omersukrugoksu/E+ via Getty Images

Disclosure

Within this article, the company Novo Nordisk A/S (NVO) will be mentioned. For the reader, I’d like to disclose that I’m an employee of the company. The nature of my position is an office job that does not concern sales.

Investment Thesis

In your conquest to establish a diversified portfolio, you will often look towards your own country and its immediate neighbors. As such, it is easy to overlook industry-leading companies if they are not part of that filter. In this article, I’ve presented an overview of some of the Scandinavia’s leading companies.

It just happens that the four countries of this region in scope offer companies across multiple different industries, allowing the investor to monitor a multitude of opportunities should the right price present itself. I hope the information herein will prove to be useful. You shouldn’t miss out on great investment opportunities just because you aren’t familiar with this part of the market.

Introduction

During the spring of 2021 I published an article here on Seeking Alpha titled “The Scandinavian Shopping List” without realizing there could be interest in a follow-up. Given that the market is significantly down YTD, it appears as a timely opportunity to present an updated version for 2022. I’ve also decided to add Finland to the scope, another strong economy in the northern part of Europe, meaning this article covers Denmark, Norway, Sweden & Finland. The debate as to whether Finland is actually part of Scandinavia is something I’ll leave to those who wish to go down the hallways of history, but in this instance, as Scandinavia isn’t a fixed term, I’ve opted for including Finland, albeit in a reduced scope compared to the other countries.

The reason as to why I have an interest in this part of the world is that I’m a Danish native, who for the first many years of my investment journey exclusively invested in Scandinavian/Northern European companies. Today, I hold a diverse portfolio with roughly 70% in North America, 20% in Europe, 8% in Scandinavia, and the rest in developing economy exchange-traded funds (“ETFs”).

There are multiple reasons as to why I hold most of my assets within North America. I’m primarily, but not limited to, a dividend growth investor, and companies within North America have a much more dedicated approach towards consistent dividend hiking. Further, that stock market is much larger, and many industries are dominated by North American companies.

While reading this, you should know that companies within Scandinavia may offer a dividend today, but that it might show unpredictable behavior as companies have a larger likelihood in terms of adjusting the dividend according to the economic cycle and performance of the company. Not all companies do so, but I suggest you look into it should you feel like investing at some point.

Also, there might be withholding tax to consider depending on where you are located. However, this should be made up for by the fact that, despite its size, Scandinavia is home to some of the world’s leading companies within several different sectors. Lastly, if you go with the ADR, always consider the trading volume, as it may be beneficial to go for the local ticker instead, where liquidity is ample.

I believe in holding a diversified portfolio, and despite these countries being small economies with populations equivalent to somewhere between Colorado or North Carolina, they are home to global industry leaders across the board. We all have portfolios where we struggle to find the right company within a given sector, and I believe that as an investor I’m potentially missing out if I limit myself to companies due to where the headquarter is located or where the ticker is traded.

In this article, you will see me discussing opportunities and companies to monitor within Scandinavia. I hope this will serve as inspiration for your own portfolio strategy.

Strength Of Scandinavian Economies

Not everybody will be familiar with the Scandinavian economies, so I believe a few factual pieces of information will serve you well in building an understanding of how mature or developed the economies are.

If you are interested in the historical economic development within Scandinavia, you may browse up on its history via the following source. What you need to know is this. Measured on “ease of doing business” as ranked by The World Bank, Denmark ranks 4th, the U.S. ranks 6th, Norway ranks 9th, Sweden ranks 10th and Finland 20th. These rankings are amongst OECD high income economies. On the Global Innovation Index, Sweden ranks 2nd, the U.S. ranks 3rd, Denmark ranks 6th, Finland 7th and Norway ranks 20th. For the Human Development Index, which also contains education level, Norway ranks 1st, Sweden ranks 7th, Denmark ranks 10th, Finland 11th and the U.S. ranks 17th.

The conclusion is that these small economies offer an attractive environment for its corporations to operate with access to a suitable business environment, an educated workforce and innovative environment. Seemingly all the necessary ingredients for these countries to harbor world-class companies – which they do.

- Norway mainly exports crude oil and gas, fish and metals.

- Denmark mainly exports pharmaceuticals, machinery and medical devices.

- Sweden mainly exports industrial machinery & appliances, vehicles and equipment.

- Finland mainly exports machinery, electrical components, wood & paper products, commodities.

Measured on GDP per capita Norway ranks 6th, the U.S. ranks 7th, Denmark ranks 10th, Sweden ranks 16th and Finland 19th. As such, these countries all harbor wealthy citizens, which creates the foundation for a solid banking sector, which wouldn’t be captured in the exports listed above.

