July Alcantara/E+ via Getty Images

The Hartford Financial Services Group, Inc. (NYSE: HIG) remains a durable figure in the industry. Thanks to its strong customer base and massive operating capacity. It can sustain its operations with its sound fundamentals amidst inflationary pressures. Likewise, the stock price shows it is an attractive stock with consistent dividends. Its growth prospects are still enticing, given the hype in the property, car, and RV market.

Company Performance

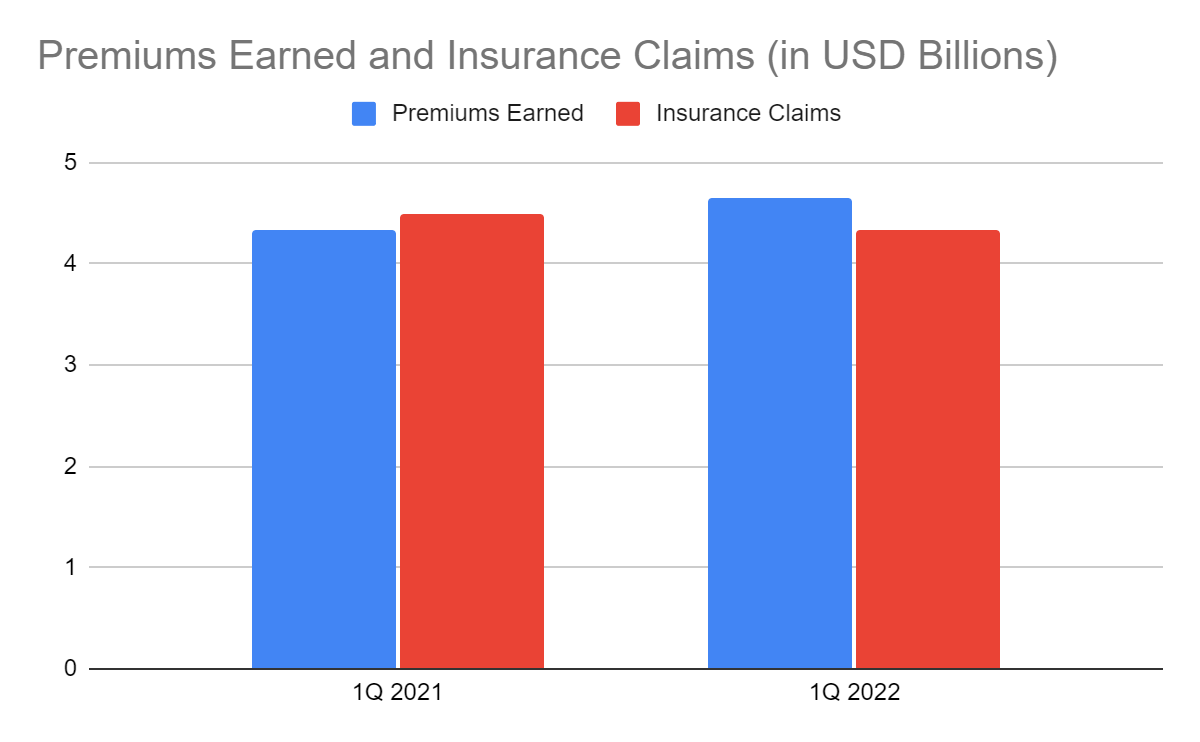

The Hartford Financial Services Group, Inc. continues to operate with ease and prudence. The market landscape is more challenging as inflationary pressures intensify. But, its robust performance remains evident. As one of the largest P/C insurance providers in the US, it covers a vast range of services. It operates through commercial lines that provide compensation for workers and retirees. Meanwhile, personal lines include home and automobile insurance. It is no wonder that it remains unbothered amidst economic and market fluctuations. This year, it appears more promising with premiums of $4.65 billion, a 7% year-over-year growth.

