A week or so ago, I wrote an article in which I suggested that investors look “up” the supply chain when considering an investment directly in their line of sight. I argued that a key supplier may offer clues as to how a downstream company will perform, as I believe is the case with R.R. Donnelley (RRD) and Iron Mountain (IRM).

As a corollary to this idea (or vice versa), if a debate is raging over whether this company or that is best positioned to survive and thrive a major transformation – and you head, like mine, is spinning – it may be best to invest in major suppliers to all competitors.

Two Auto Companies

For many, this is what we face in the race toward renewable energy and the conversion from internal combustion engines, ICE, to battery electric vehicles, BEVs. To frame this article, I will focus on only two automobile manufacturers in which I am NOT invested (for the time being?) – Tesla (TSLA) and Volkswagen/Audi (OTCPK:VWAGY).

To be sure, the German giant is slow off the green flag with BEVs. They have announced that their last ICE vehicles will “appear” in 2026 but apparently be produced until 2040; it isn’t entirely clear. It is worth remembering though that VW is #1 globally in unit sales. Moreover, it is extremely solid financially, second only worldwide to Toyota (TM), IMO.

Tesla, on the other hand commands a substantial lead as the largest Western manufacturer in the fast growing BEV market. But here we have a company that has been unable to reliably bring its top line through its P&L and onto its balance sheet where the company is over-leveraged, and lacks liquidity. Moreover, turnover at the top is troubling. I’ve known a lot of frustrated general counsels over the years, but I’ve never heard of a company cycling through three of them in a year, not to mention all the other execs who have come and gone. And, if this doesn’t give you vertigo, how about in a two-day period last week when one analyst raised TSLA’s target by $100, while another lowered it 40%? The room is turning.

Tesla, dominant in BEV’s, poorly positioned financially; VW, dominant overall, strong financially, poorly positioned in BEV’s.

| Latest Full Year | VW/Audi | Tesla |

| Summary | #1 Globally, in Autos | #1 Globally, in BEV’s |

| Revenue | $278.2B | $21.5B |

| Gross Income | $56.1B | $4.0B |

| Operating Inc. | $23.5B | $-252.8M |

| Net Income | $14.0B | $-976.1M |

| Op. Cash Flow | $8.6B | $2.1B |

| Net Change in Cash | $12.1B | $334.1M |

| Liabs./Equity | 3.6x | 4.8x |

| Current Ratio | 1.1x | 0.8x |

| Dividend Yield | 2.8% | – |

If you’re looking for broader, deeper, reinforcing, and contradictory perspectives on the BEV race, I commend you to some fine contributors here on SA including Keith Williams, Montana Skeptic, The European View, and DoctoRX. I pay close attention to what they have to say even though we have some differences of opinion.

Two Nickel Miners

As I strive to gain control over my dizziness about car companies, I’ve invested elsewhere on the supply chain, specifically, in a few mining companies whose metals are essential to all BEV manufacturers.

I’m talking about cobalt, nickel, and manganese critical to the fabrication of lithium-ion batteries. Why not lithium itself? Because it’s not mined but, rather, “produced.” And, with no intent of trivializing the metal’s importance, it is relatively easy to obtain, provided you have access to dried up salt basins known as “salars” found throughout the world. To be sure, there will be A LOT of BEV demand for lithium. However, its supply is not overly constrained, meaning that the attractiveness for me, as an investor, is not as high as with these other metals, where a few miners control most of the supply; I’m partial to oligopolists. For the names of two additional SA authors who can expand on what I’m about to say, I refer you to Matt Bohlsen and Laurentian Research. They rate rare “follows” from me.

Again, because the primary purpose of this article is to explore supply chain investing, let’s focus on just nickel. If you’re looking for a non-SA article that reinforces my perspective, look at this one dating back to August that appeared in Bloomberg, “There’s One Metal Worrying Tesla and EV Battery Suppliers.” A few highlights:

- Demand for nickel for lithium-ion batteries is forecast to surge about 16 times to 1.8 million tons of contained metal by 2030, BNEF said in a July report. Batteries will account for more than half of demand for class one nickel by that date, shifting a market that’s currently focused on stainless steel.

- According to Peter Bradford, chief executive officer of nickel producer Independence Group NL [note potential bias], “The big question everyone will be asking in a year’s time is where does the nickel come from to satisfy the demands for nickel in stainless steel, as well as the increasing demand for nickel into electric vehicle batteries?’’

- He went on to say that, “The dramatic price rise we’ve seen will pale into insignificance compared to the future.”

Two sources of volume nickel are worth considering. First, Russian public joint stock company, Norilsk (OTCPK:NILSY), the world’s #2 producer of nickel. I’m avoiding #1, Vale (VALE), for now because I don’t want their exposure to iron ore, but I do like that Norilsk is also a major producer of palladium necessary for cleaner-running ICE vehicles. Forewarned is forearmed – Norilsk has already said that in the 2023-2025 timeframe it will reduce its dividend to fund mine development and emissions abatement initiatives. The company has been transparent and, frankly, the dividend is too high given the collection of stakeholders it must serve. Nevertheless, the stock pulled back somewhat following this pre-announcement, only to resume its upward trajectory. I, for one, am undeterred.

Madagascar’s Ambatovy is reported to be (one of?) the largest lateritic – long, shallow, and lower grade – nickel mine(s) on earth with production capacity of 60,000 tons (132.2 million pounds) annually (and 5,600 tons, 12.3 million pounds, of cobalt also essential to electrification). The Ambatovy joint venture is owned 47% by Sumitomo Metals (OTCPK:SMMYY), the mining arm of one of Japan’s keiretsu. On the supply-side, Sumitomo Metals is also well established in Indonesia, another major source of nickel. And, on the demand-side, the company has deep connections to Panasonic that will be the/a principal battery supplier to Toyota as Tesla moves into battery production on its own. Elon Musk is reported to also be considering getting into nickel mining, an indication that he is concerned about sourcing the metal.

| Latest Full Year | Norilsk Nickel | Sumitomo Metals |

| Summary | #2 Nickel Miner | #1 Lateric Mine (47%) |

| Revenue | $11.6B | $8.2B |

| Gross Income | $6.4B | $1.1B |

| Operating Inc. | $5.4B | $697.1M |

| Net Income | $3.0B | $805.9M |

| Op. Cash Flow | $6.0B | $1.0B |

| Net Change in Cash | $332.3M | $-510.9M |

| Liabs./Equity | 3.7x | 0.6x |

| Current Ratio | 1.9x | 2.2x |

| Dividend Yield | 9.4% (cut coming) | 1.3x |

As is true whenever tectonic stresses build between supply and demand, historical numbers can become instantly meaningless when things shift. Nevertheless, to provide some foundation for demonstrating what we may be about to witness, I offer these year-over-year productivity statistics, courtesy of CNN Business, for Norilsk only. This is the stuff of alpha:

- Growth in Net Revenue [NR]: Norilsk +26%

- Growth in Gross Inc. as a % of NR: Norilsk from 50% to 55%

- Growth in Op. Inc. as a % of NR: Norilsk from 40% to 47%

- Growth in Net Inc. as a % of NR: Norilsk from 24% to 26%

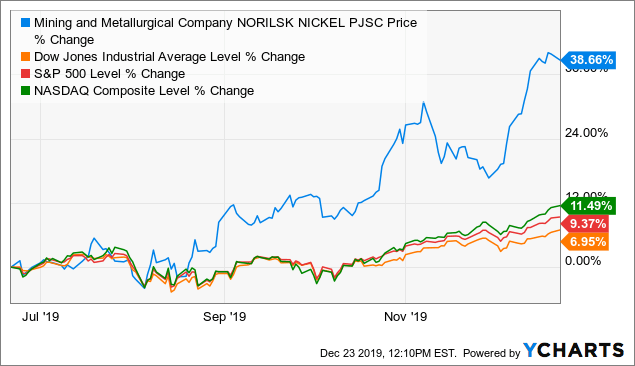

I first mentioned that I bought a half-position in NILSY in an 06/24/2019 comment to my own article that SA published five days earlier on 06/19/2019. From those date stamps, Norilsk hit my radar fully six weeks before Bloomberg’s article referenced above. Consistent with my supply-chain hypothesis, NILSY has outperformed the Dow, the S&P, and the NASDAQ since; alpha.

Data by YCharts

Data by YChartsI’ve never mentioned Sumitomo Metals in any article before today so it’s too early to report on the progress on SMMYY. However, the company’s year-over-year growth statistics are decidedly negative. Nevertheless, as of a couple of weeks ago, I’m long the ADR’s against the belief that Sumitomo Metals is stalled off bottom, waiting for BEV metal demand to accelerate. That’s the bet and, like everything else in investment land, it is no sure thing.

