Global transportation and logistics player XPO Logistics’ (XPO) share price has been on a roller coaster ride for the past few years. The year 2019 was far from great for the company. Prominent amongst the reasons for much of the poor performance was the loss of business from a big customer, potentially Amazon (NASDAQ:AMZN), and significant criticism by short-seller Point Capital.

Keeping these problems behind, the company had started rising in early 2020 only to get dashed again by concerns surrounding the ongoing pandemic. On March 19, the stock had fallen as low as $38.47. Although the stock is 110.66% up from its March low, it is only 1.68% up on YTD (year-to-date) basis. Considering the manner in which the global economy has started revving up, albeit at a slower pace, I believe that there is still room for XPO Logistics’ share price to go up in the rest of the calendar year 2020.

Demand seems to be perking up in various areas of the global economy

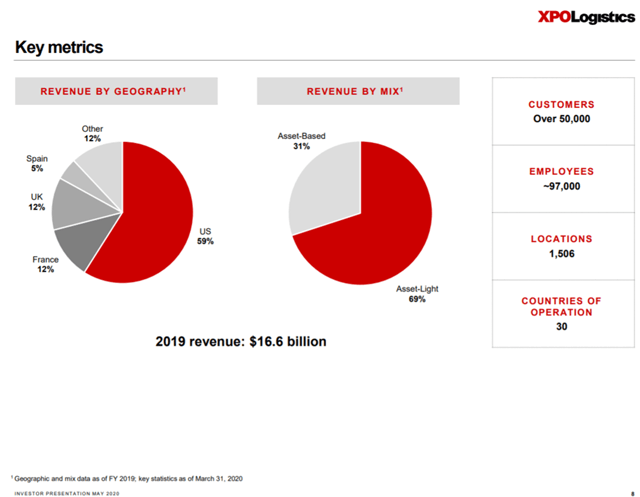

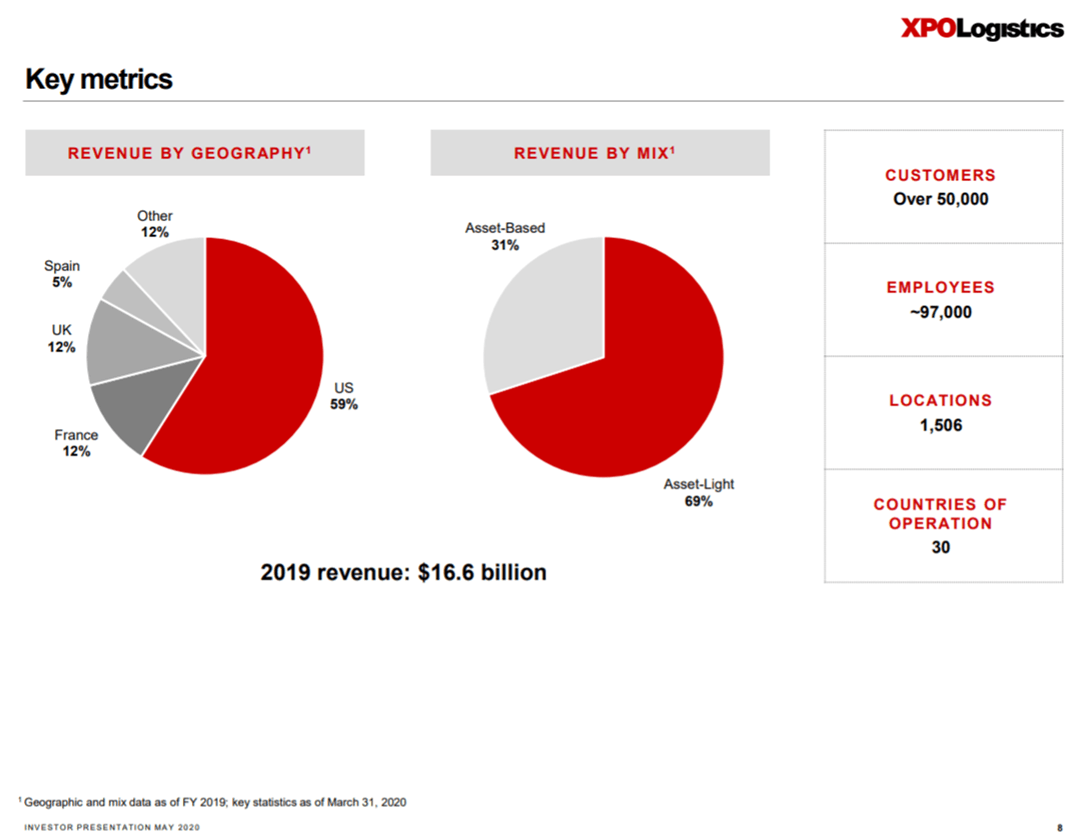