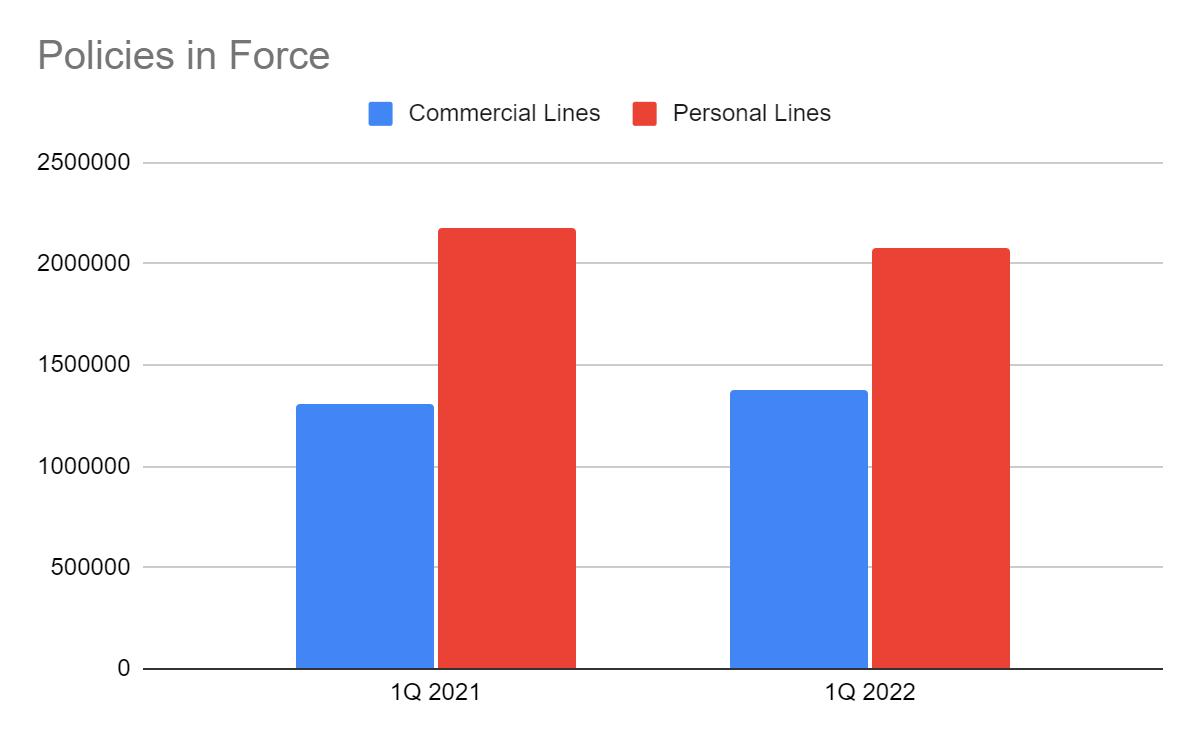

The Hartford benefits from the mix of market demand and strategic pricing. The increase is more evident in its commercial lines with policies in force of 1.37 million. It is a 6% year-over-year growth from 1.30 million in 1Q 2021. Even better, its policy count retention is now 86% versus 84%. This uptrend persists despite the higher price of premium at $186 versus $176 in 1Q 2021. Old premiums also face higher renewal premiums by 2.9% compared to 2.4% in the same quarter. Thanks to its strong customer base, allowing it to adjust its prices.

Meanwhile, personal lines are not as robust as the commercial lines. It has 2.08 million policies in force compared to 2.17 million in the previous year. It may be due to higher prices of home and auto insurance by 9% and 15%, respectively. As such, its policy count retention is 84% down from 85% in 1Q 2021. Thankfully, it also has a solid brand loyalty in this segment. For instance, it handles the home and automobile insurance of AARP members. Note that AARP is considered an influential advocacy group in the US. Its large number of elderly members comprise a substantial portion of voters. As of today, it has 38 million members in the US, US Virgin Islands, and Puerto Rico. The partnership provides The Hartford with a solid revenue stream.

