JamesBrey/iStock via Getty Images

Inflation has made a number of headlines over the past 12 months, with some of the causes being rising commodity prices and supply chain disruptions. Another driver of inflation has been loose monetary prices with record amounts of fiscal stimulus being introduced to the money supply since the start of the pandemic.

Consumer staple stocks and real estate are some of the more obvious asset classes that investors can shelter some cash in an inflationary environment. Well-run asset managers like T. Rowe Price (TROW) are another good option, in my view, especially considering their asset-light business models that make them “cash cows”. In this article, I highlight what makes TROW a good buy after the recent price drop.

TROW: Your Opportunity Is Knocking

T. Rowe Price is based in Baltimore, Maryland and was founded in 1937. Since then, it’s evolved into a global investment management organization with $1.69 trillion in assets under management as of the end of 2021, and serves clients in 51 countries. TROW’s products include actively-managed funds that hold equities, fixed income, blended, and target dated retirement funds.

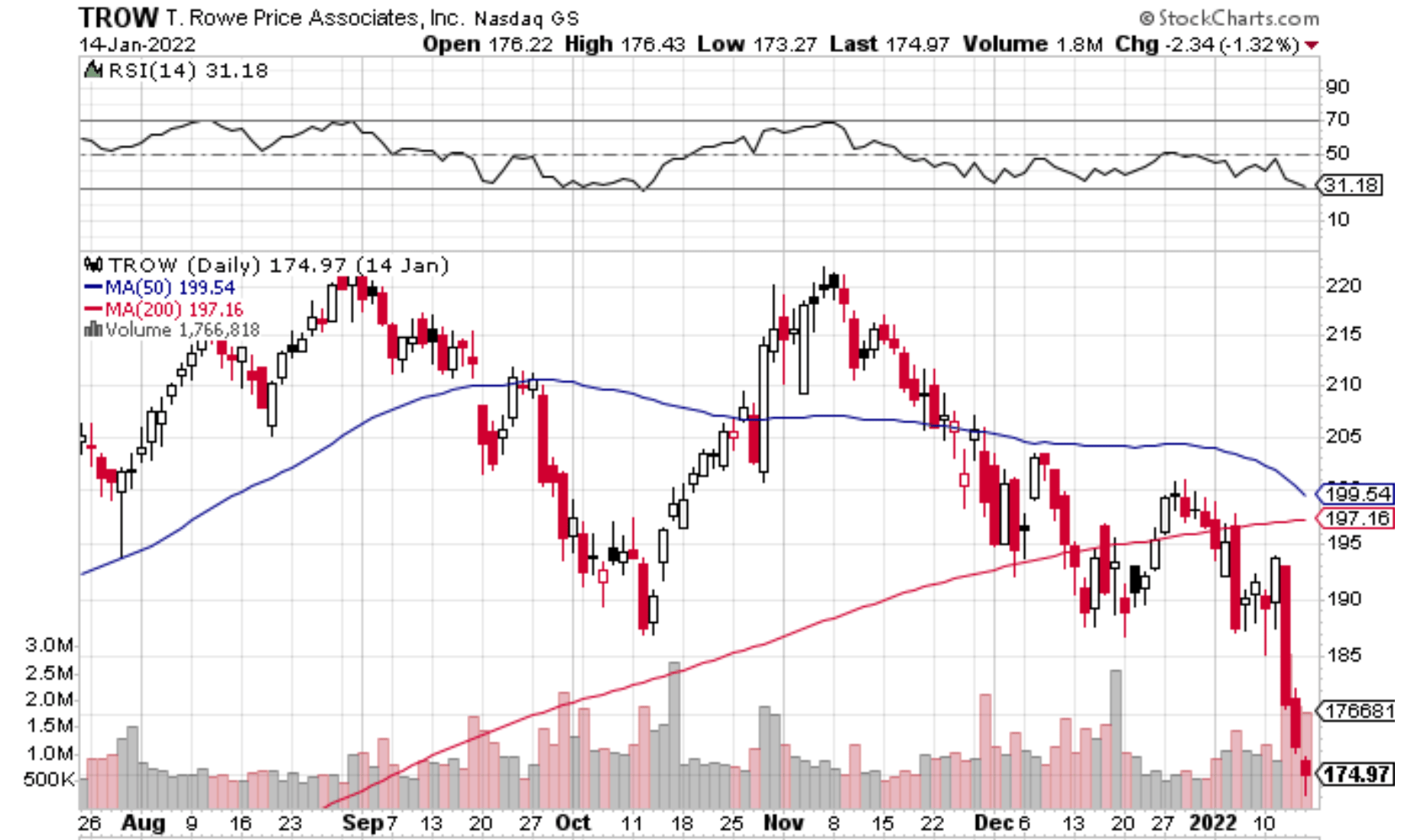

TROW has seen material share price weakness over the past couple of months, falling from the $220-level at the start of November to $175 at present. It now trades below both its 50 and 200-day moving averages of $199 and $197, respectively. Plus, as shown below, the recent drop in TROW’s price has resulted in an RSI score of 31, indicating that it’s now in oversold territory.