Companies & Selection Criteria

I’ve included a list of selected companies based mainly upon market cap. I’ve tried to keep it at companies with a market cap of $10 billion or more. In a few instances, I’ve deviated from this requirement at my own discretion.

I’ve selected ten companies from each country, Finland being the exception. With the leading indexes containing 20-25 companies per country, I couldn’t include all. I will not cover all the companies, but I’ve selected a number from the following tables, for which I will provide a bit of background and recent movements. In the tables you will see I’ve provided an indication of individual company’s industry ranking. If they are marked as “market leading,” it means that they are leading within their industry (typically) on a global scale. It doesn’t have to translate into a number one spot, but typically will do so. Otherwise, I’ve provided a specific rank indicated via a number. For a few, I’ve designated them “N/A,” as it wasn’t easily applicable to discuss a rank, i.e., in cases of conglomerates.

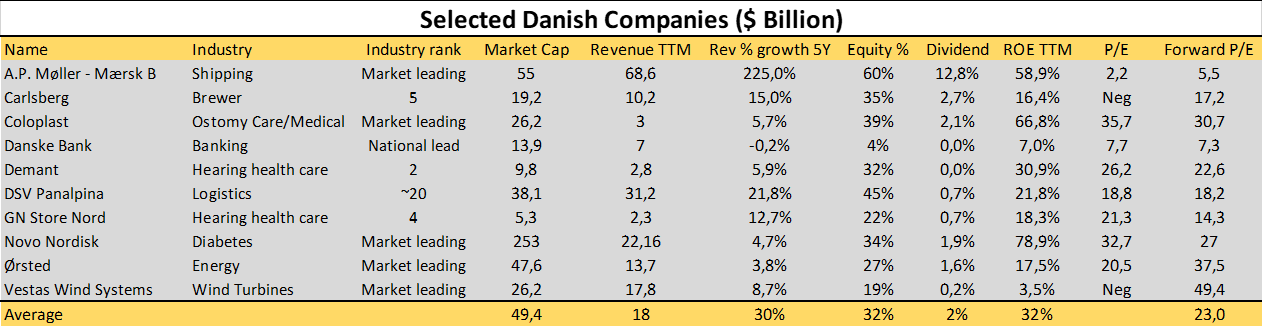

Danish Companies

Seeking Alpha, MarketScreener & Annual reports

The table above allows us to observe that the selected companies consist of a few major companies when measured on revenue, but also a range of significantly smaller ones with a revenue between $2-10 billion. You might be familiar with a few of the larger ones, but most likely not the smaller ones.

- A.P. Møller – Mærsk A/S (OTCPK:AMKBY) is the world’s leading container shipping company. I’ve covered the company several times over the past year, and I’ve been terribly wrong on how the stock turned out to perform during this period. As you can gauge from the table above, Maersk had a blow-out year during FY2021 with a similar year expected for 2022. Unless something changes very soon, 2022 should actually come out even better than 2021, when Maersk secured a net income of $17.9 billion – more than the previous ten years combined. Right now, the consensus expectation is a net income of $24 billion for FY2022 with a net income of $10 billion for 2023. That is also why Maersk is trading at such depressed price earnings ratios, as the current income bonanza is expected to cool. There are vastly different opinions concerning to what extent they will cool, with management suggesting they will begin to experience a cooling environment in second half of 2022. The industry is very competitive to the extent of being considered a commodity where price is the sole parameter. However, the surging income and free cash flow has allowed Maersk to conduct a range of acquisitions strengthening its strategy of becoming a full logistics provider. This has, of course, improved Maersk’s long-term outlook. As a company, it benefits from cyclical periods of increasing GDP and suffers in times of recession and contracted global trade. Most of the world’s goods are transported via sea freight, which is the source of its cyclicality.

- Carlsberg A/S (OTCPK:CABGY) has long struggled with declining revenue and lacking profitability – but has improved significantly in recent years. Hindsight is 20/20, but Carlsberg completed a rather unfortunate acquisition back in 2008, where it acquired Scottish & Newcastle in a 50/50 split with Heineken. Carlsberg paid $15.3 billion. With both Heineken and Carlsberg being behemoths within the industry, they had to split the company for competitive reasons, which meant that Carlsberg ended up with the Baltic/Eastern European division. Soon thereafter, Carlsberg had to conduct major write downs of assets due to declining profit levels as the Russian currency plummeted, while the bloated debt position remained steadfast – remember, assets are made out of butter, and debt out of stone. This acquisition haunted Carlsberg for most of the last decade, with a recent reorganization and cost savings program having been the focus to lift profitability and decrease leverage. Management succeeded, but Carlsberg has most likely lost its chance of ever conquering the industry, as the top 3 companies are massive in size and have leap frogged while Carlsberg fought with a leveraged balance sheet. Making matters worse, Carlsberg’s significant Russian exposure has come back to haunt the company one final time in relation to the ongoing Russian-Ukrainian conflict, leading Carlsberg to write off the assets and also causing the expected income to be negative as of this year.