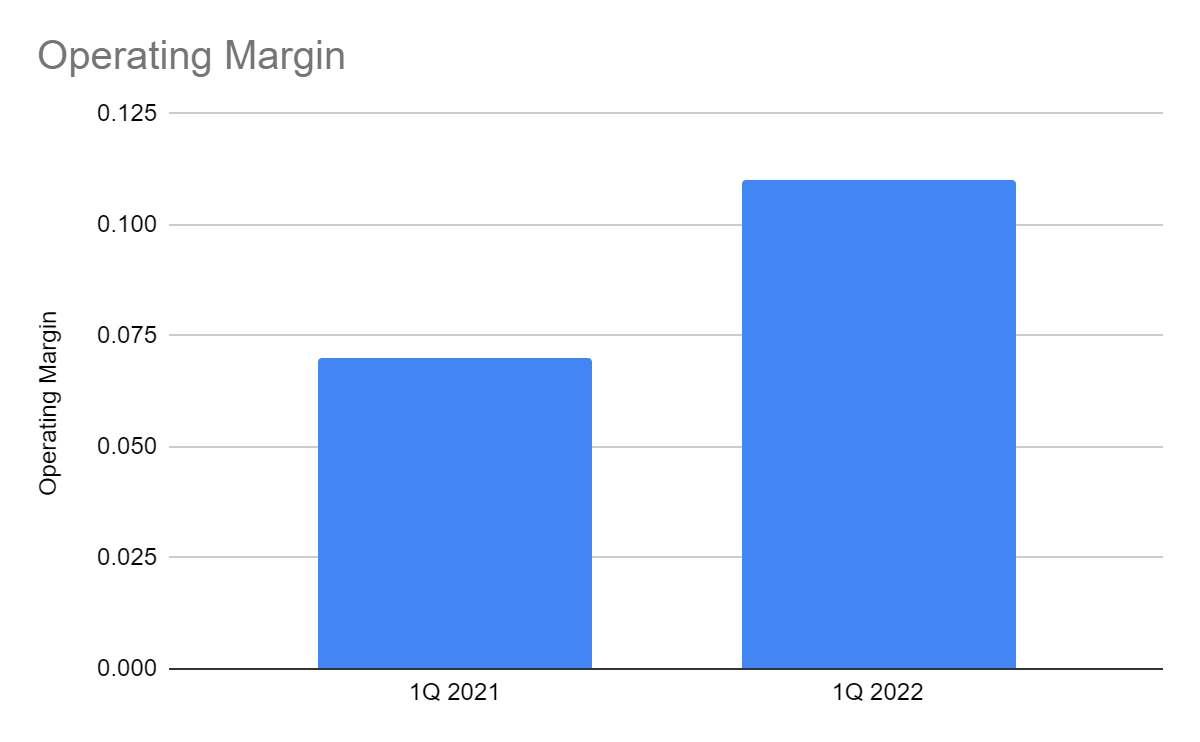

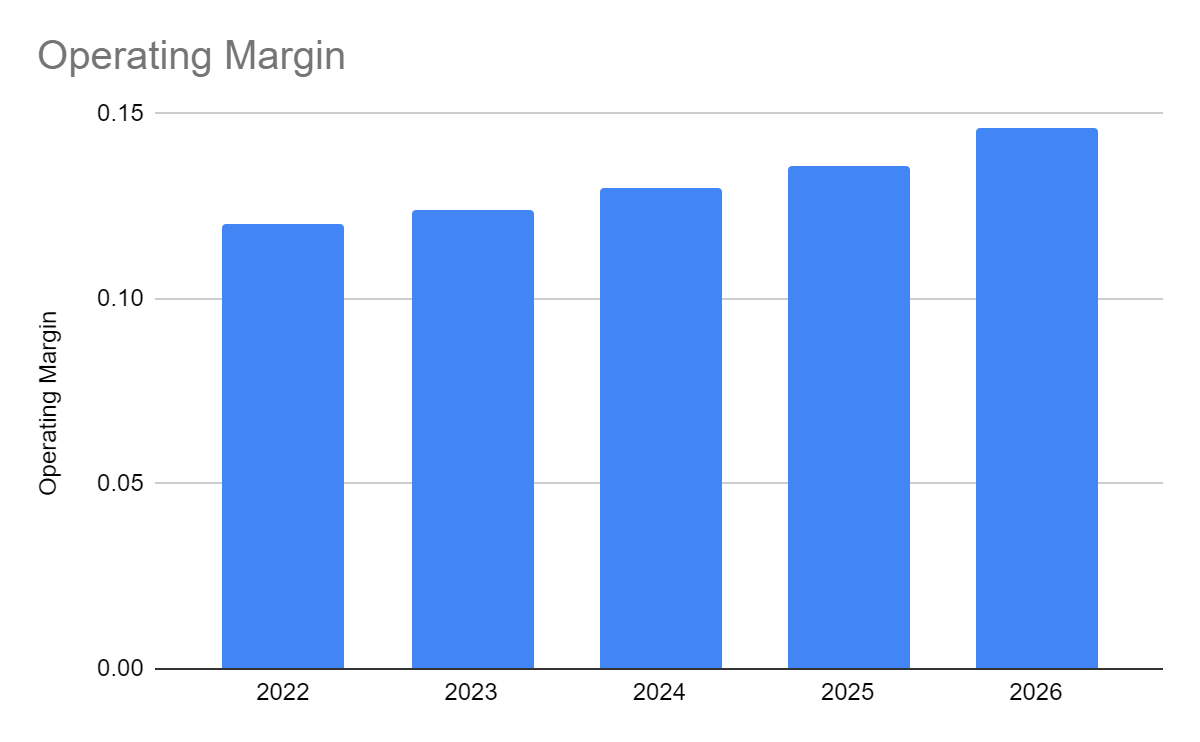

But, its core competency does not rely on its demand and pricing strategy alone. It is prudent and specific with claims policy to prevent potential scams and abuses. That is why its insurance claims remain lower than premiums. Also, it continues to stabilize its core operations while sustaining its capacity. It has efficient asset management, helping it keep its costs and expenses lower. The impressive handling of its resources is also reflected in investment income. It is another segment that stimulates its revenue and margin expansion. Hence, its operating margin is 0.12, higher than in 1Q 2021 at 7%.