TROW Technical Chart

StockCharts

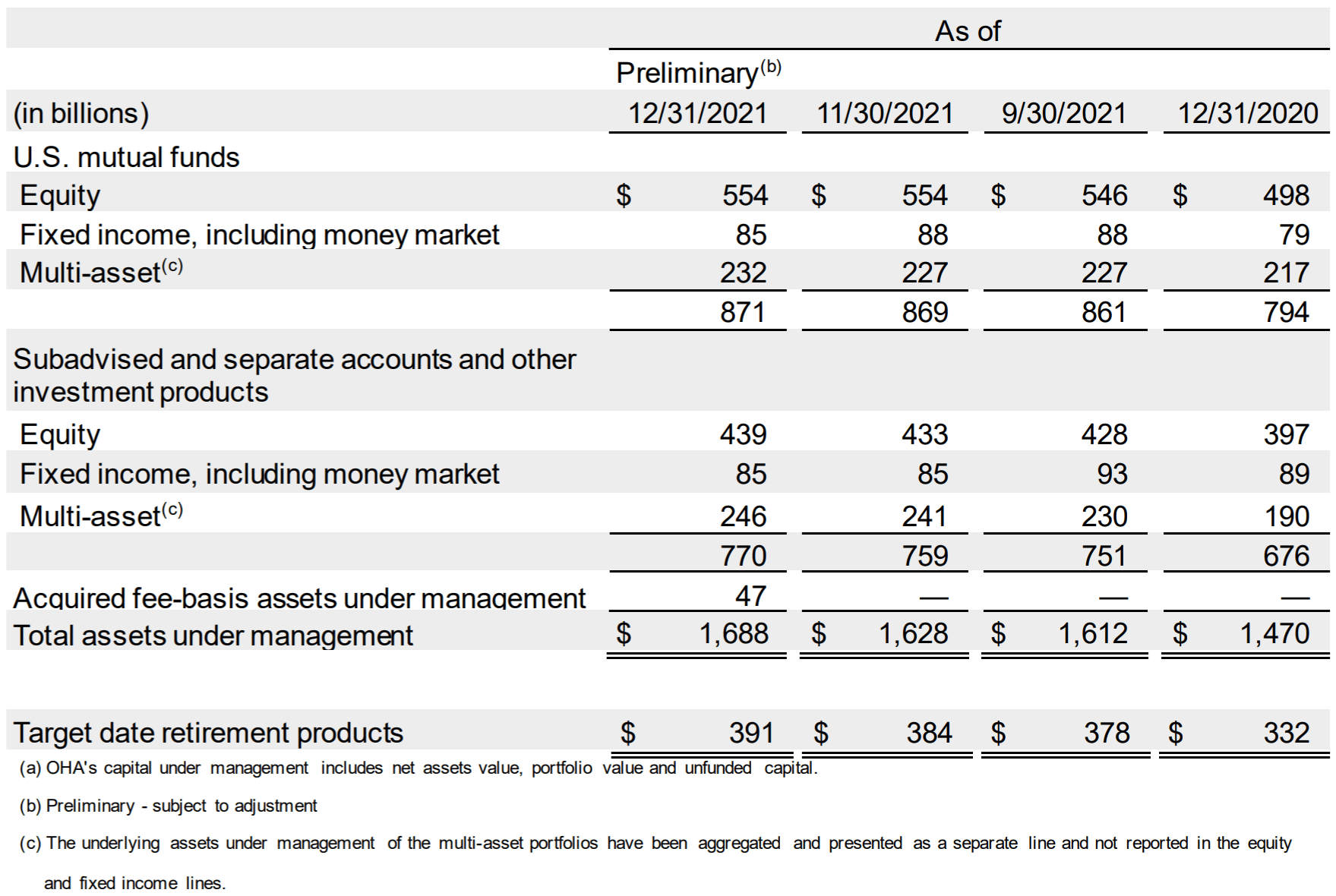

I see the sell-off as being unjustified considering the underlying strength of the business. This is supported by robust AUM growth of 3.7% on a month-over-month basis to $1.69 trillion at the end of December. This also represents a 15% YoY AUM growth from $1.47 trillion at the end of 2020. As shown below, TROW’s AUM growth is led by double-digit growth in its equity and blended asset investment products and funds.

TROW AUM Table

Looking forward, TROW is well-positioned to consolidate the asset manager sector through its position as a juggernaut in the space. This is reflected by its recent acquisition of Oak Hill Advisors, a leading alternative credit manager with $53 billion of capital under management.

This transaction strengthens TROW’s position across private, distressed, special situations, structured credit, and real asset strategies. This transaction also further bolsters TROW’s scale, and management noted the potential synergies in this press release:

“OHA and T. Rowe Price share organizational cultures that focus on long-term investment excellence and delivering value for clients and that are grounded in collaboration, trust, and integrity. As we bring together complementary capabilities and distribution, we can capitalize on growth opportunities for new product development that add value for our clients and stockholders. We share a vision with OHA’s seasoned management team to build a broader business in private markets by combining their specialty in alternative credit with our global scale.” – CIO of T. Rowe Price

In addition, Morningstar sees TROW as being well-positioned to grow its AUM, given the strong performance track record of its funds. As such, they expect a respectable AUM growth rate with while maintaining a healthy operating margin in the 47-49% range (compared to 48.4% op margin over the trailing 12 months), as highlighted in the recent analyst report:

“We also believe T. Rowe Price is uniquely positioned among the firms we cover (as well as the broader universe of active asset managers) to pick up business in the retail-advised channel, given the solid long-term performance of its funds and reasonableness of its fees, exemplified by deals the past several years with Fidelity Investments’ FundsNetwork and Schwab’s Mutual Fund OneSource platform. With the company likely to generate mid- to high-single-digit AUM growth on average going forward (aided by 0%-2% annual organic growth), we see top-line growth expanding at a 7.5% CAGR during 2021-25, with operating margins of 47%-49% on average.” – Morningstar

It’s also worth noting that TROW is uniquely well-positioned for shareholder returns, as it carries no debt on its balance sheet, and has $7.3 billion in total liquidity. This enables more capital for shareholder returns. In the first nine months of last year, TROW repurchased 2.9 million shares, representing 1.3% of the outstanding float.

Additionally, the recent share price weakness has pushed TROW’s dividend yield to 2.5%. While it’s not as high as that of other financial firms, it is double the 1.23% yield of the S&P 500 (SPY). It also comes with a safe 34% payout ratio and a 15% 5-year dividend CAGR.

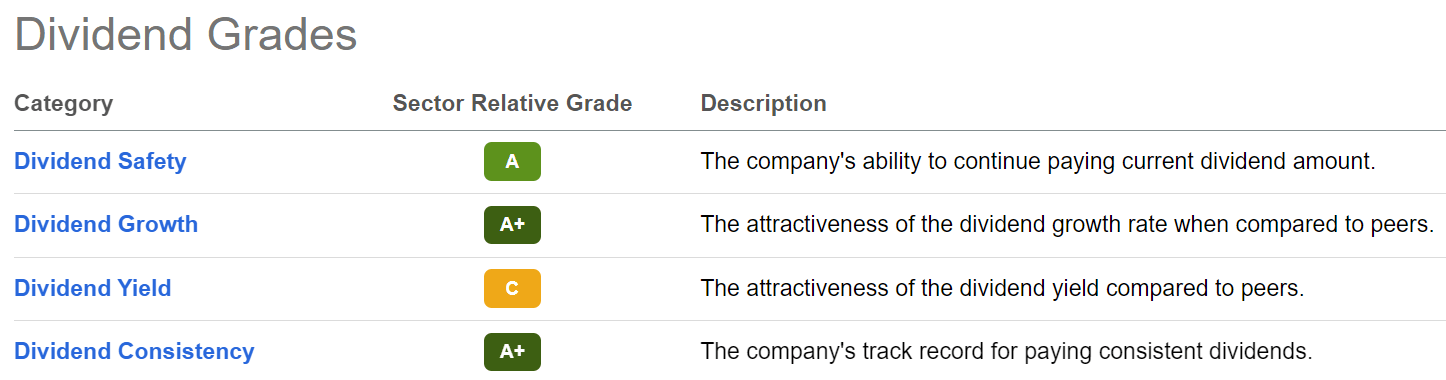

Notably, TROW is a dividend aristocrat with 35 years of consecutive annual raises. As shown below, TROW scores A/A+ grades for dividend safety, growth, and consistency.