A Word About Sovereign Risk

Investopedia defines “Sovereign Credit Rating” as “an independent assessment of the creditworthiness of a country or sovereign entity. Sovereign credit ratings can give investors insights into the level of risk associated with investing in the debt [and equity] of a particular country, including any political risk.” Russia is in B territory and Madagascar is unrated, not exactly confidence-inspiring.

However, I am not particularly concerned about poor sovereign risk scores when it comes to the import/export of critical commodities. My opinion grows out of the trade finance I did during the last days of the Iron Curtain before the Berlin wall came down in 1989 and the USSR fell apart two years later.

Those were suspicious and poor times. I recall meetings with the foreign trade bank of the Soviet Union, where KGB agents introduced themselves and sat with us bankers as we went about our business. For a little hard currency that their handlers could spend at the Western store, children sold Lenin and Soyuz pins in Red Square. Very tough.

But, times were even worse in the USSR’s satellite, East Germany. With sadness, I crossed Checkpoint Charlie once or twice each year to discuss trade finance with the Deutsch Aussenhandelsbank, which served a lunch of charged water, dry toast, and lard. I left, through heavy security, sitting at times alone in windowless rooms at the station, listening to soulful whistles, before boarding the train and riding it back to the West more-or-less by myself.

Still, I did good business in the Comecon including with Poland, Czechoslovakia, Romania, and even Bulgaria. State borrowers always met their obligations because the import/export of commodities represented their economic lifeblood such as it was. Nickel rates this distinction today for Russia, which is looking for economic drivers beyond oil and gas, and Madagascar’s Ambatovy mine(s) contributes about 14% to that country’s exports. These countries will not trifle with those who support the monetization of their assets, in my opinion.

And, A Word About Pollution

Which brings me to the issue of environmental destruction. Heavy metal mining is filthy, destroying the land and compromising the lives of those who extract the ore or live nearby. The town of Norilsk, Russia makes Time magazine’s list of the worlds’ ten most polluted places, right up there with Chernobyl. I can imagine that Ambatovy, Madagascar is not far behind. Unfortunately, there are trade-offs to be made. For the time being – we view heavy metal mining as a medium-term proposition. We will invest in local/regional supply chain activities provided broader/global benefits result and until cleaner options come along.

And, speaking of cleaner alternatives, we are investing even farther out on parallel supply chains. For example, we have three smaller positions in hydrogen fuel cell companies. These include Ballard (BLDP), FuelCell (FCEL), and Plug Power (PLUG), the first of which we’re up 149% in eighteen months or so, and the last two, beyond risky; no place for investors who are not prepared to lose it all. Something tells me that big oil will not allow itself to be rolled over by BEVs when natural gas can be “made” into hydrogen fuel.

Finally, I’ll mention perennial disappointment, IBM (IBM). As this article was taking shape in my head, Big Blue announced a partnership with Daimler Benz (OTCPK:DMLRY) to develop a new battery – with elements sourced from seawater – that could eliminate the need for heavy metals in batteries. Clearly, this represents a longer-term investment opportunity but imagine that; very exciting.

Supply Chain Investing

So, there you have it, an illustrative two-car BEV race as a way of introducing a discussion of supply-chain investing in two nickel miners. Will Tesla, VW, or another automobile company prevail? The truth be told, no one knows yet; for the time being our money is on Toyota and Suzuki (OTCPK:SZKMY).

We are invested in other miners as well, including Anglo-American Platinum (OTCPK:ANGPY) (platinum and palladium), Glencore (OTCPK:GLNCY) (cobalt), South32 (OTCPK:SOUHY) (manganese). Some of these investments have done very well, others not (yet?).

The transformation to electric vehicles is coming fast but the race is a long one; the Indy 500. Whichever auto companies ultimately close on the checkered flag, all BEV contenders will need heavy metal until scientists and business folks identify and deliver cleaner, sustainable, solutions. We’re invested all along the demand-supply chain spectrum but more so on the supply-side.

Disclosure: I am/we are long NILSY, SMMYY, TM, SZKMY, IBM, ANGPY, SOUHY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Always do your own due diligence in consultation with a licensed and competent financial adviser who understands your unique needs and puts your interests ahead of their own. Remember, there are added considerations in owning foreign securities including those associated with ADR sponsorship, buying and selling the pinks, foreign withholding taxes on dividends, and fees. (All my proceeds from contributing to SA go to charity.)

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.