To receive the Daily Shot newsletter in your inbox, please sign up at our Email Center. Previous issues of the Daily Shot are available online at DailyShotWSJ.com.

Have questions, feedback or comments? Contact author [email protected].

Twitter: @SoberLook

The Daily Shot: 27-Jan-20

• China

• Asia – Pacific

• The Eurozone

• The United Kingdom

• Europe

• Canada

• The United States

• Emerging Markets

• Commodities

• Equities

• Credit

• Rates

• Global Developments

• Food for Thought

China

1. The Wuhan coronavirus continues to spread, with quarantines appearing to be much less effective than some had hoped (see story).

Source: The Guardian; Read full article

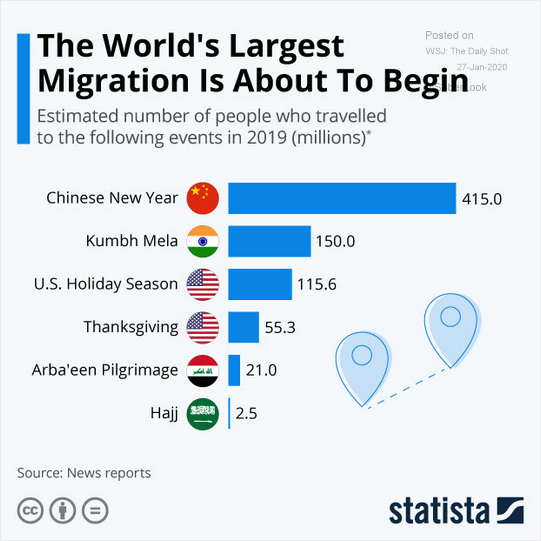

The authorities are extending the Lunar New Year holidays to limit travel, as the number of infections spikes.

Source: Reuters; Read full article

Source: Statista

——————–

2. While China’s markets are closed, stock futures are down over 5% today.

And the offshore renminbi dropped sharply as well.

Asia – Pacific

1. The Aussie dollar is having a rough month.

2. Singapore’s industrial production appears to be stabilizing.

The Eurozone

1. As we saw last week (#2 here), Germany’s Markit PMI surprised to the upside. On the other hand, the preliminary PMI report for France was disappointing. While French factory activity has been holding up, the nation’s service sector growth slowed in January.

Here is the French composite PMI and the GDP.

Source: Pantheon Macroeconomics

——————–

2. At the Eurozone level, manufacturing activity appears to be stabilizing as the index of new orders (second chart) approaches 50.

But France pulled the Eurozone services PMI index lower.

——————–

3. Better-than-expected figures on Germany’s factory activity further boosted the Eurozone Citi Economic Surprise Index.

Source: Citi

4. Credit has been easing in the euro area.

Source: Gavekal

5. Long-term inflation expectations are increasingly anchoring the CPI below 1.5%.

Source: Frederik Ducrozet, Pictet Wealth Management

6. How much political risk is already priced into the Italian government debt spreads?

According to Gavekal: – “Fundamentals suggest that Italian bonds should be priced between Greek bonds and Portuguese and Spanish bonds. At 159bp, Italy’s spread is closer to Greece’s spread (164bp) than Portugal’s (66bp) and Spain’s (66bp). This suggests investors are already asking for a significant premium to hold Italian debt, which may limit the downside potential of any bond market sell-off.”

Source: Gavekal

Update: Matteo Salvini suffered a substantial loss in a closely-watched regional election. Italian bond yields tumbled in response.

Source: @WSJ; Read full article

——————–

7. Ireland’s economic sentiment is rebounding, helped in part by the UK elections outcome.

The United Kingdom

1. Business sentiment rebounded sharply after the elections, with the Markit PMI report surprising to the upside. Services PMI figures were especially strong.

• Manufacturing:

• Services:

——————–

2. The PMI surprise sent the market-based probability of a rate cut this week lower.

3. What’s the long-term impact of Brexit on the economy?

Source: Pantheon Macroeconomics

Europe

1. The Swiss franc continues to grind higher as traders seek safe-haven assets.

2. Czech consumers are increasingly concerned about inflation.

Source: ING

Canada

1. After four months of declines, the rebound in retail sales was disappointing.

Here are a couple of regional trends.

Source: Desjardins

——————–

2. The charts below show consumer insolvencies and credit growth.

Source: CIBC Capital Markets

The United States

1. The January Markit PMI report was mixed.

• Growth in factory activity slowed.

Indices of new orders, export orders, and order backlog declined.

However, the outlook on future output seems to be rebounding.

• Service-sector activity strengthened, and employment bounced from the recent lows (second chart).

