Justin Sullivan

Tesla (NASDAQ:TSLA) has lost close to 20% of its value this month as it struggles to recover from its biggest intraday wipeout of close to 9% the day after reporting a 3Q22 delivery miss. The stock fell further in post-market trading Wednesday (October 19) as investors grapple with mixed third quarter results that consisted of an anticipated revenue miss and an earnings beat.

Given Tesla’s revenue miss was largely expected due to the earlier reported delivery miss, with the company’s forward outlook still lacking visibility as management reiterates broad-based uncertainties over supply chain / logistics constraints and the near-term global economic outlook (e.g. raw material inflation), we do not consider there a sufficient catalyst to help the stock sustain its lofty valuation – especially ahead of further monetary policy tightening and a looming economic downturn that is bound to impact forward performance. As such, we are maintaining expectations for more downsides in the Tesla stock, as deteriorating macroeconomic conditions call for a further reduction to lofty valuations over coming months.

Tesla Vehicle Demand Risks

Demand for Tesla’s vehicles is a key focus area for investors, especially after its delivery miss in 3Q22. Despite Tesla’s allusion to logistics issues for the known miss, the shortfall has inevitably drawn investors’ worries over demand risks as consumer confidence weakens ahead of an imminent recession.

While Tesla’s 3Q22 delivery volumes fell short of consensus estimates for 37,938 vehicles, its quarter auto revenues of $18.7 billion ($18.4 billion, ex-credits), which represented y/y growth of 55.9%, also fell shy of consensus estimates. This again underscores the weakening link over Tesla’s earlier-touted pricing advantage, as discussed in our previous coverage, following multiple MSRP increases this year aimed at compensating for rising input costs – and now, a volume shortfall. And the pricing advantage will only deteriorate further if real demand shows structural deterioration – especially across Tesla’s core U.S. and Chinese EV markets.

Let’s start with the U.S. Although Tesla does not break down delivery volumes by geography, the bulk of its consolidated revenues are still coming from the U.S. The company currently accounts for about 75% of the U.S. EV market share, but as we have discussed in a previous coverage, that number is bound to come down with the increasing availability of different models across various types and pricing segments.

In addition to the near-term macro headwinds observed across Tesla’s core markets (further explained here), the EV titan faces a bigger, and more structural risk of market share erosion over the mid- to longer-term as competition intensifies. The next decade will be an era of electrification with significant opportunities for the sector as EVs take the center stage. The European Federation for Transport and Environment predicts more than 300 available EV models within the European automotive market by 2025, while the IHS Markit predicts more than 130 available EV models in the U.S. by 2026, which is equivalent to the number of ICE options available in the market today.

While Tesla often reiterates the fact that it is still “selling every vehicle it makes”, the company appears to be showing its first signs of near-term market share loss in the U.S., which is ironic as EV adoption enters an inflection point in the region. Despite our optimism over Tesla’s ability to regain share over the longer-term given its competitive advantage in both input costs and early procurement of key supplies, the near-term risks of demand destruction certainly do not bode well for the highly valued stock under today’s market climate.

In the U.S., Tesla is now facing a rapid deterioration in consumer confidence as inflation remains at record-high levels, while the Fed’s aggressive pace of monetary policy tightening is now amplifying risks of recession within the next 12 months. Although American drivers are more inclined than ever to consider EVs for their next car – thanks to the increasing availability of public charging infrastructure, improved battery technologies, favourable financial incentives, and expanding model options – many are delaying the decision due to surging inflation. The average price of an EV in the U.S. today is pushing $67,000, with Tesla contributing to the bulk of it, and still a wide distance from achieving price parity with ICE vehicles averaging $45,622 – a new record as rising input costs and supply shortages have either pushed automakers to raise prices or reallocate production capacity to higher priced models that are more profitable. Increasing borrowing costs implemented by the Federal Reserve to tame inflation has also taken average auto loan interest rates towards a record 6%, which effectively deters the bulk of American drivers from making a new car purchase anytime soon – more than 80% of new vehicle purchases in the U.S. are financed via auto loans today. Only some 20% of drivers interested in considering an EV for their next car purchase are expected to make the move “within the next two years, down from 36% in 2019”.