- Coloplast A/S (OTCPK:CLPBF) is an interesting company. It is market-leading within its medical device niche of providing services to ostomy, urology, continence, and also wound care. Coloplast churns out incredible returns on invested capital and returns on equity consistently above 50% and 55% respectively. Quite impressive, and also the reason why the stock requires such a significant premium despite being down 30% YTD. The company has in recent years struggled with increasing its revenue but has delivered accelerating revenue growth in 2022 with Q1-2022 resulting in 9% revenue growth while Q2-2022 resulted in 16% revenue growth YoY. Combined, first half of 2022 showed a 12% revenue growth. Coloplast reminds me of a company like Visa (V), where it just never seems like it’s possible to acquire it with a P/E below 25-30. High quality, high price, but also a typical medical company, where it’s revenue appears sheltered from economic ups and downs due to the product being something patients rely on in their every day.

- Demant A/S (OTCPK:WILLF) and GN Store Nord A/S (OTCPK:GGNDF) are another couple of interesting companies operating within a niche. They both provide hearing aids and belong to a cluster of four global companies who completely dominate the market. For many years, they were slow growth stories, but have recently experienced reasonable revenue growth as can be observed in the table. The reason is, that both have expanded their portfolios and branched into everyday headsets for both consumers and office use. In the instance of GN Store Nord, they grew their revenue by 20% YoY for FY2021. GN Store Nord has, however, come into a recent headwind due to its acquisition of a specialized gaming company, where GN Store Nord paid a forward a forward P/S ratio of 4 back in October 2021. Today, such an acquisition could probably have been made at a discount, but back then, the world wasn’t aware of how the global economy would develop. Management has received some flak for having completed the acquisition back at that time, at a price of roughly $1.2 billion. One of the reasons the market could be raising its eyebrows is that GN Store Nord delivers an EBITA margin of 17%, while the acquired company delivers one of 13.3%. As is evident in the table, the two companies are quite equal in size, and I’d therefore compare them head-to-head if I were to decide which one to go with. I see the niche as one of interest given that the world is developing in a direction of more elderly people who stand to benefit from hearing aid.

- DSV Panalpina A/S (OTCPK:DSDVF) is an asset light logistics company and also a growth story, not something we often see in such a mature industry as logistics, with DSV traditionally being strongest in land-based logistics. The company tends to grow through acquisitions and has completed five since 2000. The latest took place in 2019 and was the acquisition of Panalpina, hence the name, and stood at $5.5 billion. Prior to that, DSV acquired UTI Worldwide in 2016 for $1.35 billion. Management has proved remarkable at integrating these companies and have delivered on their own targets for synergies and profitability during the two latest acquisitions. In conjunction with their annual report for 2020 released in 2021, management stated that they are once again ready to absorb another target with a focus on absorbing a company within either air- or sea freight – investors are waiting impatiently. DSV carries an A rating from Moody’s, just to illustrate their ability to look towards yet another acquisition. Current CEO, Jens Bjørn Andersen, has been the CEO since 2008 and therefore part of most of these acquisitions while often being highlighted as an extremely skilled leader. As you can most likely imagine, DSV often carries a rich valuation and while the stock is down 32% YoY, it is up 86% in the past three years and 171% in a five-year horizon easily beating the S&P 500. There is no lack in ambition, as they strive towards increasing ROIC from 14.3% to above 20% by 2025. DSV is currently at its lowest P/E multiple in the past ten years and could warrant a deep dive.

- Ørsted A/S (OTCPK:DNNGY) is an old-school oil & gas company turned green in no time and another company I’ve covered several times. By all accounts, wind power will grow massively all the way until 2050, and Ørsted is currently the world-leading company in offshore wind farm development. If you agree with this trend towards green energy, this could be a suitable company to follow. From my own perspective, I find the market extremely fragmented as it is in its infancy, and we might yet have to see who will dominate it. My own assumption is, that while Ørsted will have a place in the market, they will have to share the market with oil majors who are moving in that direction, something I’ve covered in this recent article. Those companies have the offshore capabilities and massive capital to invest. Having traded as high as $75 per share in the beginning of 2021, the stock is currently trading at roughly $37 per share. However, the company is project-based in terms of sales, meaning that revenue and income is volatile, making the P/E ratios tricky to compare over time.

