Source: Reader’s Digest

Amidst uncertain economic conditions, investors are increasingly drawn to consumer defense investments due to their stable industries, economic versatility, and attractive investment characteristics. An examination of the consumer goods segment reveals an often-overlooked industry stalwart, United Natural Foods Inc. (UNFI). UNFI offers a fantastic recession-resistant investment opportunity with an encouraging long-term outlook. This article will provide an in-depth examination of UNFI, substantiating my bullish investment thesis on the stock as well as discussing financials, valuation, and growth characteristics.

Business Advantages

With annual revenues exceeding $27 billion, UNFI is one of the largest North American and Canadian food wholesalers distributing more than 275,000 products to over 30,000 customer locations distributed across two continents. It displays distinct business advantages, including tremendous scale, operational efficiency, and substantial revenue diversification.

The company is the leading distributor of natural, organic, specialty, produce, conventional grocery, and retailer services with 55 food distribution centers all located within 85% of the US/Canadian population. UNFI’s close proximity to its customers drives significant cost advantages, as product transportation expenses (the costliest aspect of the food delivery business) are minimized, helping streamline operations and drive bottom line revenue growth. This provides UNFI with a competitive pricing advantage, as the company is able to deliver wholesale food items more quickly and at a better price than competitors. The food business is an extremely cut-throat industry, with strained profit margins historically in the low single digits. However, large operational scale enables UNFI to drive cost efficiencies through large material purchasing, an efficient freight and logistics apparatus, and bargaining power with major food retailers. It can deliver wholesale food items to customers faster and at more competitive pricing.

UNFI’s revenues are highly resistant to erosion or disruption. The company derives revenues from a vast array of customers across both wholesale and retail operating segments, helping to mitigate negative effects associated with losing any single customer. UNFI has been the primary distributor to Whole Foods Markets for more than 20 years and has developed entrenched competition-resistant relationships with quite a number of widely recognized food retailers ranging from Whole Foods (AMZN), Kroger (KR), Sprouts (SFM), Wegmans, Harris Teeter, Cash and Carry Stores, The Fresh Market, Coborn’s, Natural Grocers, and Jerry’s Foods, among others. UNFI only has one main competitor, SpartanNash (SPTN); other preeminent food distribution companies Sysco (SYY) and US Foods (USFD) service a different demographic targeting restaurants, schools, businesses, hospitals, etc., whereas UNFI focuses on supermarkets and food retailers in both the wholesale and retail operating segments.

UNFI’s focus on retail and food wholesale segments makes revenues highly stable, as the company’s customer base routinely engages in grocery purchasing. It is distributing a product that is a basic necessity subject to inelastic demand; regardless of economic vagaries, war, etc., everyone needs to buy groceries and eat. Even amidst lockdowns and a national pandemic, UNFI demonstrated strong performance in 2020. It reported sales growth across all channels; chains sales increased 21% to $10.7 billion, independent retailers’ sales increased 21% to $6.7 billion, supernatural sales increased 7.4% to $4.7 billion, and retail sales increased 41.0% to $1.7 million. The company has witnessed consistent revenue expansion for more than 20 years, experiencing high mid-single digit growth for many years. Its underlying food business is highly recession-resistant with stable revenue prospects over the long term.

Source: Quarterly Earnings Excerpt

Growth Vectors

UNFI benefits from a number of beneficial market developments and positive growth externalities. Fundamentally, the company supplies an essential food resource subject to steadily increasing demand. As populations grow, food needs increase, elevating inventory turnover, sales, and UNFI’s revenues; it is a self-reinforcing feedback loop.

As a result of the coronavirus pandemic, individuals still remain hesitant to go outside, attend gatherings, go into work, or go out to restaurants and other food service establishments. Money traditionally spent in restaurants, at schools, near workplaces, at bars, etc. is being redirected toward grocery spending. Some estimates indicate that the restaurant industry has lost upwards of $200 billion as a result of the pandemic. Although devastating to restaurant businesses, the money lost will be redirected toward the retail grocery segment, whether it be Kroger, Walmart (WMT), etc. For the foreseeable future into 2021, this will provide an enduring tailwind to retail groceries and food wholesalers, helping to bolster top line revenues. During the company’s first quarter fiscal 2021 results, management reiterated its net sales outlook for fiscal 2021. Management continues to anticipate fiscal 2021 net sales in the range of $27-27.8 billion. This implies 3.3% growth over fiscal 2020 at midpoint. Further, United Natural reaffirmed adjusted EBITDA projection of $690-730 million, which indicates a 5.5% rise over fiscal 2020 at midpoint.