Premiums Earned and Insurance Claims (MarketWatch) Policies in Force (HIG First Quarter Report) Operating Margin (MarketWatch)

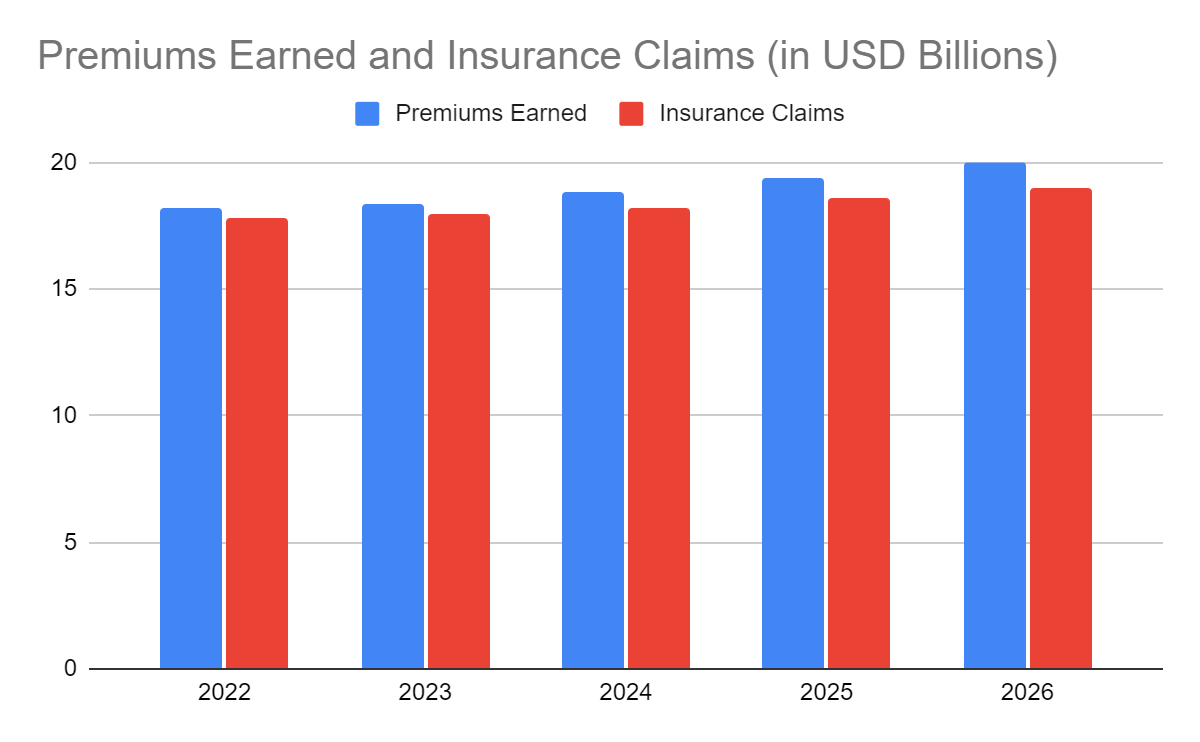

This year, I expect the company to keep its stability. It is good to see its strategic pricing, high demand, and efficiency work together. This core competency is more crucial as the market environment becomes more challenging. Its premiums earned may increase a bit to $18.7 billion with insurance claims of $18 billion. My estimation is within the average premiums and losses in the last four quarters. The 4-5% increase is also near and a bit lower than the average of 5-6% in recent years. I find it a more conservative but reasonable estimation. I consider the increase in prices that may have an offsetting effect in the increase in commercial and decrease in personal lines. Meanwhile, I expect its operating margin to remain at 0.12. Inflationary pressures may drive the operating expenses further in the second half. But in the next few years, premiums may speed up to $18.4-20 billion with claims of $18-19 billion. Likewise, the operating margin may climb to 0.12-0.14. I expect a more stable economy and increased purchasing power among potential customers. The boom in the housing and automobile market may also have spillovers in P/C insurance.

Premiums Earned and Insurance Claims (Author Estimation) Operating Margin (Author Estimation)

