Daniel Chetroni/iStock Editorial via Getty Images

Followers of my Seeking Alpha coverage on Vicor (NASDAQ:VICR) know that, although I was impressed with the company’s technology and product offerings (specifically, with Nvidia’s (NVDA) selection of Vicor components on its 48V A100 Tensor Core GPU accelerator card), my initial impression in September of 2020 was that the company’s stock was significantly overvalued. As a result, I suffered the slings & arrows of the Vicor bulls as the stock continued to move higher (and even more highly valued…). Then, the company delivered a very strong Q2 report last year and I capitulated, threw in the towel, and upgraded the company to a BUY (See Vicor: Strong Margin Expansion Has Made a Believer Out of Me). That was the kiss of death, as it’s been pretty much all downhill ever since (-44%, see graphic below). So why anyone would listen to me now is questionable, but I will take another shot at evaluating Vicor because looking back, my initial take (that the company was significantly overvalued), was pretty much spot on. However, now that the stock has dropped so much, perhaps it is a much better opportunity for investors.

Investment Thesis

In a nutshell, Vicor produces proprietary and efficient modular power delivery components – such as voltage converters, bridges, and current delivery devices – for a variety of fast-growing use cases. These include AI, high-performance computing (“HPC”), and automotive – specifically, EVs.

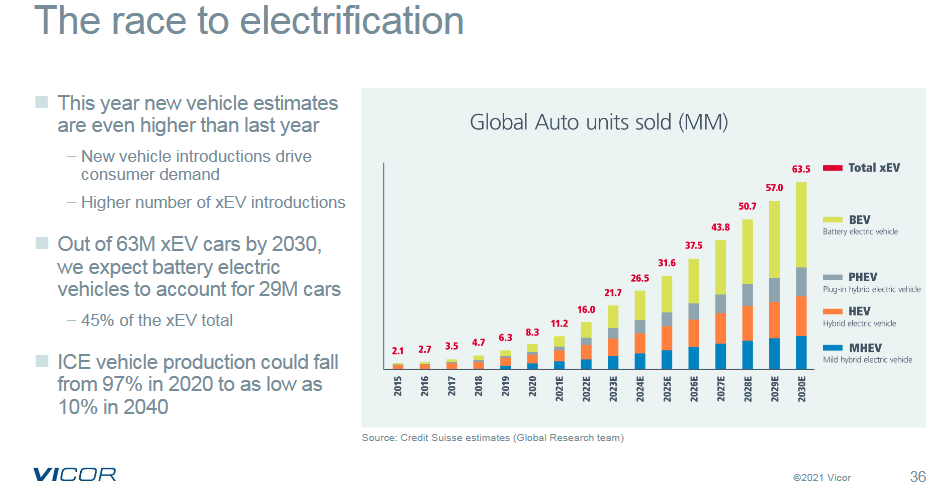

Like most automotive market analysts, Vicor subscribes to the belief that EVs are on the cusp of a significant acceleration in growth:

Vicor

One could argue that the current very high price of gasoline & diesel will only serve to improve EV growth projections as more and more consumers are becoming interested in EVs and the number of available EV options is quickly expanding, including the new Ford F-150 Lightning, of which Ford (F) recently made its first delivery (beating out Tesla’s CyberTruck to the punch).

Vicor believes EVs are a rich platform for its products and estimates the range of potential content is anywhere from $50-$720 on average per vehicle. That, of course, represents a huge market potential – which the company projects to be $29b SAM by 2030.

So, let’s take a closer look at how the company has performed as of late.

Earnings

Vicor released its Q1 EPS report in April, and it was less than stellar. GAAP EPS came in at only $0.11/share and revenue of $88.3 million was actually slightly down yoy. Net income for Q1 was only $5.0 million, just one-third of that earned in Q1 of last year and down from $8.9 million on a sequential basis. Gross margin decreased to 42.6% of revenue in Q1, as compared to 50.3% for Q1 of last year and 45.2% in the preceding quarter (Q4 of FY21).

That is obviously not what investors want to see with a highly-valued and supposedly growth-oriented tech stock. Shareholders felt the impact immediately following the report, as the stock dropped from ~$77 to $62, and it hasn’t recovered much since.

Dr. Patrizio Vinciarelli, Vicor CEO, gave the following explanation for the poor results:

For three consecutive quarters, component shortages and capacity constraints have caused revenues to fall short of expectations with increasing costs and manufacturing inefficiencies impacting margins.

Yet, it’s hard to know exactly what the problem is here: was VICR’s logistics really that bad, or did suppliers simply prioritize other customers? Regardless, it appears that VICR did not have enough supply inventory to build end-product.