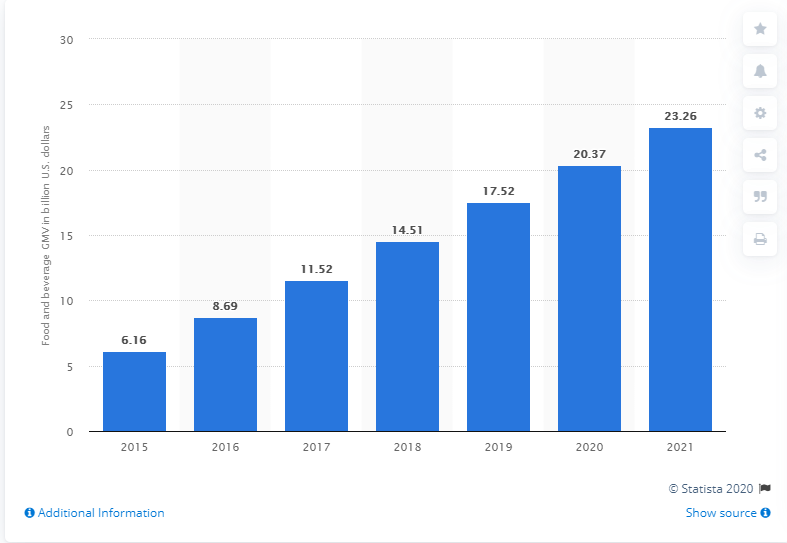

After Amazon purchased Whole Foods, UNFI has witnessed a material increase in sales across its omnichannel platform, primarily because Amazon has integrated more categories and more SKUs into its food offerings and also aggressively expanded the company’s food offerings. As Amazon continues to ramp up its Amazon Fresh, food products, and service offerings, UNFI will be a large beneficiary for many years to come. As it stands today, UNFI is an integral part of the Amazon foodservice business – it oversees the logistics of food distribution all across the United States and for all Whole Foods locations. UNFI has a 5-year contract with Whole Foods to handle the retailer’s food distribution set to expire in 2025. However, in all likelihood, UNFI’s entrenched relationship with Whole Foods as well as Amazon will continue long into the foreseeable future. Strategically it wouldn’t make financial sense for Amazon to invest tens of billions of dollars to set up another 40+ distribution facilities especially for food items and acquire fleets of delivery vehicles, all in order to generate a low-single digit return on investment. Amazon’s online grocery sales are increasing at a rapid rate with a CAGR of 9%, with 2021 grocery sales expected to reach $23 billion. UNFI will benefit from enduring tailwinds originating from the Amazon and Whole Foods operating segments long into the future.

Source: Statista

Financial and Valuation Assessment

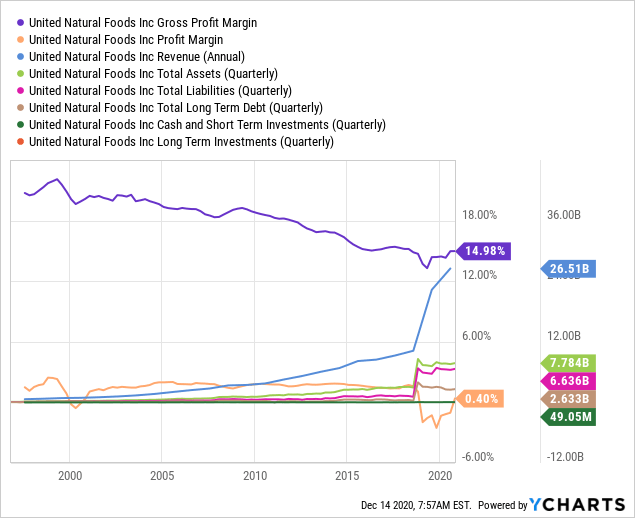

An examination of UNFI’s financials reveals very strong performance on the company’s income statement, steady revenue expansion, net sales up nearly 20% from last year alone, and that revenues have increased for 20 years. The company has maintained steady margins – the food business is very price-competitive, so single-digit profit margins are not uncommon; net margins have remained in the low single digits historically, aside from 2019-2020 amidst the coronavirus pandemic. UNFI does exhibit some vulnerabilities in its balance sheet – the company has a debt load of $2.6 billion and a moderate debt-to-equity ratio of 2:1, and debt is covered by operating cash flow at roughly 20% coverage; however, UNFI does lack substantial liquidity reserves, displaying just $49 million in available liquidity. From a valuation standpoint, UNFI is undervalued by any means of analysis: P/E, PEG, PB, or discounted cash flow; the stock is trading at a P/E ratio of 6.7x earnings and is drastically undervalued. Based on a discounted cash flow analysis, the current share price of $15.58 is way below the future cash flow value of $86.01, implying that the stock is undervalued by 82%.

Data by YCharts

Data by YCharts

Final Determination

UNFI appears to be a fantastic investment opportunity – the stock displays great recession resistance, tremendous value, and a steady growth trajectory. UNFI is being severely mispriced by the market; it’s a stock that very few investors have on their radar. The current stock price of $15.58 a share offers a great entry or addition price point.

Disclosure: I am/we are long UNFI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.