Why The Hartford May Stay Afloat Amidst Inflationary Pressures

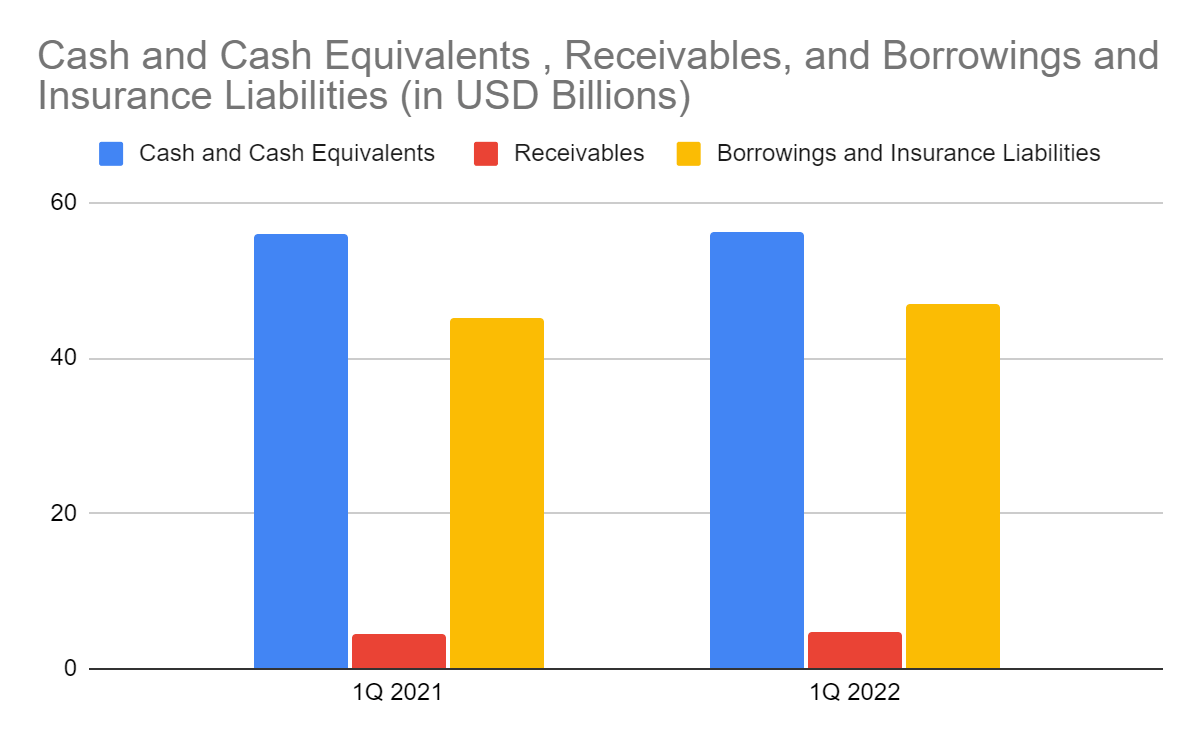

As a popular P/C insurance provider, The Hartford has a strong market positioning. Its solid customer base and strategic pricing drive its impressive revenues. Its efficient asset management allows it to keep its costs and expenses low. But, it does not rely on its demand, pricing, and efficiency alone. The efficient handling of its resources can also be seen in its solid Balance Sheet. Its cash balance and premium receivables remain stable. It may be due to stable inflows and increased market demand in its commercial lines.

The good thing about The Hartford is that most of its assets are generating more earnings. For example, it reinvests the majority of its assets. And most of these investments are liquid investments. These are short-term and held-to-maturity or available-for-sale financial assets. These are profitable as we can see in the continued increase in investment income. Of course, it is normal for insurance companies, but its prudence is what helps it drive its revenue. Its premium receivables also increase, showing more proceeds from increased demand and pricing. Given this, 89% of its total assets are liquid. So, HIG can sustain its operations, cover all liabilities even in a single payment, and even expand.

Cash and Cash Equivalents, Receivables, and Borrowings and Insurance Liabilities (MarketWatch)