What this means for Tesla is that demand will likely slow in the near-term as a result of a weakening economy. Again, given Tesla is still selling every unit it makes, the anticipated near-term demand slowdown is not expected to materially impact its revenues. However, a diminishing backlog does not make a supportive factor for its lofty valuation that calls for perfect execution under today’s market climate. A diminishing backlog would also strip Tesla of its pricing gain advantage needed to drive its industry-leading profit margins, which is a key factor that has been supporting its lofty valuation today.

And say in two years, when demand returns, Tesla is expected to be grappling with heightened competition then. As discussed in our previous coverage and consistent with management’s expectations, Tesla is poised to experience market share loss over the mid-term:

The increasing availability of non-Tesla EV models across a wide array of performance, range capability, and price categories is what has encouraged rapid mass market EV adoption in the U.S., heightening risks of share erosion for Tesla over the longer-term.

It is not until the latter half of the decade when Tesla’s supply and cost advantage kicks in to help it recapture market share. Between now and then – especially through 2023 as the global economy works through mounting uncertainties spanning record inflation, rising interest rates, and a potential recession – we expect the stock’s valuation to face an inevitable downward adjustment from current levels.

The recently enacted Inflation Reduction Act (“IRA”), which is meant to bolster U.S. EV adoption and demand with attractive purchasing incentives in favour of Tesla’s offerings, will also be a barrier to the company’s need for strong near-term sales in support of its lofty valuation amid volatile market conditions. Tesla purchases are currently not eligible for EV subsidies given the company has long used up its quota under the pre-IRA incentive scheme. The $7,500 tax credit that some of Tesla’s vehicles will be eligible for under the IRA will not kick-in until next year, meaning prospective car owners or those with existing reservations – which are mostly sensitive to price changes under today’s inflationary environment – will likely be delaying deliveries for a couple of months.

Although management has not made any specific reference to an earlier full-year guidance for 50% y/y delivery growth and production of 1.5 million vehicles in the 3Q22 Shareholder Deck released prior to the earnings call, pointing to the 50% annual growth target “over a multi-year horizon” instead, the expectation for muted 4Q22 sales as a result of the aforementioned headwinds facing Tesla’s U.S. business risks derailing the company from its goals, and taking its lofty valuation a leg lower over coming months.

Now onto China. The rapid recovery in Giga Shanghai’s production volumes following COVID disruptions in the spring, and the plant’s expanded capacity that has recently come online are supposedly good things for Tesla as China becomes an increasingly substantial market for the EV titan. But recent observations of shrinking wait times, coupled with sales figures that trail local rival BYD (OTCPK:BYDDF / OTCPK:BYDDY) by wide margins are inevitably contributing further to investors’ concerns over demand risks.

EV sales (including plug-in hybrids) represented 31.8% of new passenger vehicle sales in China during September, a new record that far exceeds the government’s previously established goal to achieve a 20% penetration rate by mid-decade. Yet, considering lower-priced rival BYD sold 1.2 million EVs in the nine months through September with the bulk of it attributable to the Chinese market, compared to Tesla’s 318,000 EVs sold in the region over the same period, underscores that demand is largely entrenched in the price-sensitive mass market. This is also consistent with data showing the SAIC-GM-Wuling’s Hongguang Mini, which has a starting price of under $5,000, being the best-selling EV in China, as well as local premium EV maker NIO’s (NIO) upcoming plans to launch two lower-priced sub-brands to better capture demand from China’s smaller Tier 3 and Tier 4 cities.

While expanded production capacity at Giga Shanghai means Tesla can now better convert its growing backlog in China into recognized revenues and profits (Giga Shanghai currently boasts the most favourable auto margins), it can only achieve a further improvement to economies of scale if demand keeps up too. To outcompete the growing volume of local mass market competition as mentioned in the earlier section, Tesla may need to introduce a lower-priced offering sooner than it had previously expected.

This circles back to previous market speculations over Tesla’s development of a $25,000 model , or “Model 2”, which CEO Elon Musk had said is currently not a priority during the 4Q21 earnings call given protracted industry-wide supply chain constraints and a greater preference for developing its autonomous driving technology. But with the long-awaited Semi commercial trucks starting customer deliveries by the end of the year, which runs on the 4680 cells critical to enabling lower-priced models (further discussed here), perhaps the Model 2 will come sooner than expected after all to safeguard demand from destruction, and salvage investors’ confidence in Tesla’s valuation premium. However, given there has been no direct update on prospects for a lower-priced model during its latest earnings call, we do not see any immediate catalyst in sight that can provide sufficient support to Tesla’s lofty valuation relative to peers under the dour market climate ahead – especially as investors identify competitively-priced Chinese EV brands as a key looming threat to Tesla’s long-term growth trajectory.