In addition, and as explained on the Q1 conference call, margins took a hit from a variety of headwinds, including: costs associated with outsourced panel production, higher freight costs, higher expenses related to tariffs, and increased staffing to support the startup of the company’s capacity expansion plans (i.e., the new ChiP fab, which opened May 17th).

Basically, it seemed as though everything that could go wrong did go wrong. But this far into the pandemic, investors are likely asking a simple question: Why? I mean, I remember writing over a year ago about how the company was going to expand manufacturing capacity and that that would enable the company to ride on a rocket-ship of growth. It never happened … and we are hearing it again:

The Q1 book-to-bill ratio came in well above 1, with one-year backlog increasing nearly 23% from the prior quarter. Substantial progress on production rates and margins awaits capacity expansion which is nearing completion for initial operations to start in Q3.

However, once again, it is not clear to me if production rates and margin will increase unless VICR secures the parts it requires to build end product.

Going Forward

CEO Vinciarelli was asked about logistics and securing adequate supply on the Q1 conference call referenced earlier. In my opinion, his reply was less than comforting and seems to give the company a “way out”. Since this is obviously such a key issue for VICR going forward, I want to post Vinciarelli’s entire response:

Well, I think as we’ve discussed in the past, with respect to the availability of all our proprietary semi-conductors and waiver outs, we’ve made strides in that front, both with respect to getting the output and also securing a long-term sourcing at rise that are expected to support the requirements. With respect to getting variety parts that it being from time-to-time unavailable because of general supply train issues, we’re very focused on that, I think I’m beginning to see, and I don’t want to be too definitive with respect to this because it’s still relatively preliminary, I’m beginning to see some easing and some increase availability coming online later this year. Obviously we’re watching that very carefully with respect to making sure that once we have all of the process steps integrated and we have our fab capacity in place, that component availability is not going to get in the way of being able to use.

Risks

Vicor is obviously not immune to the macro-environment risks associated with the global pandemic (primarily China’s “Zero Covid” policy) on supply chains, high inflation, a higher interest rate environment, and the impact of Putin’s horrific war-on-Ukraine, which has effectively broken the global energy and food supply-chains. Any of these factors could cause a slower global economy and/or a recession.

The global EV market, which VICR is focusing on for growth, could be negatively impacted by a lithium (i.e., battery) supply shortage.

In March, Seeking Alpha reported that a 17.6% plunge in Vicor’s stock was due to a report by CJS Securities analyst Jonathan Tanwanteng indicating that Nvidia’s new AI chip (the NVDA H100 AI Processor) might exclude Vicor’s components. Nvidia has been a large customer for Vicor, and since VICR components are proprietary and sole-sourced, investors need to be concerned that customers like Nvidia may feel they cannot hitch their wagon to a horse that can’t deliver the volume required. See this “cut-out” short report on the subject.

Upside risks include the potential announcement of a significant tier-1 EV manufacturer supply contract. However, once again we come up with the question: would VICR be able to supply parts in volume and, therefore, would a tier-1 EV maker take the risks of it not being able to do so (likely requiring printed circuit board redesign(s) and addition certification testing).

From a valuation perspective, VICR’s is still very rich in my opinion, and the valuation level is simply not supported by the company’s demonstrated performance (or lack thereof): the TTM PE = 66x and the forward P/E = 100x. Indeed, the valuation metrics Seeking Alpha tracks suggest Vicor is at high-risk of performing badly: with an overall valuation risk grade of D-. Note, VICR’s valuation report card also has quite a few Fs, including for its TTM price/sales of a whopping 8x:

Seeking Alpha

Summary & Conclusion

Like it has been since I first met the company, Vicor seems to always be waiting for the next quarter in order to meet shareholders’ expectations for strong growth. With the possible exception of Q2 last year, the company’s quarterly reports have been mostly big disappointments. The potential of losing big customer Nvidia is a real danger in my opinion. It’s not clear where the growth will be coming from, despite what appears to be an impressive backlog (an estimated ~$425 million). That said, Vicor seems to have always had an impressive backlog for quite some time.

Bottom line: Vicor certainly has potential, but in my opinion, the company has not demonstrated the growth necessary to support its valuation level – even after the big drop in the stock price. I am going to whipsaw my followers and change my rating from BUY to SELL. And for those of you who think I am a good contrary indicator on the stock given my track record, you’ll probably be buying next week. But I won’t be. That’s because I think there is a good chance that Nvidia bails on Vicor.

I’ll end with a 5-year price chart of Vicor’s stock: