Suburban Propane Partners (NYSE:SPH), an MLP, offers real value at low risk. The current yield exceeds 22% (or 15% on an estimated distribution cut, which may not occur). Propane demand is primarily for household heating, which should hold up during the current crisis. Also, most sales occur during the winter months. Therefore, even if the spring and summer months prove slow, SPH will see less impact because far less fuel sales occur in those months due to less need for fuel in warmer months. Therefore, SPH offers a relatively low-risk way to obtain a high distribution.

Business Overview

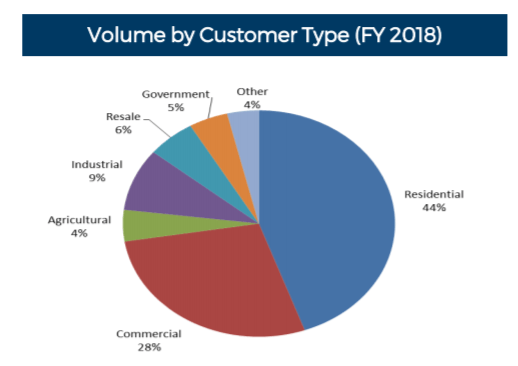

SPH supplies propane by truck to residential and commercial customers in broad sections of the U.S. The company is based in New Jersey and has a 90-year operating history. It frequently does bolt-on acquisitions to expand its footprint and has about 5% share of the U.S. propane market and ancillary services. The company is structured as a Master Limited Partnership (MLP).

Source: SPH Investor Presentation

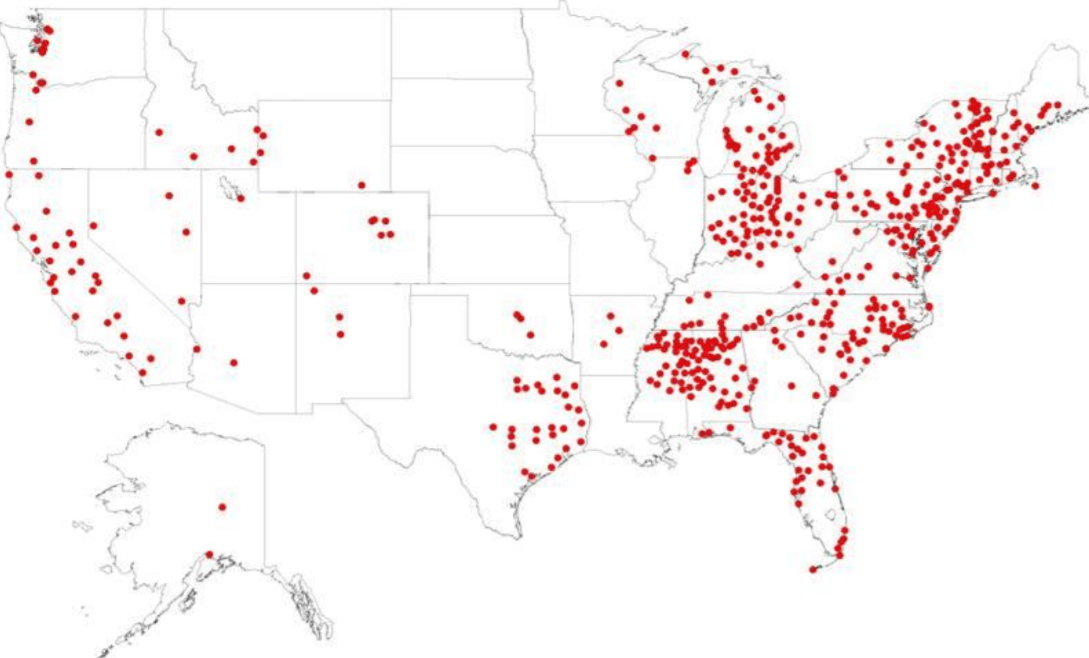

Operating Footprint

Source: Suburban Propane Investor Presentation

What Are The Risks?

Typically when you see a 22% yield, you want to ask what are the risks? Let’s work through them:

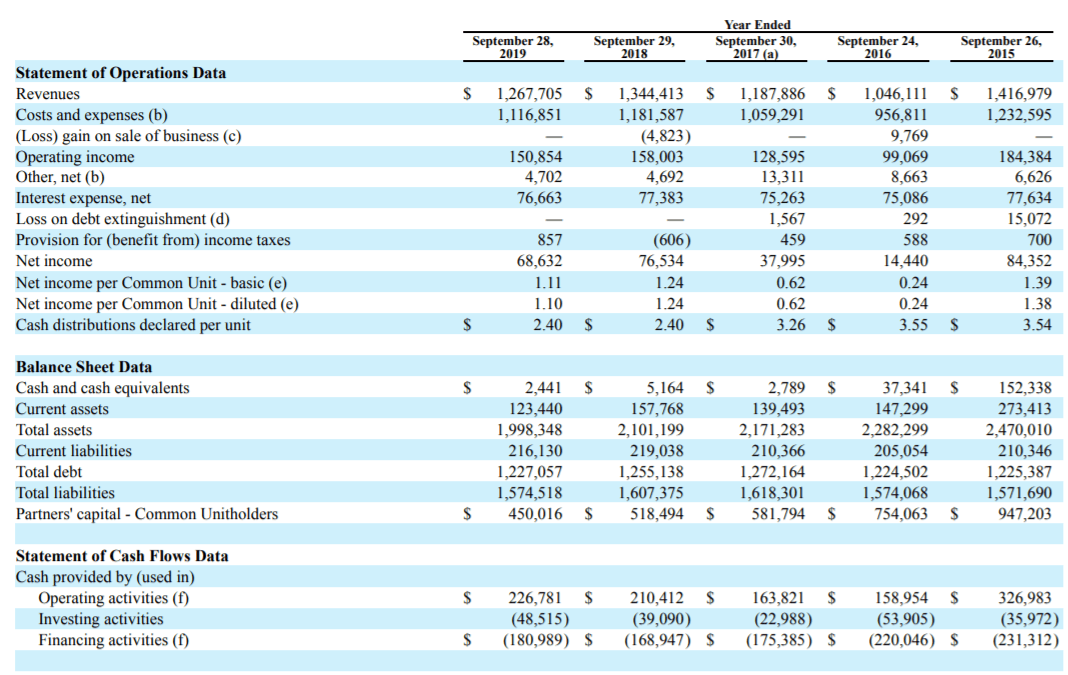

- Warm 2019/20 winter – This winter has been 9% warmer than average at the time of writing. Warmer winters mean less need for heating and hence lower demand for propane. However, SPH has seen warm winters before such as, most recently, in 2016. Though net income does decline in these years, cash flow generation remains strong because depreciation typically exceeds capex by over $100M annually, meaning net income typically materially understates free cash flow.

Source: SPH 10-K

- Coronavirus disruption – Virus-related disruption is less of a concern for SPH. Propane for heating is an essential service and roughly 80% of heating degree days occur November-March. As a result, if there are further U.S. quarantine and lockdown measures leading to economic decline over the coming weeks and months, SPH will be less impacted. It can be considered an essential service because people need to heat their homes. Currently SPH has closed some walk-in locations, but continues to deliver to customers.

- Global warming – As temperatures increase demand for propane may progressively decline. Though this is likely to be a slow and uneven process. If the world warms at 0.3 degrees Fahrenheit per decade, then that reduces heating demand by about 0.1% a year. Hence global warming is a slight drag over time, not a material one.

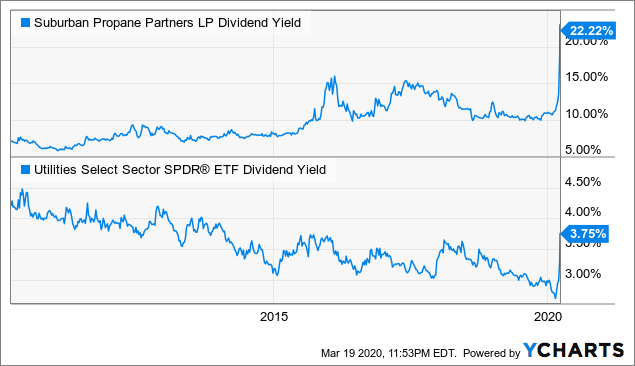

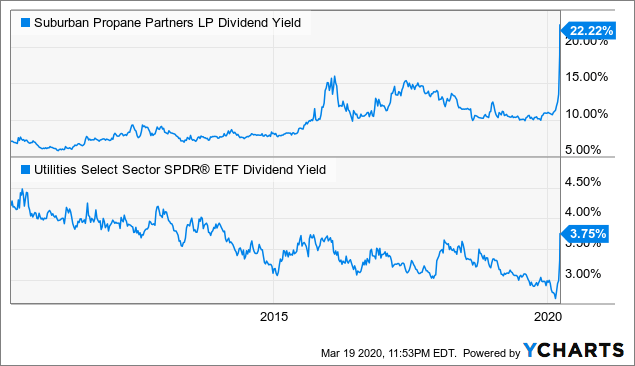

- Distribution cut – A final risk is that the distribution gets cut. This is a real risk, but the distribution is still attractive even after an estimated reduction. SPH has 62M units outstanding and therefore the $0.60 quarterly distribution costs $148M annually. If 2020 proves to be a soft year such as 2016 (as seems likely on current temperature data), then the distribution would be only 1.02x covered by operating cash flow (see forecasts below). That may prove insufficient. However, assume $100M is a sustainable distribution level, creating 1.5x coverage even on a seasonally warm weather year such as 2020. That creates a $1.6/unit annual distribution or a 15% yield on the current price. That’s still attractive, and remember we’re baking in a distribution cut that has not happened, and possibly may not. Below we compare SPH’s distribution yield to a popular U.S. Utility ETF as a benchmark. SPH’s distribution is clearly elevated relative to its own history and peers. Peers have spiked recently too, but the reaction seems disproportionate.