- Vestas Wind Systems A/S (OTCPK:VWDRY) has been a pioneer within windmill construction and is year-on-year the number one or two based on market share. The company had a bumpy period after the financial crisis and had to rely on a joint venture to get their offshore division going. As such, they entered offshore windmill production together with Mitsubishi Heavy Industries (OTCPK:MSBHF) in a 50/50 split. However, having had a number of skilled CEOs since then, the company has recovered its financials. As such, by the end of 2020 they bought out their former partner to regain 100% control of their offshore wind division. I’ve covered the stock several times, having highlighted the uncertainty tied to their ability to secure profits, and as of the most recent quarterly performance the company is now staring at a negative bottom line for FY2022. The company, and also its competitors, are struggling with supply chain and raw material price issues having eaten away at the operating margin to the point where it’s hovering close to 0%. Vestas has delivered stronger profits than its competitors and is, as mentioned, the dominant player in this industry. Given the outlook for the industry over the coming decades, this could be an interesting play in green energy. However, I also believe investors can hedge themselves better by going via ETFs such as First Trust Global Wind Energy ETF (FAN) which is focused on wind energy related companies, or broadening into iShares S&P Global Clean Energy Index ETF (ICLN) focused across wind, sun, etc. Given the company has suffered so badly from being unable to control its cost in a better way, I’m personally not to keen on investing in the company at this time.

- Novo Nordisk A/S (NVO) has the largest market cap in Scandinavia while also belonging to the top five largest market cap companies in Europe, and for good reason. Novo Nordisk is the world’s largest company for diabetes treatment and also leads the market for treatment of obesity. That market, however, is much smaller and only makes up a fraction of the overall business. It is, however, a strategic priority for the company, as the global population is getting ever more obese. Novo Nordisk consistently delivers a ROE at 70% and an ROIC at 60%+. The company has a history of increasing the dividend annually and distributing it via two bi-annual payouts. Its market cap has bloated in recent months as investors seek shelter in companies with very visible free cash flows going many years into the future, but also as expectations are growing for Novo Nordisk’s newer products. Management was able to increase the full year guidance in conjunction with its Q1 performance. Personally, I find the current valuation is a stretch.

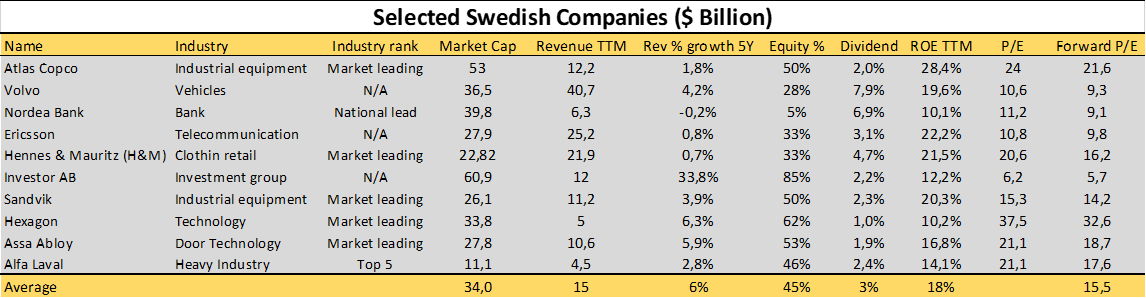

Swedish Companies

Now, I should remind the reader that I’m Danish and, therefore, follow the business media a little bit less for the neighboring countries.

Seeking Alpha, MarketScreener & Annual reports

Where the Danish stock market was focused on green energy, pharmaceuticals, and med tech, the Swedish stock market is strong within different parts of heavy industry. Some of the industrial companies operate within several niches, and it is therefore difficult to determine whether the company as a whole is market leading, but they typically are within one or more of their divisions. Sweden has a proud history of success, especially within engineering, which translates into the companies that will be covered here.

For those comparing the table above to the one roughly one year ago, the difference in company valuations is significant. Forward P/E had an average of 29.3 one year ago, which is now 15.5 for the companies included. Average yield has also climbed from 2% to 3%, while revenue growth seen over a five-year period is substantially lower.

Seen from my perspective, the Swedish stock exchange provides some of the most interesting prospects in Scandinavia. One note, however: the Swedish currency has consistently depreciated against the USD over the last decade, which could hollow one’s investment, albeit slowly.