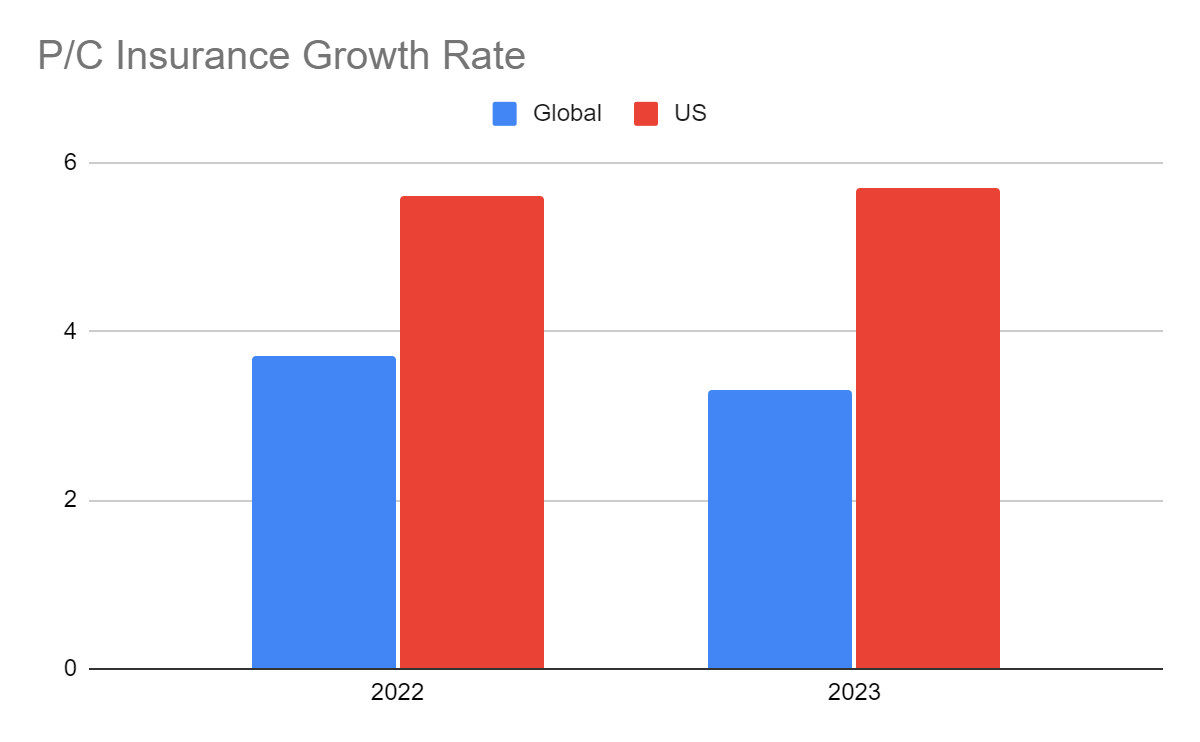

Other factors may stimulate its performance. P&C insurance is now more of a staple as the effects of climate change become more evident. The increased frequency of natural disasters and the pandemic highlight its integral role. In the US alone, 20 natural disasters hit many homes, leading to losses of $57 billion. Likewise, Asia experienced a record-breaking 432 natural disasters in 2021. It was way higher than the average in 2001-2020 at only 357 per year. It is no wonder that it may grow by about 6% per year in the US and 3.7% globally. HIG may leverage its popularity to market its products and services.

P/C Insurance Growth Rate (Insurance Journal)

The boom in the housing market has positive spillovers on P/C insurance companies. Despite the skyrocketing prices, the demand persists. In fact, 26 million Americans intend to buy a house in the next twelve months. They are more confident in their financial capacity to do so than in the previous year. It is no surprise that many homebuyers are also purchasing home insurance.

