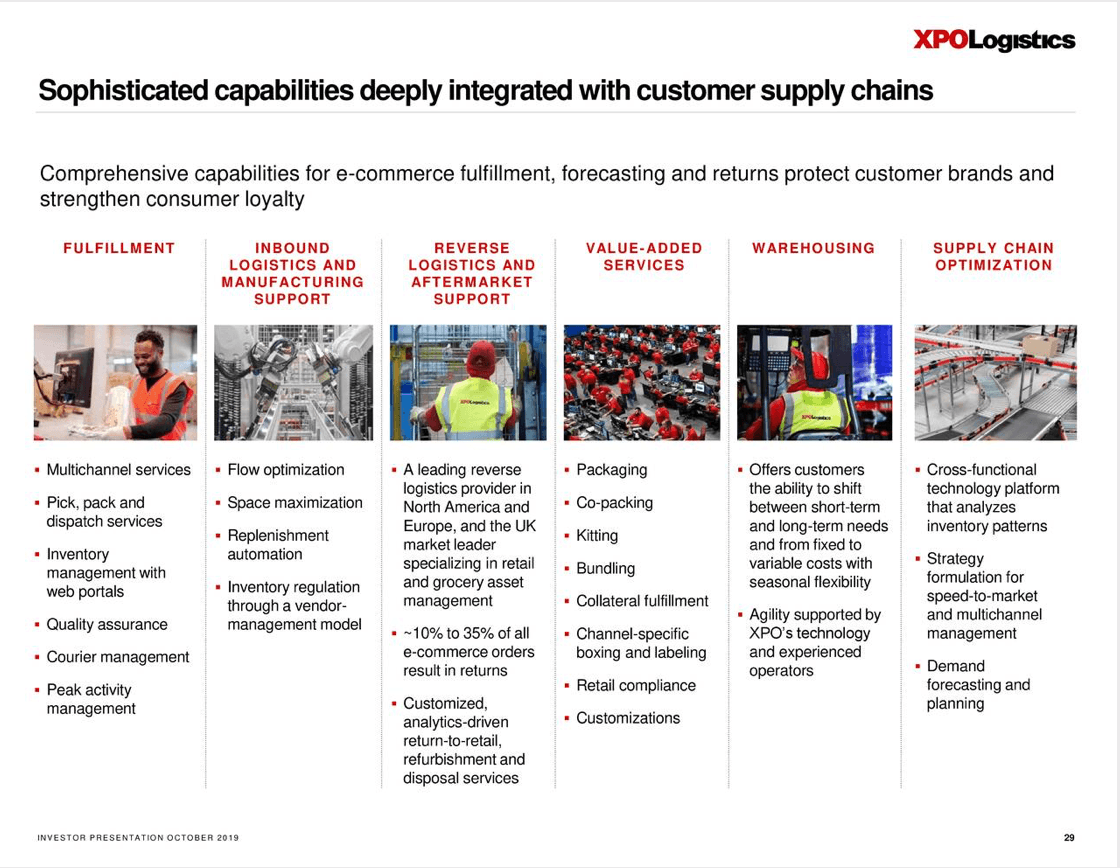

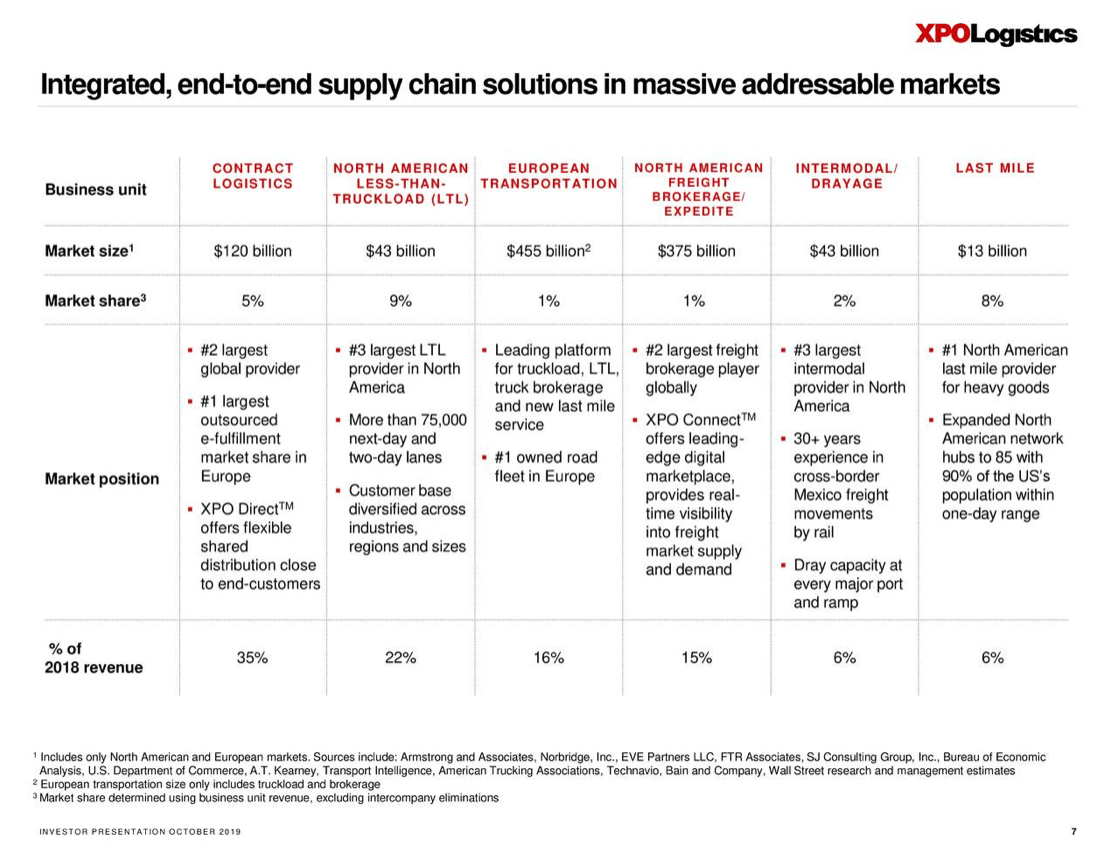

XPO’s physical assets give it an entrenched logistics ecosystem that is crucial to customers’ supply chains. XPO’s scale enables it to deliver a superior end-to-end supply chain solution. Through M&A expansion, the company has grown the number of services used per customer. High dollar customers create an advantageous opportunity to expand from within current customers’ operations, enabling decreased spend on customer acquisition. SG&A was a $1.9 billion expense over the past 12 months, representing yet another opportunity for XPO to expand margins. XPO’s strength across a number of transportation and logistics segments enables this process.

XPO’s focus on technology doesn’t stop at just improving operational processes. XPO Logistics also stands to benefit from the growing shift to e-commerce. XPO is the largest last mile deliverer of heavy goods, a market that will grow as e-commerce expands. XPO Direct will leverage the company’s scale to assist businesses without strong distribution capabilities such as Amazon (AMZN). XPO has a degree of internalized network effects, so as the business grows, its customers benefit from improved efficiencies and supply chain abilities. The transportation industry is highly fragmented, and XPO’s scale is hard to match. The assembly of highly valuable assets is not an easy endeavor; this secures XPO a place in the massive industry.

XPO’s transformation over the past decade is nothing short of remarkable. XPO has a clear path to drive more efficient movement of goods, making the company a valuable partner to businesses looking to optimize supply chains. Don’t expect stagnation at XPO either; it is dipping its toes back in the M&A waters. Brad Jacobs’ dealing making prowess could reignite the top line.

Conclusion

Long term investors should not worry about short-term fluctuations. XPO Logistics’ share price roller coaster is not an accurate reflection of business performance. There is no practical way in predicting cyclical downturns. Investing using core principles that assess business quality and cash generation ability will succeed over timing cyclical downturn.

XPO is a clear best of breed in the transportation sector at a fantastic price. Weariness of cyclical businesses is not unfounded, but XPO has managed to succeed despite various headwinds. It scores highly in pure business quality and value. XPO is a stock to own for long-term, marketing-beating performance.

Disclosure: I am/we are long XPO. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.