- Atlas Copco AB (OTCPK:ATLKY) markets its products towards the construction industry and improved its performance from 2020 to 2021. Since having been reshaped as a company in 2017 due to a group split, the company has managed consistent revenue growth. Atlas Copco’s main focus is within compressor technology, where it is the world’s leading provider. The company serves B2B clients within semiconductors, airspace, construction and several other industries. Management recently announced a 5.2% dividend hike which was slightly better than the 5% announced in 2021. Despite also being exposed to the global supply chain issues, the Q1-2022 results showed a strengthening order book, a 16% increase in revenue YoY and a 25% growth in EBT. This company is quality, and that is also evident in the valuation. However, having come down 31% YTD, this company is worth a look for those chasing an industrial company to their portfolio. My two reservations are the exposure to construction given the state of the global economy and the mismatch between P/E and revenue growth, as a P/E above 20 is reserved for companies with strong revenue growth, something Atlas Copco hasn’t managed. However, one look at the orderbook and that might change down the road, as incoming orders have been growing massively in the wake of Covid-19, which also provides favorable comps. Atlas Copco is definitely one of my favorites in Sweden.

- Telefonaktiebolaget LM Ericsson, commonly known as Ericsson (ERIC) would be interesting if you are looking for a way into 5G technology. Revenue has been more or less flat for the last ten years, with restructuring taking place and profit levels only recently recovering. The company has struggled to renew itsel,f but still has a strong, and once again, growing cashflow it can utilize to drive value going forward. One shouldn’t underestimate this giant, which has a strong tradition within R&D. It holds more than 60,000 patents, having invented the Bluetooth technology and being the largest player within 5G. The main shareholder of Ericsson is Investor AB, a company within the list above, which provides a stable ownership structure and long-term strategic focus. Due to the recent turnaround, both profits and revenue has shown improvements within the last couple of years. The question is whether the company will manage to innovate even further and ride the revenue opportunities within 5G. Ericsson operates four segments, with “Networks” being by far the largest, making up roughly 70% of total revenue. This segment grew 4% organically in Q1-2022 while also holding the strongest EBIT margin, therefore allowing Ericsson to grow its emerging bets that currently operate at a loss. Observing Ericsson since Q1-2020 and seeing the gross margin trending upwards from 37.9% to 43.3% as of this quarter, Ericsson is starting to become a much more interesting investment case, as the company used to be surrounded by quite a bit of skepticism.

- H & M Hennes & Mauritz AB (OTCPK:HNNMY) is a fast fashion clothing retailer with a global presence. Between 2010 and 2017, the company managed to double its revenue, though with little bottom-line impact as margins contracted. Going beyond 2017, operating margin has continued to decline, landing at roughly 7% prior to Covid-19. Earnings per share have declined and the company has been behind the curve in terms of transitioning towards an eCommerce strategy. The strategic focus was, until recently, mainly on increasing its physical footprint around the world. They have deployed massive investments into digitalization and supply chain optimization, but questions remain whether that is sufficient to move H&M to the next level. The company has been run by family until just recently ,with a new CEO taking over in 2020 who isn’t part of the family. I applaud that they finally skipped the idea of having family continue to run such a large business, as I personally believe the most recent family CEO failed as a result of having deployed the wrong business strategy. This is also evident in how income eroded from the beginning of the last decade until the onset of Covid-19. The family is still majority shareholder, and I could be fearing they continue to impose poor judgement upon the company and the current CEO, who has been with the company since 1997. I personally believe it would have been better to find an outsider with a strong track record who could stand up to the family when needed. I used to hold H&M shares, but sold them roughly five years ago with a massive loss. So maybe I’m scorned by the past, as I’ve chosen to steer clear of H&M. The Q1-2022 performance showed growing revenue and a return to profitability YoY after having suffered during Covid-19, however, profit levels were not what they used to be. However, with a strong and global brand, the company can of course still correct itself.

- Investor AB (OTCPK:IVSXF) is an investment conglomerate who would be your backdoor to owning a chunk of the Swedish stock market without limiting yourself to a specific company. The Wallenberg Family is majority owner with 23%, and Jacob Wallenberg is chairman of the board. Its major holdings can be found in the annual report on page 3. It is a shareholder in several of the companies listed here, and many others belonging to the largest stock index in Sweden. As per end of 2021, its investments stood at roughly $79 billion compared to $64 the year prior. The company has paid a growing dividend like clockwork, but is the perfect example of how dividends are treated in Scandinavia, as Investor reduced its dividend in the wake of Covid-19 despite having a payout ratio around 20%. However, the dividend is once again growing, and I believe Investor is a very interesting company worth a look, especially due to its proxy-like nature of covering the Swedish corporate landscape.

- Sandvik AB (OTCPK:SDVKF) is the last company highlighted and also the last company trading below the average valuation of the companies selected. Sandvik provides systems and tools within mining, engineering, automotive, offshore, construction and aerospace. Mining makes up 40% of revenue and is its largest division, with aerospace being the smallest at 5%. In this regard, I’d say the company is cyclical, perhaps riding the last waves of this economic upside. However, being invested in mining companies myself, I can see they have held back on investments in renewing their assets in recent years. With the long-term demand going upwards for copper and other metals playing a role in electrical conductivity due to the green transformation, I believe Sandvik may have strong years ahead of it. Sandvik struggled in the wake of Covid-19, but one glimpse at the recent Q1-2022, and we see the company is doing well, with a growing order book across all geographical regions. The company has historically exhibited fluctuating levels of revenue, profits and dividend payouts as it appears to be following the ups- and downs of its major divisional performance in mining.

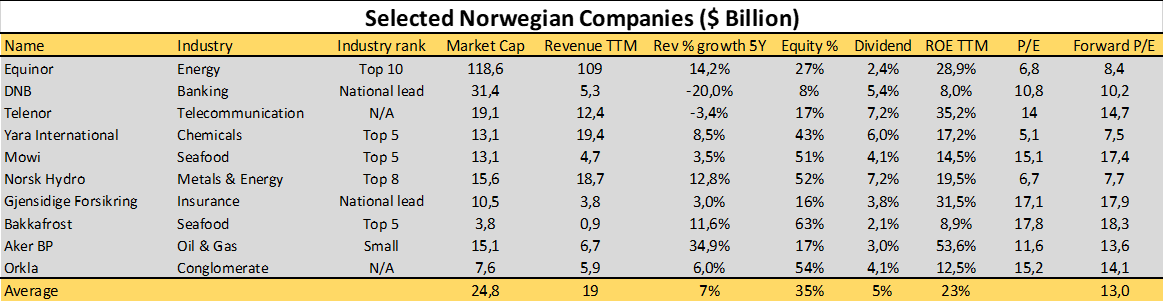

Norwegian Companies

Measured on forward P/E, the Norwegian companies are currently the least expensive of the companies I’ve selected to represent each portion of the individual markets.

Seeking Alpha, MarketScreener & Annual reports

The Norwegian market is again different from the previous two, especially in the sense that it is more focused on offshore and seafood. There are several stocks trading on the Norwegian major stock index that operate within the seafood industry that I didn’t include here. Norway is also a proud shipping nation.

Similarly to Sweden, the forward looking P/E levels have come down substantially compared to a year ago. This should elevate the possibilities of finding a good investment case amongst some of these companies.

- Equinor ASA (EQNR), formerly known as Statoil, operates within the offshore energy sector. The Norwegian state holds a 67% stake in the company. Equinor stands out from its oil peers due to having an ambitious renewables transformation strategy. Equinor is placing its chips on becoming a leading company within especially offshore wind. The YoY change for Equinor is very visible in terms of a growing revenue and market cap. The company is naturally positively affected by the current bloat in oil prices, but I view Equinor even more as a bet on a greener future energy-wise. However, I hold one bit of skepticism related to the fact that the Norwegian state is the main shareholder. That concern is that it may adversely impact main street investors should the state push through the green transition faster than Equinor’s profitability can keep up in relation to investments – in order words, driving investments at the expense of a satisfactory profitability. This is not an unreasonable concern, as I see it.

- Yara International ASA (OTCPK:YARIY) is a chemical company with its main focus on fertilizers. It was originally part of Norsk Hydro ASA (OTCQX:NHYDY), but was spun off back in 2004. Like Equinor, the majority shareholder is the Norwegian government with more than a third of the shares. Yara has struggles with its profitability since 2016, but that has changed in recent years. ROIC has been trending upwards since 2019, where it stood at 4.1% compared to 12.7% in the most recent quarterly performance. The company is exposed to higher energy prices but has driven improved margins via pushing price increases without impacting its demand. While Yara struggled with maintain a positive free cash flow prior to 2019, it has consistently been positive since then, even though it had declined some in the previous quarters. The stock is flat YoY, but Yara is in a good financial situation.