XPO Logistics is one of the top ten global transportation and logistics company with an annual turnover close to $17.0 billion. The company is the third-ranking for-hire transportation company, fourth-ranking LTL (lower-than-truckload) company, and the first ranking provider of home delivery of big and bulky goods in North America. XPO Logistics is also the leading global contract logistics company.

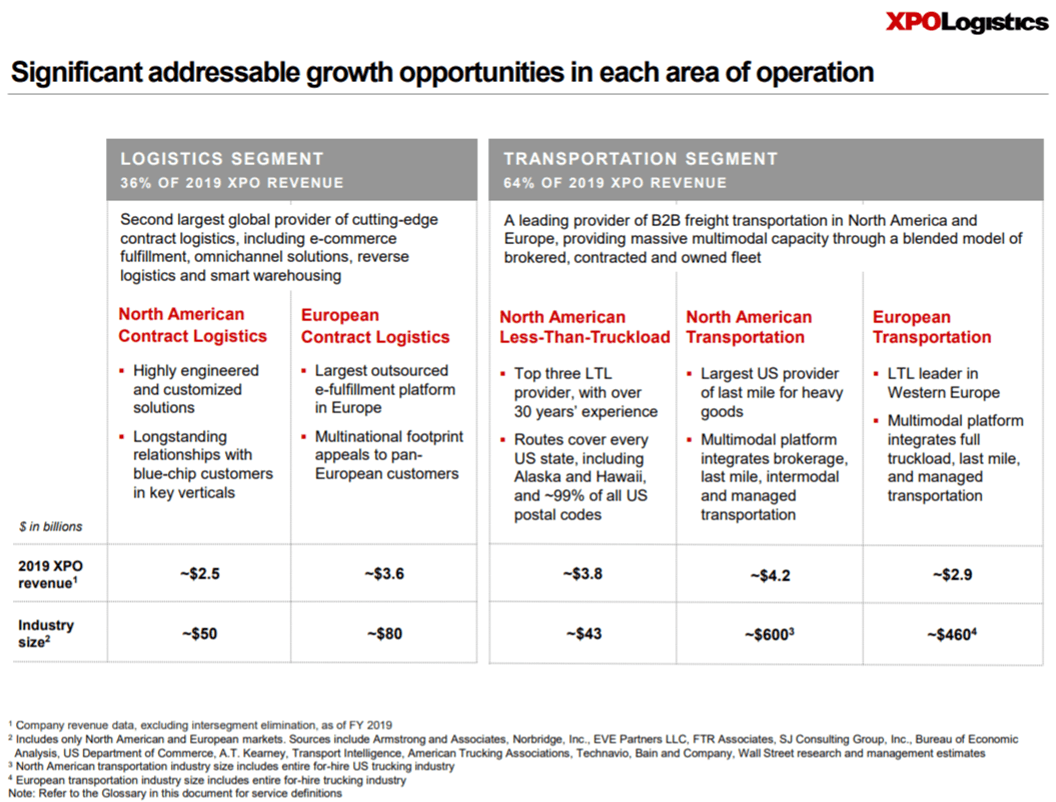

XPO Logistics is a leading player in multiple market segments with long-term growth potential and durable demand trends. The company currently holds only a 2% share of the above addressable market opportunity and hence has much scope to grow in the long term.

The short-term trends are also moving in the right direction. The U.S. Truckload market has been slowly but surely improving since the end of May 2020. According to Coyote’s Truckload Market Update for July 2020, this market is seeing a jump in spot rates and volumes after bottoming out in April 2020. The report attributes these trends to the limited opening up of the economy and a slight increase in consumer spending. However, the volumes, although going up in the right direction, are lower by around 20% than what would be typical for this period of the year.

