My dad recently emailed with me a few times and back forth about investing, and in that context, he had asked me for my thoughts on AT&T (T), since he had recently sold one holding and was looking for an income replacement. The company’s famous dividend is currently yielding around 7%; I am personally long AT&T and consider it a reasonable income investment, but I suggested to my dad that for a very similar yield he consider the Triton International (TRTN, TRTN.PA, TRTN.PB, TRTN.PC, TRTN.PD) preferred shares. He opted for AT&T instead on his financial advisor’s recommendation, and I think he’ll get the equivalent income either way, or maybe more with AT&T if it continues to grow its dividend, but to me it represents an opportunity again to look in at Triton International, which is the world’s largest lessor of container boxes to shipping lines.

(Image Source: Freightwaves)

Triton’s Role in the Shipping World

As an investor in Triton International, I have tried to keep abreast of news related to trends for container shipping, and have followed with interest some stories in the Wall Street Journal in the last few weeks. The first one was highlighting how busy the port of Los Angeles and Long Beach were, while the second was pointing out the longer-term trends of more inbound freight (and I assume outbound as well) happening on the east coast of the United States, with some key ports having been upgraded to handle larger vessels.

It seems like an overall bull signal to see this sort of freight activity, implying that carriers may need to either roll over leases on the containers they get from Triton, either at spot rates or for longer-term signups. Management reported after the close of Q2 that July leasing demand had been strong, but the quarter had ended with a utilization rate at 94.8%. Then, in a press release related to refinancing some debt since the close of the second quarter, utilization was quoted at 96.1% in mid-August, but then mid-quarter updated guidance came out a week ago, and that utilization rate was now up to 97.1% as of mid-September.

Income, Growth, or Both

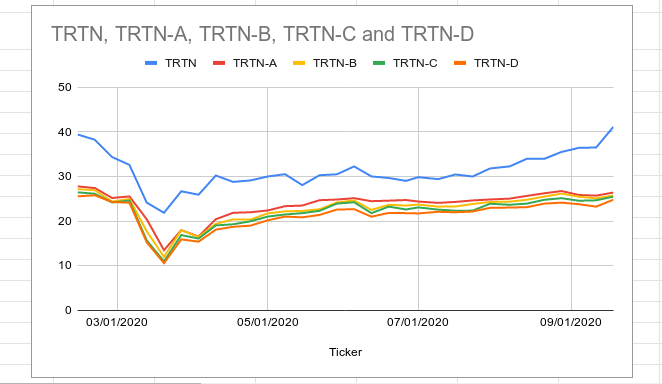

Triton offers retail investors multiple ways to own equity, with 4 series of preferred shares (labeled A through D), in addition to the common shares. In June, I switched from bullish to neutral on the preferred shares, which are primarily an income vehicle unless you were lucky enough to purchase during the massive sell-off this spring, and they had basically come back to reasonable value near their par redemption value of $25.00, with the exception of the “D” shares that took until recently to return close to par value. The common shares still had some legs since June, and also just recently came back to the $40 level, where there were before the pandemic.

(Image Source: Author’s spreadsheet; data sourced from Google Finance)

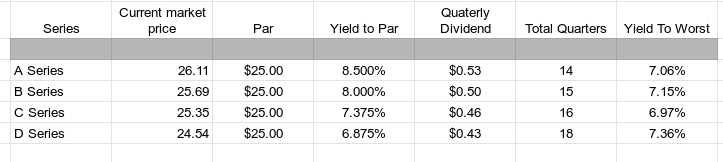

What sort of income is on the line with Triton? The preferred shares all work the same way – a preset quarterly dividend paid out for at least 20 quarters (5 years) from the date of issue, that can be redeemed for $25 at that point but may not be called before then, and cannot be converted into common shares. Before the dividends on the preferred series could be suspended, Triton would first have to suspend the common dividend. While all 4 have different nominal yields to par, they have all settled in around 7% yield to worst, assuming all issues are redeemed at the earliest date allowed.

(Image Source: Author’s spreadsheet; data sourced from Google Finance as of mid-day trading on Tuesday 9/22/20)

Receiving a 7% return for the next 14-18 quarters on a more protected position in the capital stack seems like an attractive income opportunity; the downside is likely limited if you are willing to live with the limited upside.

With Triton, you do not necessarily have to choose one or the other, as the common shares themselves pay out a dividend equal to 5.3% even after their return to the $40 range. The first question on common shares might be if they are now overvalued, but on valuation, I don’t think so. For example, Triton’s P/E is only 9.61, and price-to-cash flow is 2.75. Management gave updated guidance on September 15 for Q3 to see adjusted at 20% higher than Q2, with Q4 even higher. The new guidance is pointing to a Q3 EPS around $1.03, which would be a beat on earnings. The numbers are partly helped along by some well-timed share buybacks. According to the updated slides, the company “repurchased 3.8 million shares in 2020 through Sept. 14 at an average price of $28.39.” That is not a bad buy price for 2020, and 3.8 million shares is equal to taking out 5.2% of the share count since December 2019.

