Sharply higher interest rates and capital market volatility will weigh on US non-financial corporate debt issuance through 2022, says Fitch Ratings.

Record issuance in 2020 and 2021 to refinance high-cost obligations and increase liquidity during the pandemic provides many companies with flexibility in issuance timing and some capital allocation discretion.

Fitch’s economic team expects the policy interest rate to increase to 3.5% by 1Q23 from 0.25% at YE 2021. The ICE BofA US High-Yield (HY) Index Option-Adjusted Spread rose to 5.87% at June 30, 2022 from 3.10% at Dec. 31, 2021, according to the Federal Reserve. Coupons for the ‘A’ and ‘BBB’ rating categories averaged 4.4% and 4.6% in 2Q22, respectively, up from 2.5% and 2.5% in 4Q21.

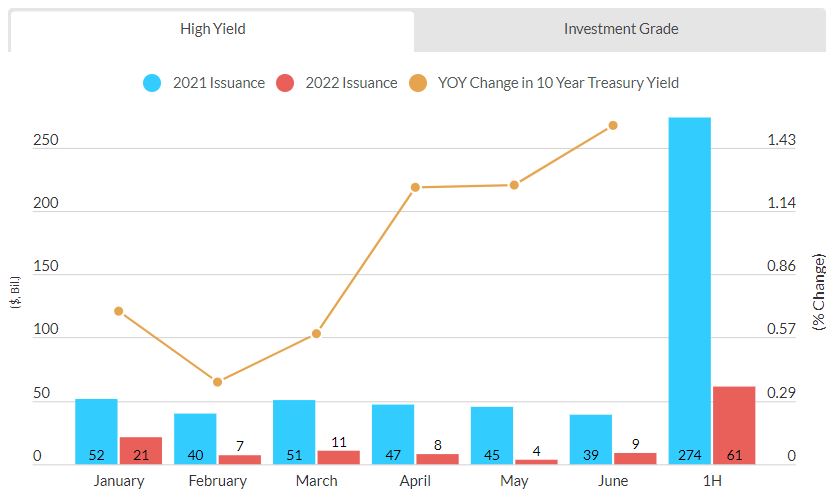

HY and investment-grade corporate debt volume declined significantly in 1H22 compared with 1H21. HY bond issuance fell 78% to $61 billion in 1H22, compared with 1H21, and is down 49% from the $119 billion issued in 1H19. July 2022 HY issuance is exceptionally weak with just two deals pricing for $1.1 billion, while 2022 volume is on pace to be the lowest since 2008. YTD mutual fund outflows of $34 billion underscore investor pullback in demand.

Investment-grade issuance fell 26% to $292 billion during 1H22. The decline was down only 14% through April compared with last year, but accelerated in May and June with issuance falling 60% and 44%, respectively, as rates continued to rise. Investment-grade issuance may be normalizing near 2019’s $617 billion after $1 trillion was issued in 2020.

Investment-grade issuance fell 26% to $292 billion during 1H22. The decline was down only 14% through April compared with last year, but accelerated in May and June with issuance falling 60% and 44%, respectively, as rates continued to rise. Investment-grade issuance may be normalizing near 2019’s $617 billion after $1 trillion was issued in 2020.

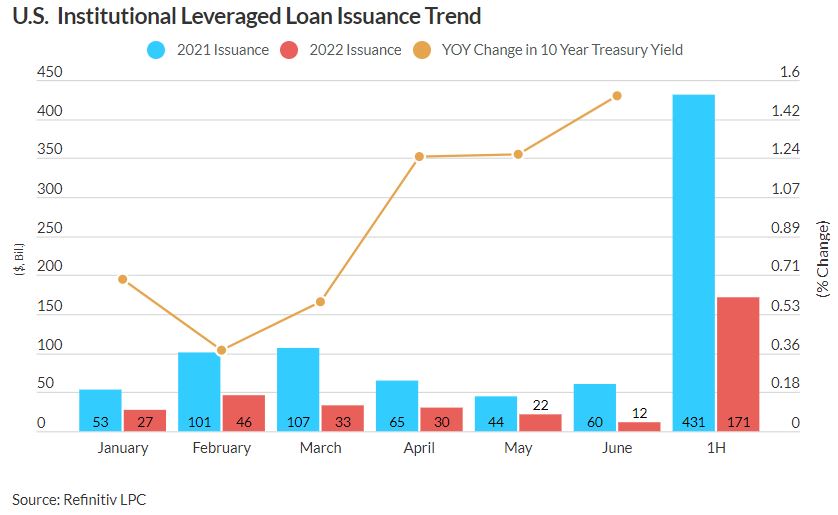

US institutional leveraged loan (LL) issuance is also down, falling 60% through 1H22 due to fewer refinancings and repricing transactions. LL issuance during June was the lowest since May 2020, at $12 billion, and was 79% below the comparable prior-year period.

Bond maturities are expected to be low through the rest of 2022, with $95 billion of investment-grade obligations, $13 billion of HY and $15 billion of LL outstanding left to mature as of June 30. Investment-grade maturities will increase to $258 billion in 2023 and $294 billion in 2024, which could support additional issuance in the investment-grade market over the near-to-intermediate term. However, HY maturities will remain low in 2023 and 2024 at $41 billion and $60 billion, respectively, before jumping to $145 billion in 2025. LL maturities also remain relatively low until 2025 at $47 billion and $144 billion in 2023 and 2024.

The last major US corporate debt issuance slowdown occurred during the 2007-2008 financial crisis. HY and LL issuance volume in 2008 was a paltry $48 billion and $70 billion, respectively, down 63% and 83% from 2007.

Source: Fitch Ratings