CoffeeAndMilk/E+ via Getty Images

The shopping center segment has seen a decent rebound over the past 12 months, but mall REITs remain discounted, as I recently highlighted in this piece about Simon Property Group (SPG).

Notably, this also includes the pure-play outlet shopping REIT, Tanger Factory Outlet Centers (NYSE:SKT). In fact, SKT’s shares have returned just 2.5% over the past 12 months, and while that’s hardly anything to write home about, I believe it presents investors with an asymmetric risk-reward potential, so let’s get started.

SKT: Shop Until You Drop

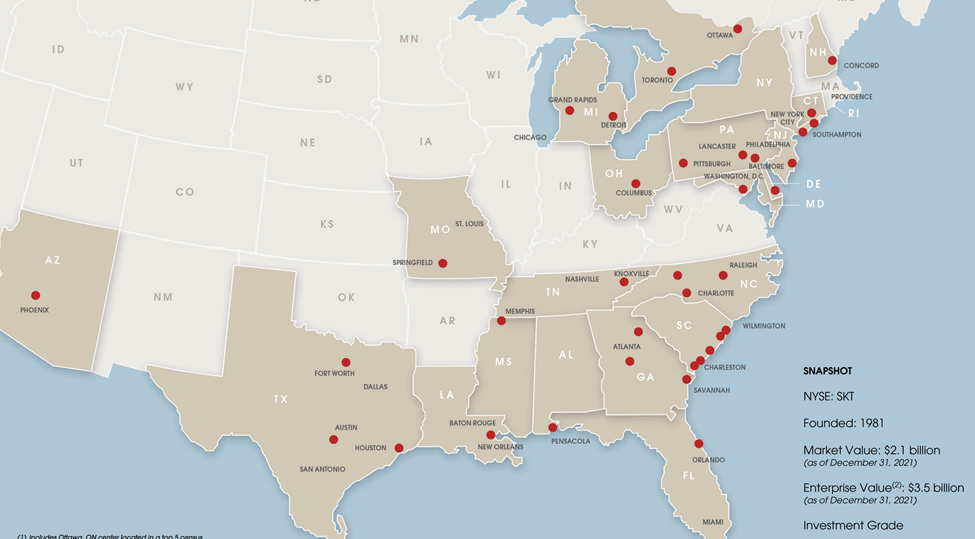

Tanger Factory Outlet is the nation’s largest pure-play outlet center REIT, with 36 centers spread across 20 states and Canada, covering 2,700 stores leased to 600 different brand name companies.

SKT Properties (Investor Presentation)

Notably, SKT has 41 years of experience in this industry and has built a strong reputation with retailers who depend on the outlet model as an important distribution channel.

Its properties are well-located, with 90% of square feet in a Top 50 MSA or leading tourist destination, and 94% of the portfolio is open-air, and this helps to alleviate pandemic-related pressures. SKT also counts top retailer names such as Gap (GPS), PVH (PVH), Nike (NKE), Columbia, and Under Armour (UA) among its Top 10 tenants.

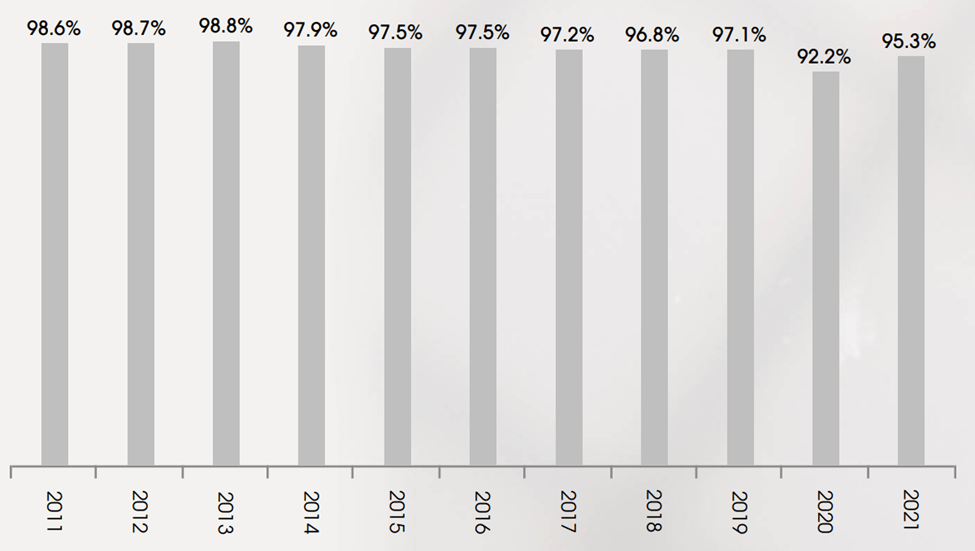

Anyone who’s followed SKT closely would know that the REIT has faced pressures stemming from retailer turnover and COVID over the past few years. It appears, however, that retail cycle is demonstrating a rebound. This is supported by 95.3% occupancy and a 16.0% increase in same center NOI for the full year 2021.

Also encouraging, tenant sales per square foot have also solidly rebounded by 17.6% from 2019-levels to $468, indicating that the outlet model is durable and moving beyond the challenges it faced even prior to the start of the pandemic. As shown below, SKT’s occupancy is now nearly in line with that of pre-2020 levels.

SKT Occupancy (Investor Presentation)

Additionally, SKT benefits from the fact that its stores are like fungible boxes that can be easily reconfigured to suit the needs of prospective tenants replacing outgoing ones.

Blended cash rent spread was -0.6% during 2021, but the aforementioned healthy tenant metrics portends a potential reversal this year. This is supported by the following comments by the CEO during the recent March investor conference:

This year, we have a unique opportunity to increase rents with 19% of our space coming up for renewal against a backdrop of strong sales productivity, and low occupancy cost for our tenants. In fact, in January our blended 12-month spreads turned positive and in place rents represented an occupancy cost ratio of approximately 8%. This is meaningfully lower than any other retail distribution channels despite Tough comps due to January winter weather.

Our rolling 12-month tenant sales sustain the record high level achieved in December. Leasing activity is accelerating as demand is growing for space in our open air portfolio. And we did not recapture any space during the fourth quarter due to early terminations and are now seeing open to buys from retailers and alternative uses like home, food and beverage and other experiential brands.

Meanwhile, SKT pays a well-covered dividend, with a dividend to 2021 Core FFO/share payout ratio of 41%. It also doesn’t have significant debt maturities until April 2024, and carries a reasonably low net debt to adjusted EBITDAre ratio of 5.5x, down from 7.2x at the end of 2020.

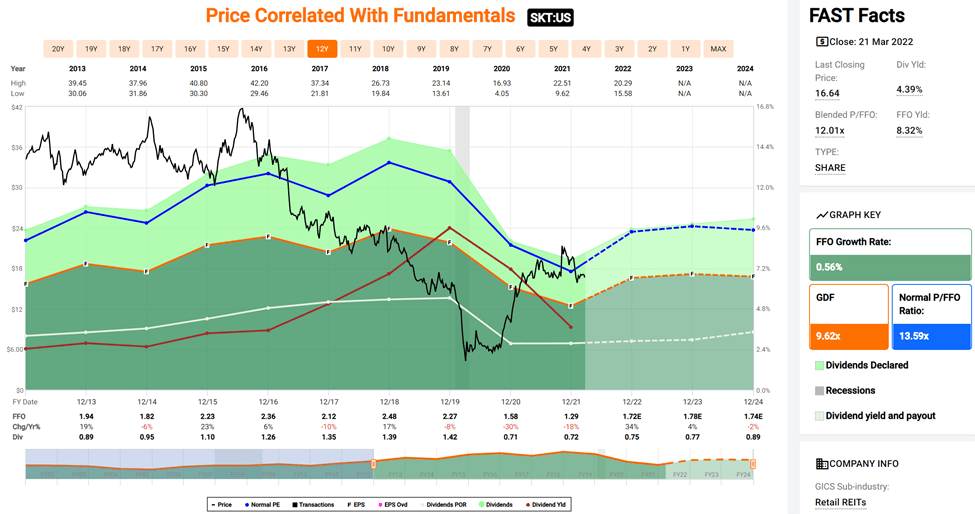

SKT appears to trade in bargain territory at the current price of $16.98 with a forward P/FFO of 9.9x, sitting well below its normal P/FFO of 13.6 over the past decade. While sell side analysts have a consensus Hold rating on the stock, the average price target of $19 implies a potential one-year 16% total return including dividends.

SKT Valuation (FAST Graphs)

Investor Takeaway

It appears that SKT is on the rebound. The REIT has a healthy portfolio of high-quality properties, and is seeing increased demand for its space. With a dividend yield of over 4%, a payout ratio of 41%, and a low net debt to adjusted EBITDA ratio, SKT appears to be a good investment at the currently discounted price.