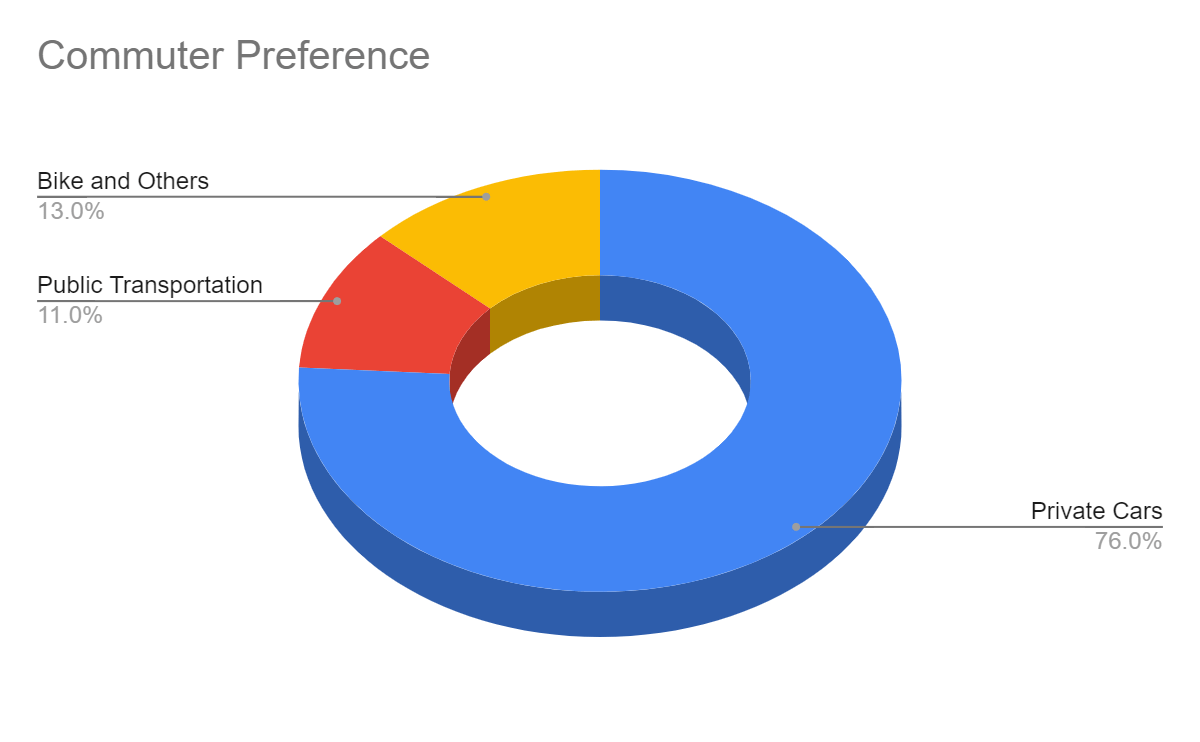

Automobiles are other potential growth drivers of The Hartford. Despite the inflated price of oil and fuel, the demand for cars remains high. In a recent study, car and car chip shortages are still evident. Despite the easing of restrictions, people prefer a private car when traveling. Another recent survey shows that 76% of commuters prefer a private car. As such, many analysts project that 15.2 million cars will be sold this year. In turn, more drivers today will have to get auto insurance. Note that many are willing to pay as high as $1,732 for their car insurance.

Commuter Preference (Statista)

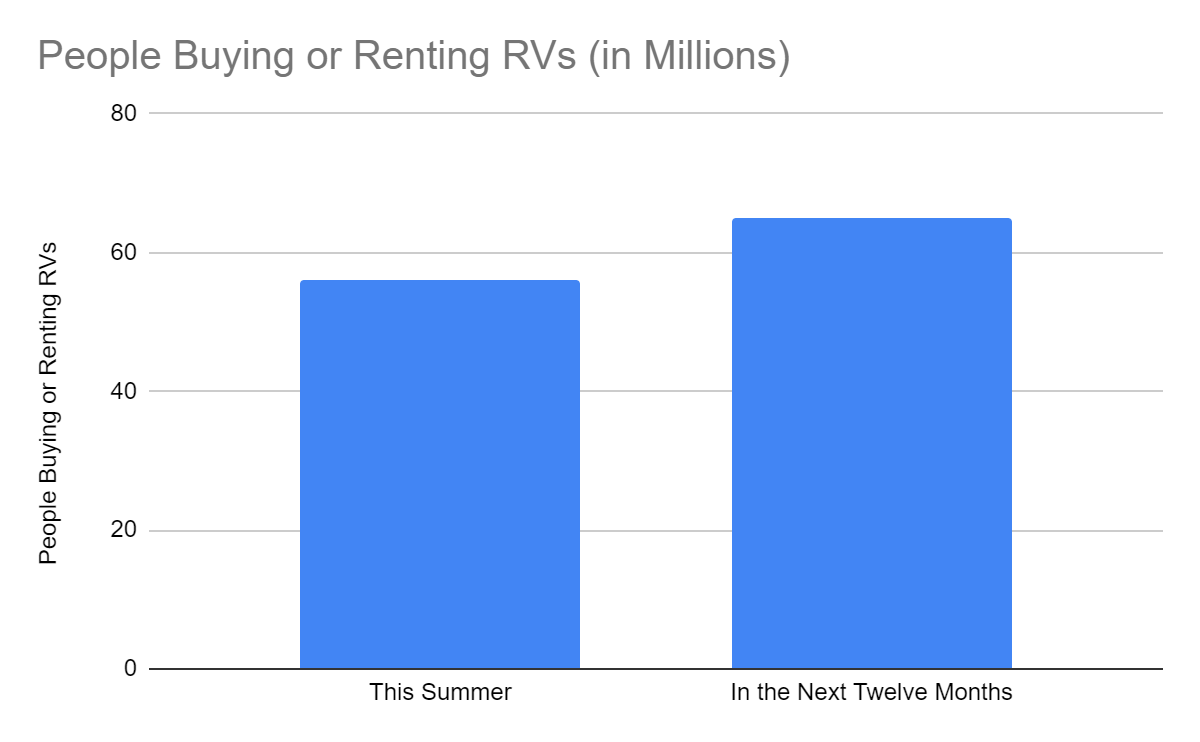

Likewise, RVs are on the rise as travelers choose to make more domestic travels this Summer. In a recent survey, 56 million Americans conveyed their interest to buy or rent RVs this summer. More buyers may flock into the market, reaching 65 million in twelve to twenty-four months. As such, it may drive the increase in RV insurance providers like The Hartford. It is logical as the company remains one of the best RV insurance providers. More estimations show a potential increase in the RV insurance market by 4.2% per year.