——————–

2. Next, we have some other survey-based economic indicators.

• The New York Fed’s regional service-sector activity:

Source: NY Fed

• The Yelp local economy index (dragged lower by brick & mortar retail):

Source: Yelp; Read full article

• Gallup’s economic confidence index:

Source: Gallup; Read full article

• Online search activity for charge-offs, foreclosures, and liens:

Source: Arbor Research & Trading

——————–

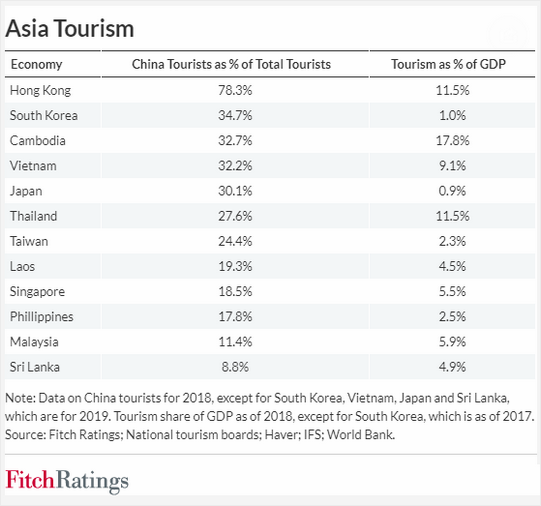

3. How exposed is the United States to the Wuhan Coronavirus? Here is the number of visitors from Asia?

Source: Fitch Ratings

4. The Conference Board Leading Economic Index turned negative on a year-over-year basis for the first time this cycle after having peaked in July of last year. However, as we noted last week (#2 here), the latest decline appears to be transient, and we should see a rebound in this index.

Source: @MacroOps

5. Capital Economics is estimating the 4th-quarter GDP growth to be 1.9% (consensus is 2%), with lower US imports (higher net trade) offsetting slower consumption and inventory cuts.

Source: @LizAnnSonders, @CapEconUS, @Refinitiv

6. Market-based inflation expectations are moderating again.

Emerging Markets

1. EM stock futures are down sharply on Wuhan virus fears.

EM currencies are softer as well. Here is JP Morgan’s index.

The Thai baht rally appears to be over, with the latest declines driven by the virus uncertainty as well as the central bank’s desire to halt the currency’s gains.

——————–

2. Asian bond spreads rebounded from the lows.

h/t Andrew Monahan, @TheTerminal

3. India’s unsold housing inventory keeps climbing.

Source: ANZ Research

4. Hungary’s economic sentiment is rolling over.

The Hungarian forint is trading near multi-year lows against the euro.

——————–

5. Mexico’s economic activity showed a deeper contraction than markets were expecting.

Economists now don’t think that Mexico’s GDP grew at all last year.

——————–

6. The Chilean sovereign CDS spread is widening again.

Commodities

1. The Wuhan Coronavirus uncertainty is pressuring industrial commodity markets.

• Iron ore in Singapore (down 6%):

• Crude oil:

• Copper:

——————–

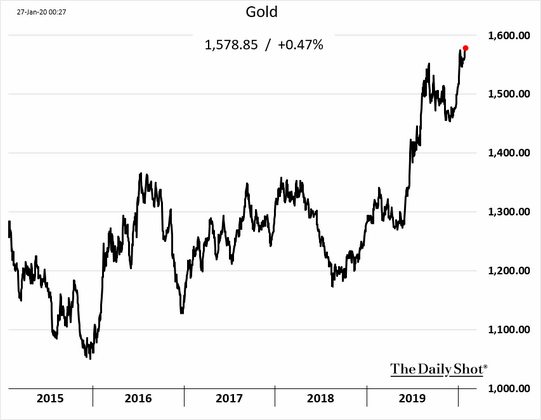

2. Gold hit a multi-year high.

3. US soybean prices continue to weaken.

4. Managed money outright long positions in wheat surged last week, defying historical trends.

Source: @kannbwx

Wheat appears to be overbought, and sellers are entering at resistance.

Source: @DantesOutlook

Equities

1. The Wuhan Coronavirus is showing up across the US, unnerving investors.

Source: Fox News; Read full article

• S&P 500 futures:

• VIX futures:

——————–

2. We finally saw some volatility last week.

Source: @markets; Read full article

3. Equities and Treasuries have been sending different signals.

Source: @financialtimes; Read full article

4. The underperformance of US small caps continues to widen.

5. Energy has been a drag on the S&P 500 Q4 earnings and performance.

Source: @WSJ; Read full article

Source: Yardeni Research

——————–

6. Trading activity at discount brokers climbed since the implementation of zero-commissions.

Source: @WSJ

Credit

1. US corporate high-yield credit spreads are starting to widen, and technicians are signaling a bottom here.

Source: @TommyThornton

2. The iShares High Yield Corporate Bond ETF (HYG) is under pressure at resistance.

Source: @DantesOutlook

3. The multi-year decline in investment-grade municipal and corporate yields has been impressive.

Source: @bopinion; Read full article

4. European high-yield issuance soared this month.

Source: @markets; Read full article

5. US speculative-grade companies have almost $1.2 trillion of debt maturing over the 2020-2024 period. That’s up 14% from the year prior, setting a new record, according to Moody’s.