- Mowi ASA (OTCPK:MHGVY) is a seafood company which specializes in salmon farming. Mowi has been kind enough to provide a handbook which describes the industry in detail. Here you will learn that the vast majority of farmed salmon is produced in offshore basins lying in bays supporting the needed biological conditions, as you cannot farm salmon in more than a few select coastal areas across the planet. For the salmon to thrive, there must be sufficient water flow and a narrow temperature range between 0 degrees Celsius and 20 degrees Celsius. Farming salmon plays into a long-term trend of healthy eating as health authorities recommend eating fatty fish – one of the reasons why I’m fond of this sector, as I’ve historically held several companies within my portfolio, including Mowi, which I’m still invested in. The company has historically offered an aggressive dividend payout, as the majority shareholder, John Frederiksen, also owned Seadrill limited (OTCPK:SDRLF) an offshore drilling company which required financial support. Mowi has gotten a great start to this fiscal year, as Q1-2022 delivered record profits due to strong demand and low supply, resulted in EBIT growing 89% YoY, but that is, of course, an effect that can’t be expected to last. However, shareholders may be in a for a treat later this year as such a performance could drive additional dividends, we shall see.

- Norsk Hydro ASA (OTCQX:NHYDY) is yet another company which the Norwegian state owns roughly 34% of. It is one the world’s largest aluminum producers. It also holds a smaller energy division via hydroelectric power. Management is working on elevating profit levels through a program running through 2025. As was the case for Mowi and Yara, Norsk Hydro benefits from strong sales prices which more than offset input price increases, causing surging profits. There is no doubt the world will still need aluminum tomorrow, but the industry appears fragmented, so I’d conduct a deep dive on the competitive environment to identify the industry winner. Norsk Hydro adds to the depth of the Scandinavian economy as a whole, operating in a niche of its own.

- Aker BP ASA (OTCPK:DETNF) belongs to the family of oil and gas exploration companies. An industry where Norway has very strong traditions and a capable workforce, same for oil and gas service companies. Aker has benefited from rising oil prices and is having a great time from a financial standpoint. In general, Norway has plenty of oil and gas companies also within separate niches such as offshore service companies. However, beware, they rely on the oil majors having a good time within the North Sea where they primarily operate. Similarly, Aker BP is exposed to oil and gas fields in the North Sea. As such, there is a geographical exposure tied to many of these smaller companies

- Orkla ASA (OTCPK:ORKLY) is a conglomerate if you look it up, but only because it owns majority stakes within hydroelectric power production and a paint producing company. Putting those aside, it is a producer of food, confectionaries, snacks and your everyday health care products. Those might not sound like the fastest growing categories of products, which is also why management from time-to-time conducts acquisitions. Orkla doesn’t only market its products locally but also throughout Scandinavia, the Baltics, Eastern Europe, and India. This causes exposure to a region of the world where the immediate economic outlook is uncertain – there will be more of those companies when we look at Finland in a minute. Orkla should be considered a consumer staple and is, therefore, easily comparable to many other major household names across North America. Orkla Is down 26% YoY and could very well deserve a closer look for those seeking to add a type of company that typically provides shelter during uncertain times, as people will still need everyday consumables.

Finnish Companies

This is the latest addition to my list, in comparison to my previous article. Finland comes with a disclaimer, as one of its top five export partners is Russia. This is only natural as they are neighboring countries, but it has resulted in a number of Finnish companies having to absorb substantial losses in the wake of the ongoing crisis, also resulting in changed economic outlooks as they have to change focus. There is no reason to overcomplicate the situation, but the prospective investor should dive into the financial performance to understand the historical and future exposure as well as current impact.

I’ve decided to only add five Finish companies, as my knowledge is a little bit limited. However, there are more interesting Finish companies in the large cap index.

Seeking Alpha, MarketScreener & Annual reports

- Fortum Oyj (OTCPK:FOJCF) is a diversified electricity utility company generating electricity through primarily gas, making up roughly 40% of its energy mix but also operating within hydropower and nuclear power. These make up roughly 20%, while they also have a small segment in coal. During its Q1-2022 presentation, management stated that no additional investments would be made within Russia and that the company is seeking a controlled exit. Here, it’s important to note, its Russian exposure stood for almost 20% of its generated EBITDA. Fortum’s energy mix is well situated to support Europe’s current energy troubles, and especially in terms of renewables holding substantial assets within hydropower and also nuclear. Fortum is currently trading at a discount to its historical P/E, but with a negative cash flow, a need to exit Russia, low solidity, and changes in working capital weighing on its ability to secure profits. I’d await the situation for now. However, in the long-term, Fortum could be an interesting company to track given its energy mix.

- Nokia Oyj (NOK) in many ways resembles Ericsson, as it’s exposed to telecom equipment, infrastructure, and 5G. A company that used to set the trend for mobile phones, while today being an infrastructure play. A viable 5G company, similarly to Ericsson and recently having reinstated its dividend even though it’s at a very low yield. While most of those reading this will be familiar with a company like Cisco (CSCO), Nokia and Ericsson are both larger players within telecom infrastructure, and Nokia appears reinvigorated after having come under new management that brought forward a three-step plan to refocus the company. A few years back, Nokia struggled with both its top- and bottom-line while having secured itself healthy profit margins in a handful of consecutive quarters at this point. It also exhibited top-line growth, though it should be mentioned it has been rather volatile. Nokia was, from my perspective, a company asleep for a very long time, but perhaps those times are behind the company. Nokia is a global player and doesn’t carry the same exposure issues related to Russia as many of its domestic peers.

- Kone Oyj (OTCPK:KNYJF) my absolute favorite Finish company and one of my favorite ones in Scandinavia. Kone builds and services moving walkways and stairways as well as escalators and lifts. If you go to your local shopping mall and notice the manufacturer on either of those, chances are they will be manufactured and serviced by Kone, which is a global leader together with only a couple other companies. Unfortunately, due to its strong market position and the fact that investors love companies with a strong service division, the company is notoriously expensive. The founding family retains more than 60% of the voting rights and 22% of the outstanding shares. The company is down 37% YoY and could be worth a look, as this company holds a very strong market position while riding growing urbanization. Lastly, it generates incredibly strong returns on invested capital.

- Stora Enso Oyj (OTCPK:SEOJF) is included as I early on mentioned that Finland is an exporter of wood, pulp and paper – and this is where Stora Enso comes into play. Ever thought about how McDonald’s (MCD) has been moving to biodegradable paper straws, or how the utensils at your kid’s birthday were swapped from plastic to wooden ones? This is the trend that Stora Enso could ride. While the prime focus is paper, wood, and packaging materials, the aforementioned is in the arsenal of what Stora Enso can provide materials for. The company is primarily exposed to Europe, but also Asia and South America. Stora Enso is an example of another company with exposure to Russia, as some of its wood supply is from Russia. Stora Enso is an interesting play for the future, as packaging materials have to become more sustainable.

- Sampo Oyj (OTCPK:SAXPF) is a leading insurance group. Historically, the company has also held substantial minority positions within Scandinavian banks, most recently Nordea, Scandinavia’s largest bank. However, it recently sold its entire position, generating €1.8 billion in proceeds. The company offers insurance across all of Scandinavia and also the Baltics, counting its customers by the millions. Sampo has historically been a well-run company from a financial standpoint, as it has been governed by a conservative management team and a board that had a keen nose for striking a good deal, when it came to acquisitions or initiating minority positions within, for instance, banking.

My Own Takeaway

I’m only long a few of these companies, but I’m exposed to several via ETF holdings in either my brokerage or pension. There are still a couple of these companies, that I would very much like to add to my portfolio, particularly in Sweden and Finland.

Last year, I concluded that DSV from Denmark, Atlas Copco/Investor from Sweden, and Norsk Hydro/Orkla from Norway were my favorite picks.

This year, I would be very interested in having a closer look at GN Store Nord, which is trading at a significant discount compared to its direct competitor, Demant. Perhaps the market is overreacting? However, given DSV’s relative valuation, that company is also worth a look.

From Sweden, I would go with Investor, which has come down in valuation and has a strategy that I’m personally very much aligned with, while also being the proxy to the Swedish economy – as such being both a proxy and a diversification play at once.

In Norway, Yara International could be worth a look at they have succeeded in generating growth once more, while perhaps looking into some very positive years ahead, being a leading fertilizer company.

Lastly, from Finland, I believe Stora Enso or Kone are very interesting companies. I have to admit I’m always biased in favor of Kone. No matter the angle from which I study the company, it’s just a fortress.

Closing Remarks

I believe in diversification. Being from a small country, I’m almost forced to look outside my region for opportunities to identify industry leaders that I believe to be winners. Flipping that coin around, it also means I may benefit from the best of my local market and the best of the well-known North American stock market.

I believe those who aren’t familiar with the Scandinavian economies and companies potentially are missing out. As such, the reader can find a brief overview of selected companies across Scandinavia and will then have to decide for themselves if any of them are worth a deep dive. Conclusion being, that there are plenty of industry-leading companies to choose from.

Now, I’m very curious to hear your perspective

- Do you hold some of these companies and why?

- What is your perspective on small economies and how does that encourage their companies to go global?

- Is this a diversification play belonging in your portfolio?

- With a number of Scandinavian contributors, are there companies you would like covered in more depth?