The seasonally adjusted S&P Global US Manufacturing

Purchasing Managers’ Index™ (PMI™) posted 51.5 in August,

down from 52.2 in July to the lowest since July 2020.

We look beyond the survey’s headline index to provide more color

on the health of US manufacturing, with is undergoing a period of

falling demand, inflation and ongoing supply constraints, which are

driving output lower and leading to a greater reluctance to invest

in machinery and labor.

More positively, supply chain delays moderated in August, and

price pressures fell to the lowest for one and a half years.

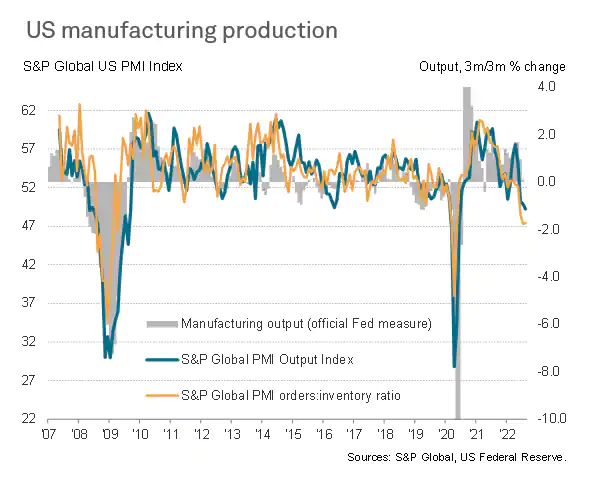

Output down for second straight month

The PMI survey’s Output Index showed US factory production

having dropped for a second month running in August, with the New

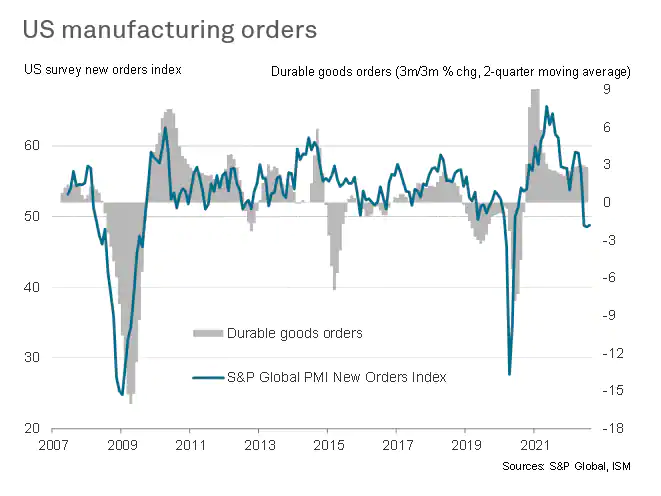

Orders Index meanwhile indicating that demand for goods has now

fallen for three straight months.

Barring the initial pandemic lockdown months, this is the

steepest downturn in US manufacturing signalled by the PMI since

the global financial crisis in 2009. Forward-looking indicators

such as the orders-inventory ratio suggest that the downturn has

further to run.

Companies blamed a variety of factors for the deterioration in

demand, including the ongoing impact of soaring inflation, supply

constraints, rising interest rates and growing uncertainty about

the economic outlook.

Reluctance to invest and expand

Worryingly, the sharpest drop in demand was recorded for

business equipment and machinery, which points to falling

investment spending and heightened risk aversion. At 44.7, the New

Orders Index for producers of investment goods such as plant and

machinery was the lowest since comparable data were first available

in late-2009, excluding the first pandemic lockdown months of

early-2020.

Similarly, payroll growth slowed close to stalling, reflecting a

growing reticence to expand workforce numbers in the face of the

deteriorating demand environment. August’s Employment Index was the

second-lowest for just over two years and, at 51.1, well below the

average of 53.0 seen so far during the recovery.

Supply delays moderate

Falling demand for raw materials has, however, taken pressure

off supply chains and helped shift some of the pricing power away

from sellers towards buyers.

Although vendor performance deteriorated again in August as

transportation and logistics issues remained evident, the

lengthening of average supplier lead times was the smallest since

October 2020.

With supply constraints having acted as a major cause of higher

prices during the pandemic, this easing of supply delays has led to

a commensurate cooling of price pressures. Average input costs paid

by producers rose in August at the slowest rate since January 2021,

reflecting this partial shift in pricing power away from sellers

towards buyers.

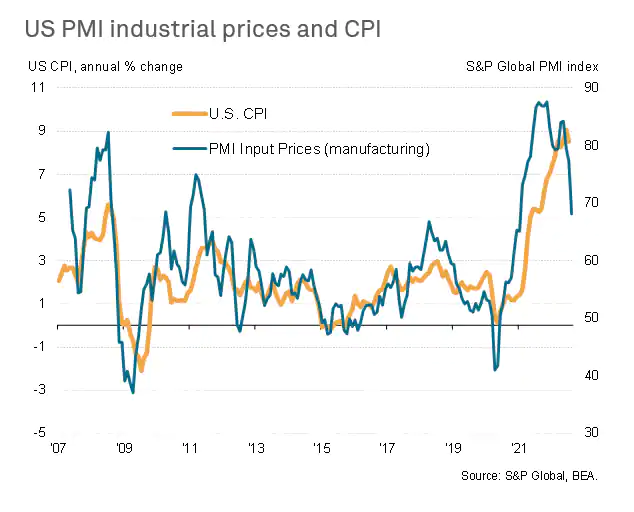

Inflationary pressures ease

Although still elevated by historical standards, the survey’s

inflation gauges measuring both input costs and selling prices are

now at their lowest for one and a half years, which should help to

bring consumer price inflation down in the coming months.

The manufacturing PMI’s Input Cost Index, for example, exhibits

an 86% correlation with the annual change of consumer prices in the

US, with the PMI acting with a lead of two months.

Clearly, the inflation outlook will also depend on service

sector inflation rates and the volatile energy market in

particular, but the feeding through of lower supply-related cost

pressures in manufacturing undoubtedly bodes well for the inflation

outlook in coming months.

S&P Global US Manufacturing PMI press release

Chris Williamson, Chief Business Economist, S&P

Global Market Intelligence

Tel: +44 207 260 2329

© 2022, IHS Markit Inc. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers’ Index™ (PMI™) data are compiled by IHS Markit for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.