Coyote also expects the USMCA (US-Mexico-Canada Agreement), which is bipartisan tooling of the 1994 NAFTA Agreement, to be a major growth driver for the U.S. Truckload Market. Since Canada and Mexico account for 30% of U.S. trade worth almost $1.225 trillion trade, this agreement is a major positive for the truckload segment.

Bank of America’s proprietary bi-weekly BofA Truck Shipper Survey Rate Indicator has also highlighted the improving demand trends and pricing environment, as well as tightening capacity in the trucking sector. Citi Bank’s recent trucking shipper survey also reaffirmed these opinions.

These trends will benefit XPO’s transportation business. The company has reported improvement in its LTL business, last-mile delivery, and contract logistics business in the U.S.

In Europe, the contract logistics business has seen increasing demand from segments such as e-commerce, food, and beverages. The company expects the European transportation business to perk up in the coming months. However, the recovery depends largely on the state of economy considering that the transportation business mainly caters to construction, automotive, and industrial segments. Europe remains a major market for XPO considering that it accounted for almost 40% of the company’s total 2019 revenues.

The company has a resilient business model

While the transportation and logistics sectors are mostly cyclical, XPO Logistics has managed to limit the downside by building a fairly resilient business model. Certain characteristics of the company’s business model have positioned it far better than its peers.

XPO Logistics operates through two business segments, transportation, and logistics. Approximately, 64% of the company’s revenues come from the transportation business while the remaining 36% comes from the logistics business. The company serves approximately 50,000 customers across the U.S. and Europe. The customers vary based on their sizes, geography, requirements, and industry. A diversified customer base is key to preventing extreme revenue and earnings volatility. This is especially important during a recessionary environment.

XPO Logistics has also developed an asset-light business model. In 2019, the company’s net capex was only 2.1% of the total revenues. Contract logistics is an especially lower capex business and has strong free cash flows and returns on invested capital. The company’s contractual logistics business also helps reduce revenue volatility and offers a certain degree of visibility. This business is less cyclical than the transportation business and involves long-term contracts with clients.

Excluding the LTL business, the company’s transportation segment is also asset-light. The company’s transportation business is also relatively resilient and banks on long-term relationships with customers. This is a major differentiator in the asset-heavy transportation and logistics industry. Asset-light businesses have inherent protection during economic downturns.

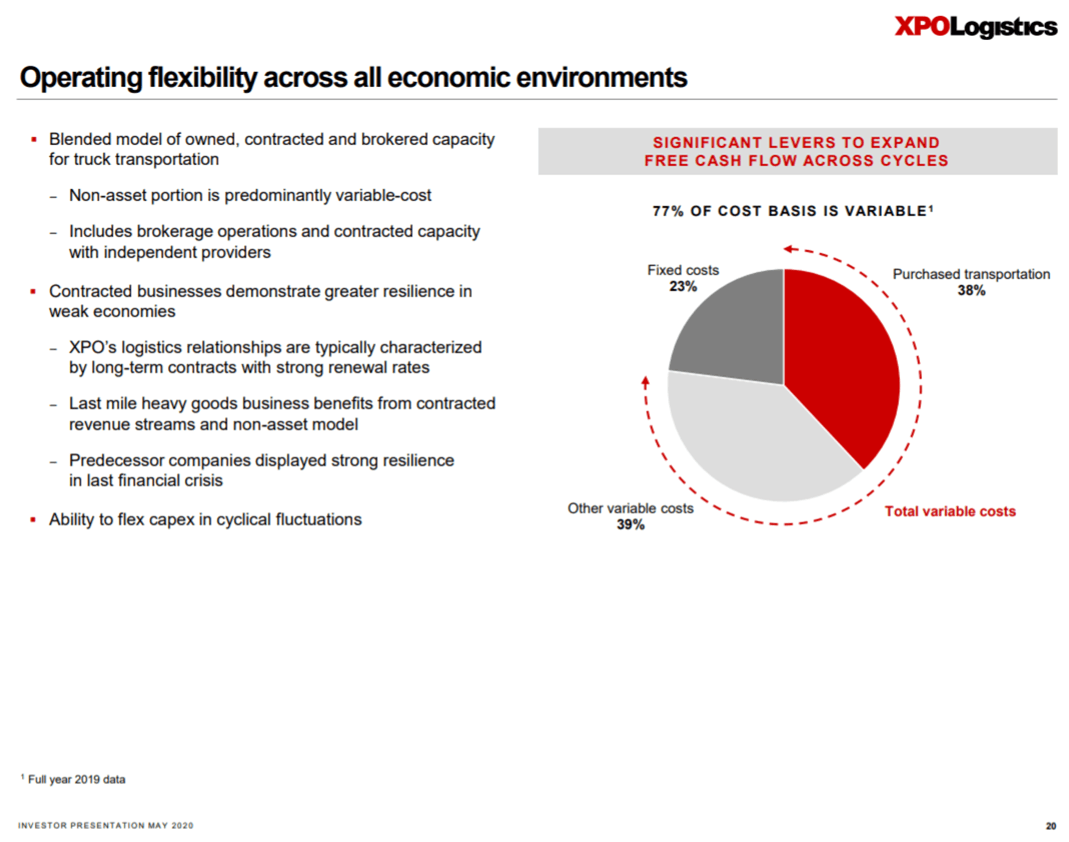

In addition to low capex requirements, the company also enjoys a high degree of operational flexibility since 77% of the costs are variable. This protects the company in recessionary times, considering that XPO can scale down both capex and operating costs quite quickly.

The company’s scale also helps the company to further explore cross-selling and innovation opportunities. It enables the company to optimize costs through increased purchasing power and operating leverage.

The diversified revenue base, huge scale, and flexible cost structure enabled the company to surpass EPS estimates even in the first quarter of fiscal 2020. While revenues fell YoY by 6.21% to $3.86 billion, which was short of the consensus by $103.73 million, EPS of $0.47 was ahead of the consensus estimate by $0.04. The company also reported CFO (cash flow from operations) of $180 million and free cash flow of $95 million in the first quarter.

The company is differentiating itself in this crowded and fragmented transportation and logistics market by leveraging technology

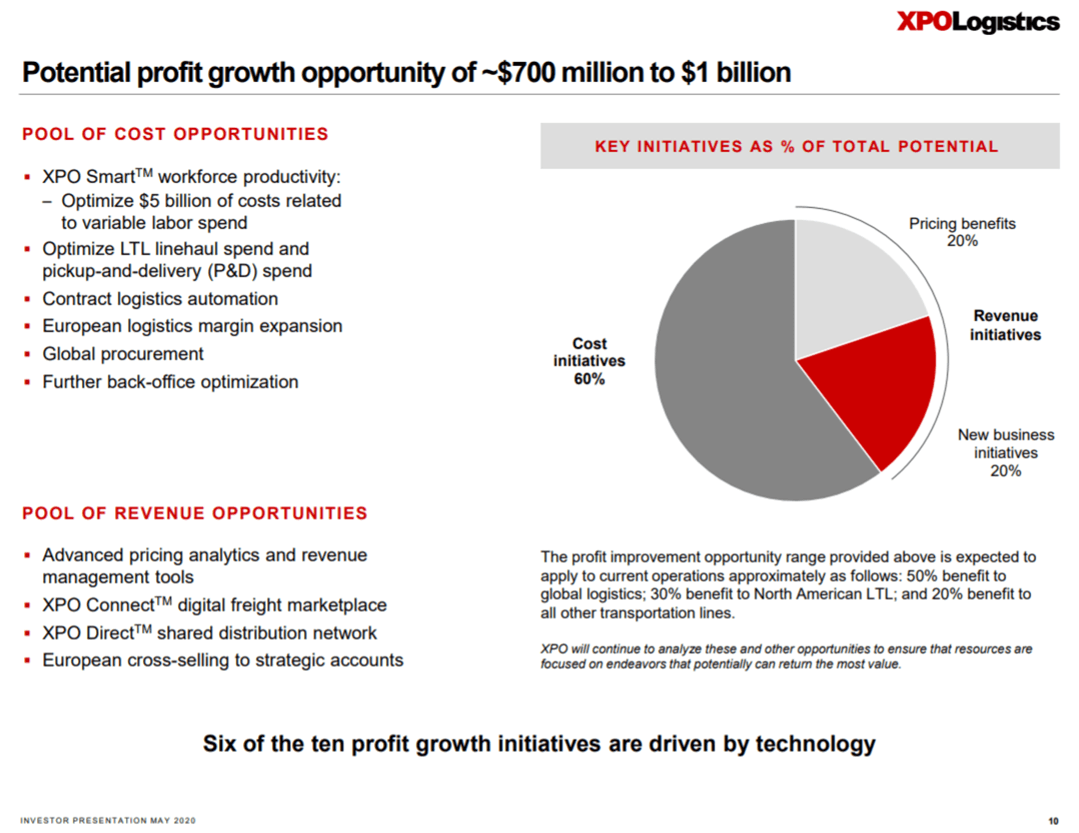

XPO Logistics has designed ten initiatives to generate long-term annual profits in the range of $700 million-$1.0 billion. Of these, six are technology-enabled initiatives aimed at either boosting topline or reducing costs. The company has made annual investments close to $500 million annually in these tech initiatives.

XPO Smart is one such suite of tools based on data science and machine learning for improving overall business productivity through demand management, labor optimization, and warehouse management. The company has also launched XPO Connect, a fully automated digital freight marketplace. This is used to connect shippers and carriers and helps differentiate the company in this crowded field of freight brokerage. The company has also come up with XPO Direct, a shared-space distribution solution to allow retailers to share logistic resources optimally.

Investors should consider these risks

The biggest risk for a transportation and logistics company in the current environment is the depth and the length of the ongoing recession. In case the pandemic-triggered recession continues for a longer time frame, it may significantly depress consumer spending. This, in turn, means lowered demand for XPO’s freight and delivery services.

Investors are also concerned about $8.17 billion in debt on the company’s balance sheet. Of these, $2.1 billion is attributable to operating leases. However, we should remember that the earliest the company will require to repay anything is in June 2022. Additionally, the net debt is a much more manageable number, close to $4.9 billion. The company’s net leverage ratio at end of March 2020 was 2.95x, definitely more than desired but not astronomical.

The company reported EBITDA of $1.67 billion in 2019 and of $333 million in the first quarter. The company has grown EBITDA at a CAGR of 37% from 2015 to 2019. The consistent and robust pace of increase in operating profits will act as a margin of safety for investors as the company tackles its debt.

The total liquidity, which includes cash and borrowing capacity, on the company’s balance sheet as on March 31, 2020, was $2.5 billion. Besides, the company is cash-flow positive and generated CFO of $791 million and FCF of $628 million in 2019. Additionally, the company generated FCF even during the first quarter of 2020 and expects to be FCF positive for the rest of 2020. Hence, the chances of the company being unable to repay any of its immediate liabilities remain slim.

What price is right here?

According to finviz, the 12-month consensus target price for the company is $87.94. The company is trading at a PS multiple of 0.44x and forward PE of 22.87x, which is lower than the valuations of competitors such as C.H. Robinson Worldwide (CHRW) and Old Dominion Freight Line (ODFL). C.H. Robinson Worldwide is trading at PS multiple of 0.74x and forward PE multiple of 23.21x. Old Dominion Freight Lines is trading at PS multiple of 5.23x and forward PE multiple of 32.59x.

Considering XPO Logistics’ resilient business model, focus on margin expansion, and technological differentiation, I believe that the consensus target price is not capturing the fair value of the company. A target price of $92, as set by SunTrust analyst Stephanie Benjamin on July 17, seems to be a fairly achievable target price for the company in the next 12 months. On July 8, Citi analyst Christian Wetherbee also raised target price to $92 from $73 and reiterated Buy rating.

The COVID-19 pandemic has definitely added to the uncertainties faced by XPO Logistics in the short run. However, the company stands to benefit in the long run and may even emerge stronger from the pandemic. Being a leading e-commerce logistics player, the company will most likely benefit from the trend of outsourcing e-commerce fulfillment in Europe, rising demand for last-mile services for big and bulky goods in the U.S., and for reverse logistics. XPO Logistics will also be a big beneficiary of the increasing demand for logistics automation services. Finally, the company’s solid focus on cost optimization may result in a much leaner XPO in post-pandemic times.

In this backdrop, I believe that retail investors with above-average risk appetite and investment horizon of a year can consider this stock for their portfolio in July 2020.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.