I understand concerns that the EPS improvements give a false impression of underlying growth in the business, but I don’t share that concern. The share buybacks are juicing the EPS numbers a little, but the 200 bps improvement in utilization rates since the end of Q2 is remarkable sign of some foundational strength in the business, and I do not believe container shipping over the long term is going to slow down. The European delivery company DHL (DPSTF) puts out a nice update on shipping trends, and while DHL’s September 2020 outlook points to a low order book for new ship construction, I anticipate that is a modest headwind for Triton, as it only needs to match supply and demand for the containers and be able to service its debt, capex and dividends.

The long-term trends do not point to declines in the need to move goods from one geographic region to another, but rather, growing demand. The growth in maritime transport over the next decade is impossible to predict with great accuracy, and varies by region and type of load (i.e., coal transport may fall but other dry goods increase). The International Transport Forum (a sort of think tank within the Organisation for Economic Co-operation and Development [OECD]) has detailed research pointing to a range of outcomes by sectors. In container shipping, they really just quote the Norwegian / German insurance and advisory company DNV GL Group’s 2017 report that suggests container shipping growth to average 3.2% (on the basis of tonne-miles) to the year 2030 (see page 22 specifically in the ITF report; the original DNV GL Group report they are quoting from can be downloaded here). Richard Scott, writing last year for Hellenic Shipping News Worldwide, is less bullish on growth, seeing a baseline case closer to 2%, and his arguments merit a listen. Regardless, there is plenty of reason to expect steady, if unspectacular, growth in container shipping, and Triton sits at one of the key fulcrum points.

Debt and cash management

The next question might be on how highly leveraged Triton is, which has been a common thread in comments on my previous articles as a reason to steer clear. The company has been chipping away at debt to keep the balance street improving, with long-term debt down to $6.55 billion as of the end of Q2, down from $6.93 billion from the prior year, and that reduction is all the more impressive coming under some tough circumstances, with tariffs, COVID-19 and recession. As mentioned earlier, some debt has been refinanced in August, including $2.3 billion in ABS (asset-backed securities) that have an “A” rating with the S&P. That represents about 35% of Triton’s existing debt getting refinanced, some as low as 2.1% coupon and up to 3.7%, and altogether, should save the company $25 million in interest annually.

If debt went down, what about cash? Over the same period, cash on hand went up from $46 million to over $250 million. Plenty of firms were raising cash through additional debt, but Triton has improved its cash through smart operations, while also reducing debt and now reducing interest expenses as well. Triton was planning to reduce CapEx coming into 2020, and even with the increased dividends due to the series of preferred shares, it is a net positive to the company’s cash flow.

The combined dividends in a quarter amount to $46 million. On a share count most recently reported at 69.5 million common shares, this works out to $36.14 million for common dividends, and just under $10 million per quarter for all the preferred together. That total is up from a year ago, when dividends ran $40.4 million, but the extra cash to dividends is clearly more than offset by the interest savings. The redemption of the preferred shares starting in four years will be costly – about 21 million preferred shares at $25 each will run a total of $525 million over 5 quarters starting in March 2024, assuming all are redeemed at earliest call date. With Triton’s ability to borrow at attractive rates improving, I fully anticipate all preferred shares to be called as soon as allowed by combination of cheap debt and cash on hand.

Conclusions

Even after Triton’s strong return from those March lows, I do think this name still has additional room to move higher. Management has shown itself to be prudent and opportunistic so far, and I previously pointed out, has been bringing down the company’s cost of capital. By leasing the containers to shipping lines, the company’s primary risk is that its clients are not able to pay on existing leases, or choose not to renew or sign on for new leases. With container shipping looking steady for the long run, and Triton’s clients being the largest operators in the business, I do not expect a major problem with non-performing accounts. Triton’s utilization rate is back over 97%, and I do not see a prolonged bear case, even with relatively high leverage. Management has worked diligently to address the debt, and all around keep the company poised to deliver value to its shareholders. I like the preferred shares for income and common shares for blended growth and income.

I recently sold my original long position in the common shares (not because my view changed, but to take profit on what was a small position), and I currently remain long the preferred C shares. I remain bullish and may re-enter a long position in either the common shares, the preferred D shares, or both.

Disclosure: I am/we are long TRTN.PC. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I may also initiate a long position in TRTN.PD within 72 hours, and may re-establish a long position TRTN common shares in the near future.