TROW Dividend Ratings

Seeking Alpha

Risks to TROW include competition from passively managed index funds from the likes of BlackRock (BLK). In addition, the recent acquisition of OHA comes with merger integration risk. Lastly, market volatility can result in fluctuations in TROW’s AUM value.

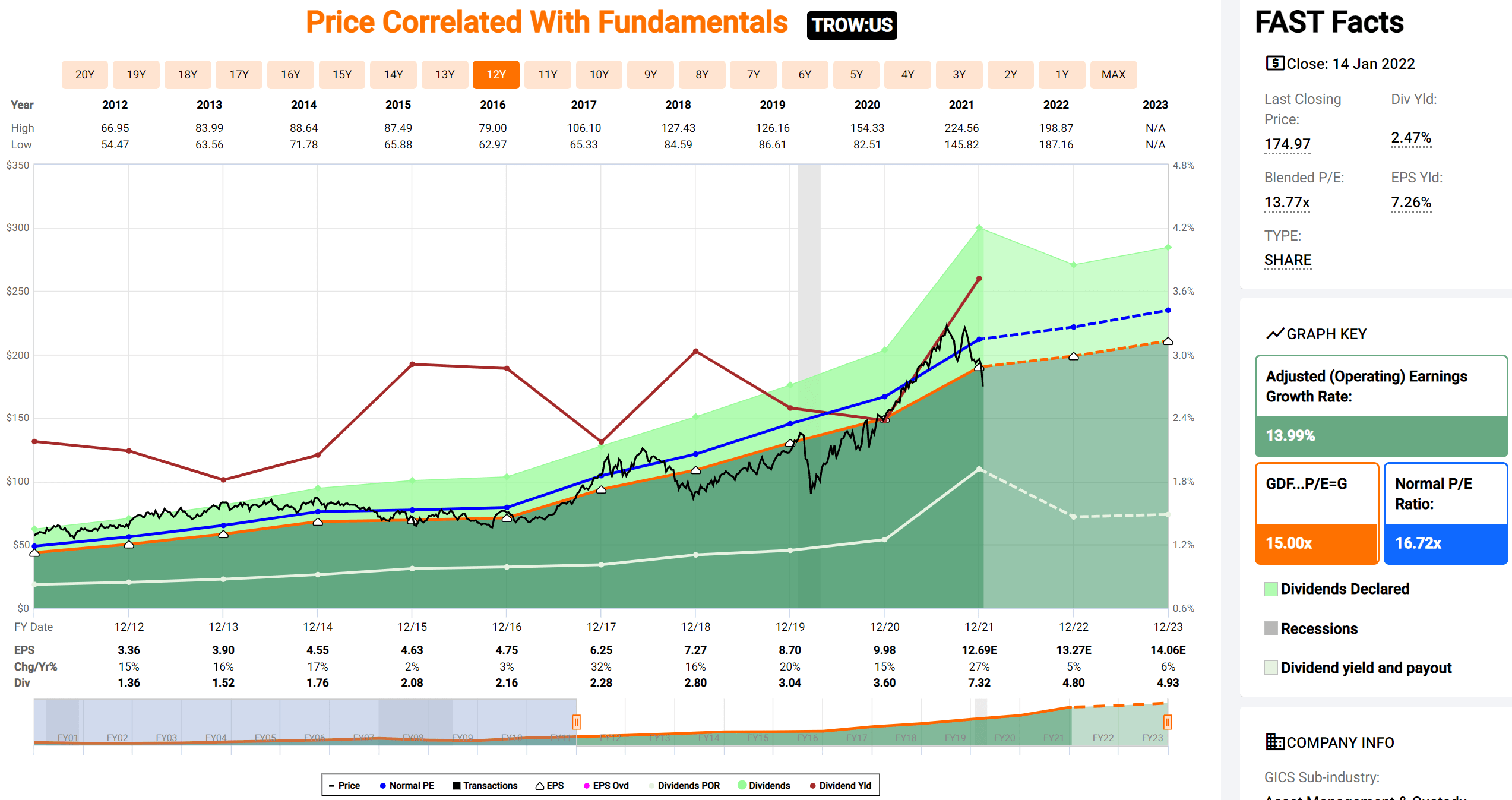

I see value in TROW considering all the above at the current price of $174.97 with a forward PE of 13.8, sitting below its normal PE of 16.7 over the past decade. Analysts estimate 12.1% EPS growth this year, and have an average price target of $202, implying a potential one-year 18% total return including dividends. Lastly, Morningstar has a $212 fair value estimate.

TROW Valuation Chart

FAST Graphs

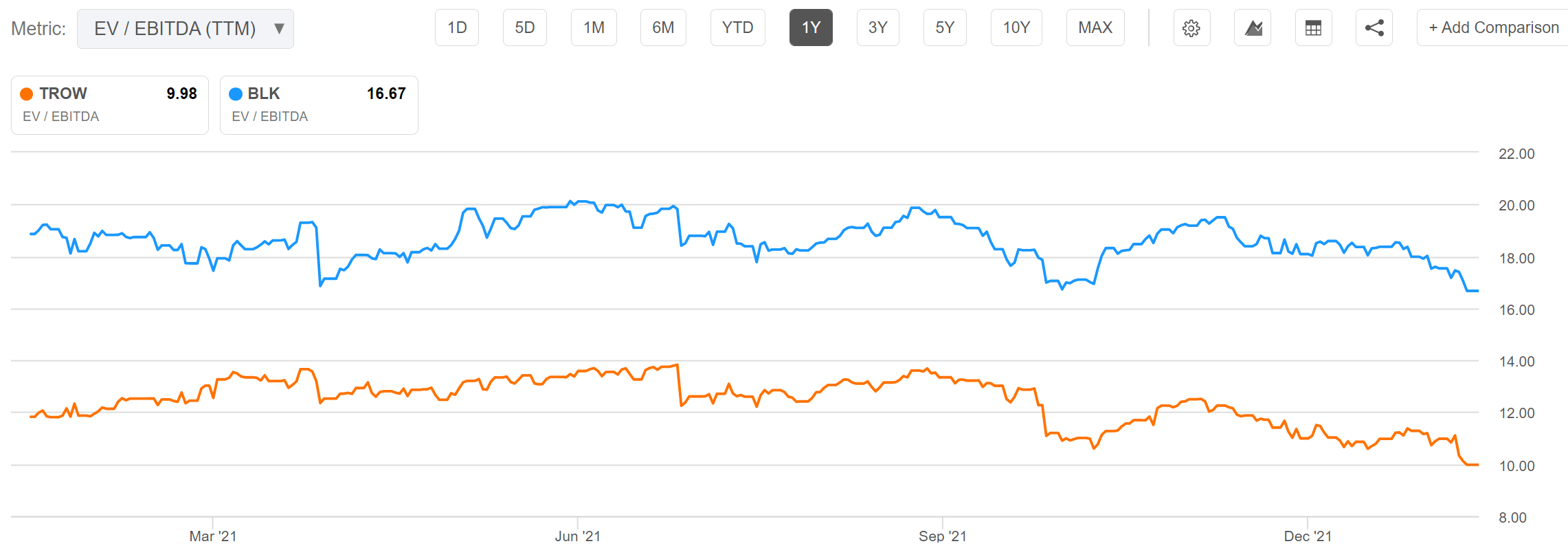

Plus, as seen below, TROW trades at a material discount to the passive investment management leader, BlackRock, as reflected by its EV/EBITDA of 9.98 as opposed to BLK’s 16.67. This is despite analysts expecting the same 12.1% EPS growth rate for BLK in 2022.

TROW and BLK Valuation

Seeking Alpha

Investor Takeaway

T. Rowe Price is a well-regarded asset manager and is often viewed as being a leader in the actively-managed investment space. It’s demonstrating robust AUM growth, and is well-positioned for industry consolidation with its strong liquidity, and it carries no debt on the balance sheet.

Meanwhile, TROW continues its track record of shareholder returns with buybacks and dividend hikes. I see value in TROW, especially after the recent material price weakness.