TSLA Stock: Fundamental and Valuation Update

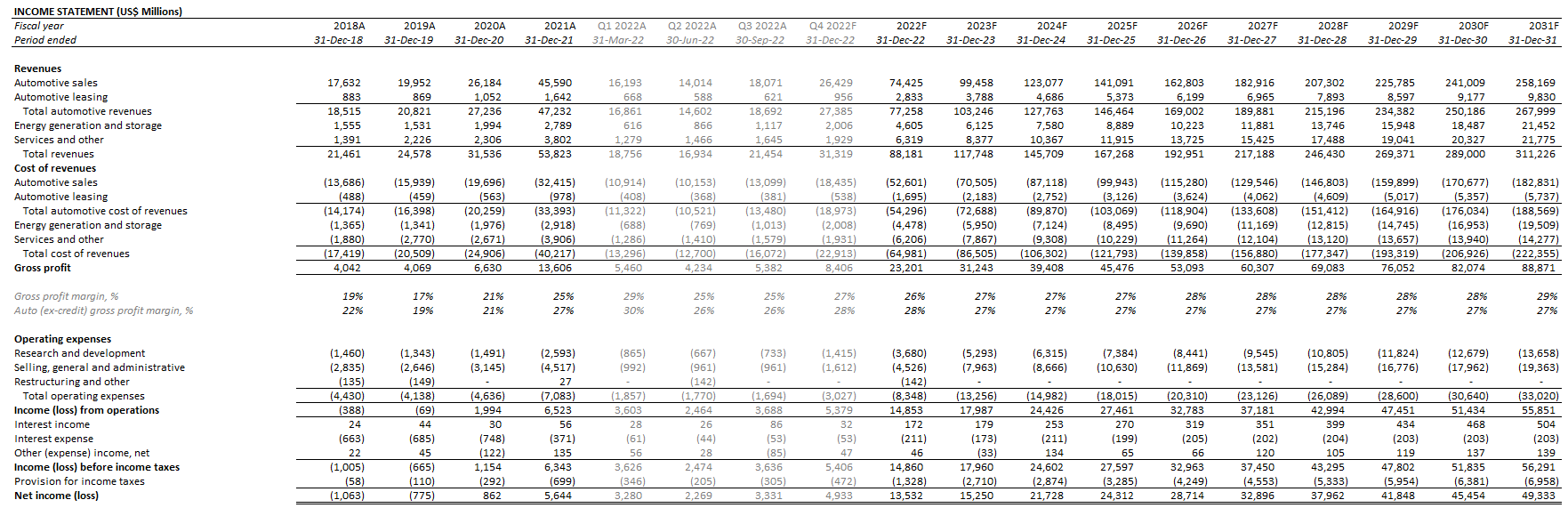

Adjusting our most recent forecast for Tesla’s actual 3Q22 fundamental performance, as well as preliminary commentary on the company’s near-term forward outlook released in the Shareholder Deck, we are projecting total revenue of $88.2 billion by the end of the current year. The figure will be primarily driven by growth in auto sales (ex-credit sales) based on deliveries of about 1.4 million vehicles, barring any continuation of significantly logistics constraints experienced in 3Q22.

While overall profit margins have performed better than expected in the third quarter, auto margins in 3Q22 which came in at about 26% fell short of consensus estimates of about 28% and fell further from the figure in 2Q22. This continues to underscore the burden of additional ramp-up costs at Giga Berlin and Austin, which will likely persist into 4Q22 as Tesla hurries to begin customer deliveries on the Semi truck by the end of the year.

Tesla Delivery Forecast (Author) Tesla Financial Forecast (Author)