People Buying or Renting RVs (Camper Report)

Price Assessment

The stock price of The Hartford is moving sideways although it is geared upward. At $72.15, it is almost unchanged from its starting price with an increase of 4%. It makes the current not too expensive, given the little semiannual change. The P/E Ratio of 9.88 shows its cheapness since it is way lower than the standard industry ratio of 20-25. Also, it is lower than the average P/E Ratio of the S&P 500 of 15.97. The potential undervaluation must be considered as well. Currently, it is trading at 5-10x multiple, which is also the same as its peers on Seeking Alpha. Given the enticing growth prospects, I expect the EPS to reach $7.44-$8.44 in 2022-2024. Given this, the price may increase to $79-84 in 12-24 months. My projected price is within the historical multiples and near NASDAQ estimation.

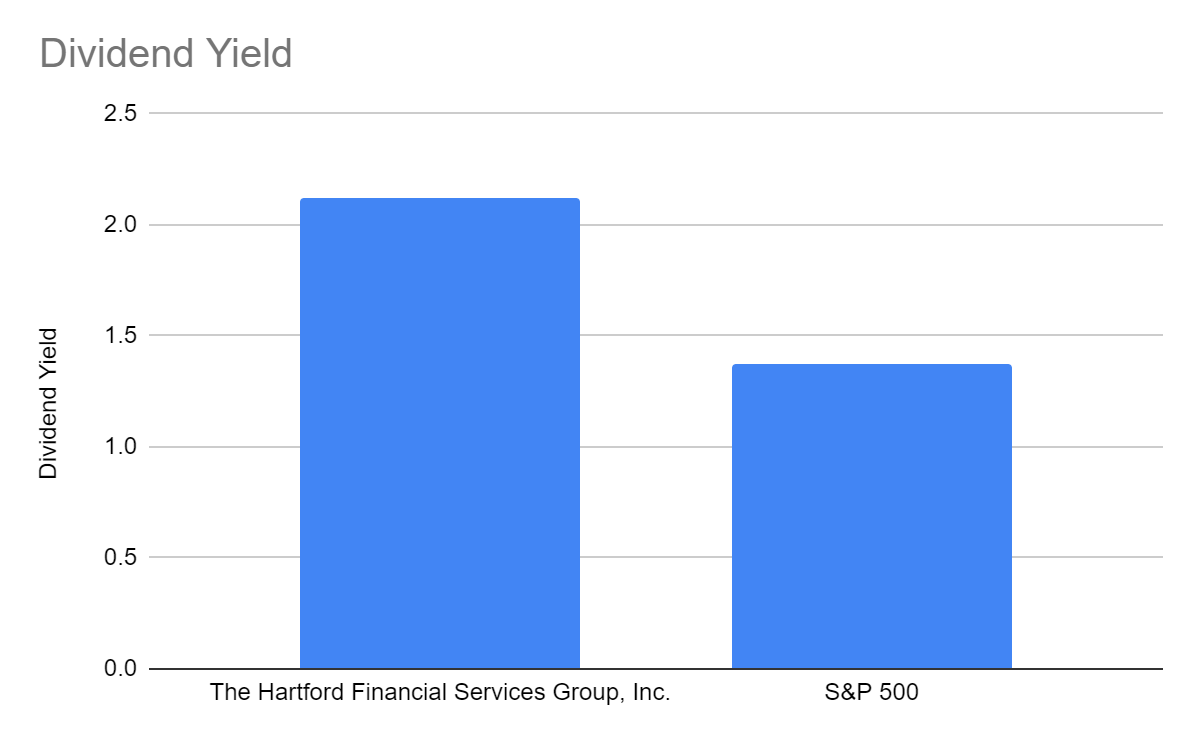

Moreover, HIG is a promising dividend stock. The per-share value had a consistent increase even during the pandemic. It now has an average growth rate of 11%. This year, it may increase to $1.54 per share, making it more attractive relative to the stock price. With a dividend yield of 2.14%, it is far higher than S&P 500 at 1.34%. To verify the enticing assessment, we may use the Dividend Discount Model.

Dividend Yield (NASDAQ)

|

Stock Price |

$72.15 |

|

Average Dividend Growth |

0.1087016388 |

|

Estimated Dividends Per Share |

$1.54 |

|

Cost of Capital Equity |

0.1288579 |

|

Derived Value |

$83.90819585 or $83.90 |

The derived value is adherent to my estimation with earnings multiples. There may be an upside of 16% next twelve to twenty-four months. The dividends may also be covered as the dividend payout ratio remains low at 30%. Indeed, it has enough capacity to sustain its operations. More growth prospects may drive the increase in the stock price.

Bottomline

The Hartford Financial Services Group, Inc. remains durable. It has sound fundamentals with its maintained profitability and stellar Balance Sheet. Also, it has enticing growth prospects amidst inflationary pressures. Likewise, the reasonable stock price and consistent dividends prove it to be ideal. The recommendation is that The Hartford Financial Services Group, Inc. is a buy.