Source: @lisaabramowicz1

6. Credit Suisse expects leveraged loan default rates to surpass high yield bonds.

Source: Credit Suisse

Rates

1. The US 10-year Treasury yield broke below a 4-month uptrend.

Source: @DantesOutlook

2. Here is the attribution of Treasury yield changes since the October FOMC meeting (BE = inflation expectations, RY = real yields).

Source: Morgan Stanley Research

3. The Treasury curve is flattening again.

4. The market still expects a Fed rate cut this year.

Source: Morgan Stanley Research

Global Developments

1. Which countries have the most visitors from mainland China?

Source: Fitch Ratings

2. Manufacturing has not been contributing to global growth in recent quarters.

Source: @SergiLanauIIF

3. Which exporters are most vulnerable to the Phase-1 US-China trade deal?

Source: @ZSchneeweiss, @MaevaDebarge, @TomOrlik; Read full article

——————–

Food for Thought

1. The drop in state & local US tax deductions:

Source: @WSJ; Read full article

2. US sources of federal tax revenue:

Source: Deutsche Bank Research

3. IRS audits:

Source: @WSJ; Read full article

4. Revenues from cloud infrastructure:

Source: @WSJ; Read full article

5. US consumer technology usage:

Source: Pew Research Center; Read full article

6. Making America great again:

Source: @YouGovUS; Read full article

7. The impact of having kids on wages:

Source: @voxdotcom; Read full article

Source: @voxdotcom; Read full article

——————–

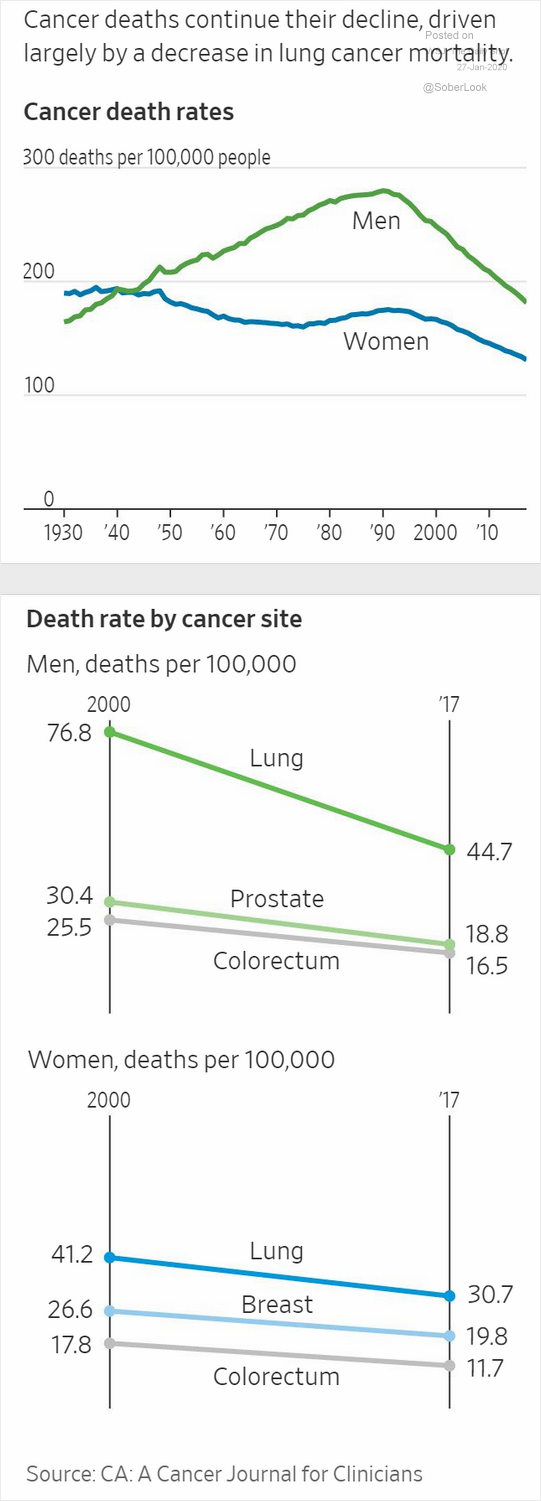

8. Cancer deaths:

Source: @WSJ; Read full article

9. US meat consumption:

Source: @WSJ; Read full article

10. US population growth (slowest in history):

Source: @WSJ; Read full article

——————–