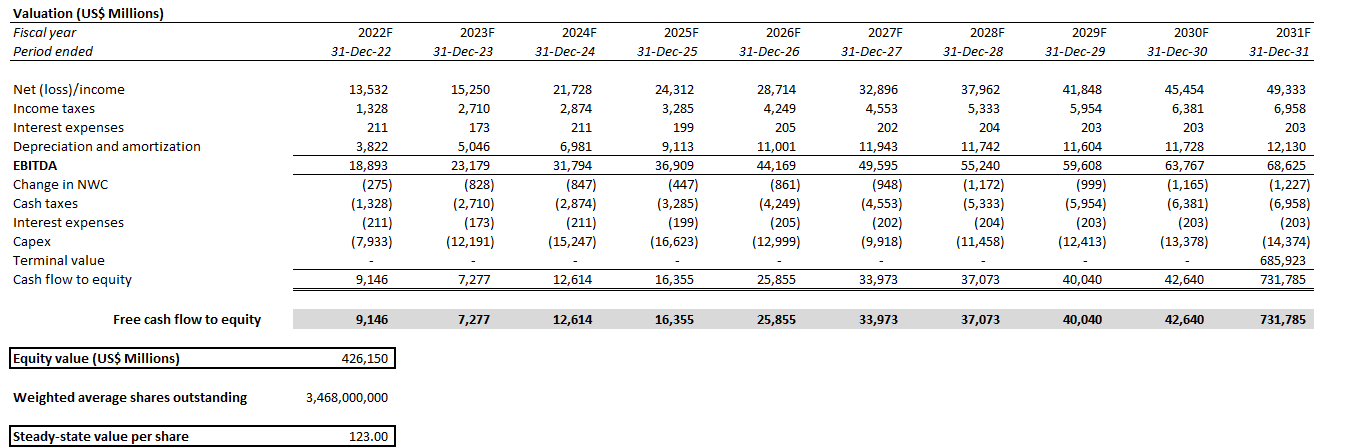

On the valuation front, we are maintaining our near-term bear case PT at the $150-level, derived based on the steady-state and future value creation methodology discussed in the previous coverage. We continue to brace for a drop in the stock to the sub-$200 level over coming months considering no immediate catalysts to support Tesla’s lofty valuation, as near-term macroeconomic headwinds pickup.

Tesla Valuation Analysis (Author) Tesla Valuation Analysis (Author)

Tesla_-_Forecasted_Financial_Information.pdf

Risks to Consider

Given the foregoing analysis on Tesla’s bear case is primarily a near-term expectation given rapidly deteriorating macroeconomic conditions, timing is a key risk area to consider. Specifically, uncertainties over the Fed’s policy tightening trajectory, where inflation is headed, and whether a recession is near are risk factors over whether and when the foregoing bear thesis on Tesla might materialize.

For now, we expect the Tesla stock to remain volatile through 1H23, over which interest rate hikes are expected to peak and an economic recession is expected to take place, which will likely impact Tesla’s near-term fundamental performance and cause its lofty valuation to buckle. In addition to macroeconomic headwinds, Tesla is also dealing with some internal matters that could take its valuation another leg lower – namely, Musk’s bid for Twitter (TWTR) which could lead to another selloff of its stake in Tesla to fund the transaction. So there is a reasonable case for a downward valuation adjustment to the Tesla stock over coming months.

However, some other potential factors that could counter this short-term bearish expectation include the fact that Tesla still has a few tools in its pocket to buoy investors’ confidence in the stock. As mentioned in the earlier section, Tesla’s sudden decision to begin customer deliveries on the Semi commercial trucks before the end of the year potentially implies significant progress in ramping up productions of the long-awaited 4680 cells critical to building a lower cost vehicle. This suggests that there is a chance Tesla could and might fast-track the development of a lower price mass market product to overcome impending near-term market share loss to cheaper rival offerings, attract consumer dollars amid an inflationary environment, and accelerate its longer-term plans to sell 20 million vehicles per year. Pulling out the wild card could potentially overshadow the anticipated impact from both macroeconomic and internal share-selling headwinds to the stock’s lofty valuation today, and trump the near-term short thesis.

Final Thoughts

Nonetheless, with a lofty valuation come high expectations – and this is the case we see for Tesla ahead of worsening macroeconomic conditions. Alternatively, we have seen a lower bar set by investors for companies that have had their valuations already battered earlier this year, such as Netflix (NFLX) which staged a strong rally earlier this week after a return to user growth overshadowed a weaker-than-expected forward guidance. As such, we expect a further and more rapid convergence between the valuations of those that are overvalued and oversold over coming months as investors bake their “pessimism” over near-term macroeconomic prospects into stocks – such as Tesla – that have largely maintained hefty premiums amid the violent market rout observed in the first half of the year.

While we remain optimistic over Tesla’s sustained market leadership in global EV sales from a long-view perspective, the dire near-term market outlook likely harbingers some downside risks to the stock, and warrants reconsideration from those looking to invest at current levels.