Data by YCharts

Data by YCharts

Q1 Earnings And 2020 Forecasts

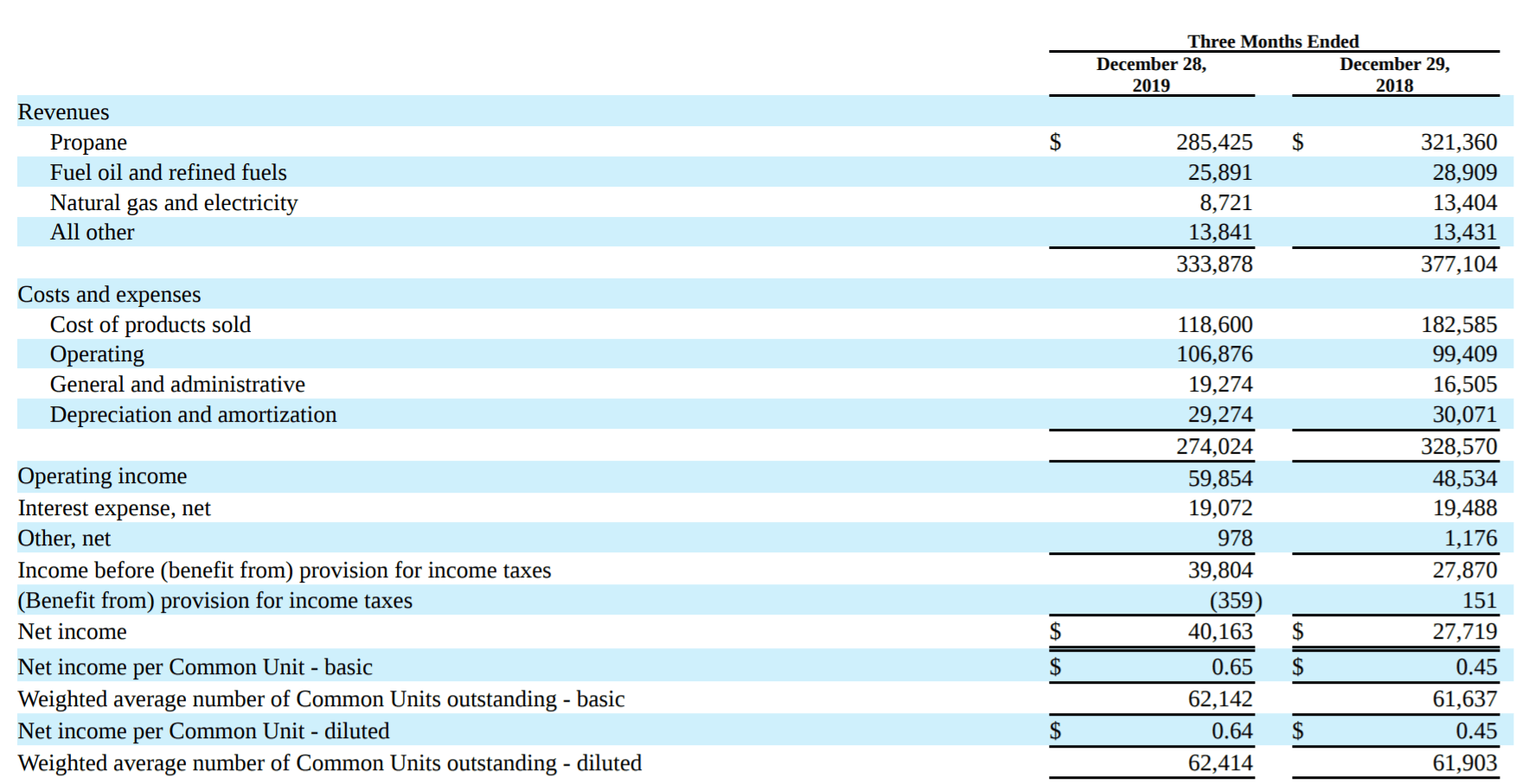

Despite a relatively warm winter, Q1 earnings which cover October-December 2019 saw an improvement over the prior year with $0.64 net income per unit compared to $0.45 the prior year.

source: SPH 10-Q

2020 Forecasts

| Q1 actual | Q2 est. | Q3 est. | Q4 est. |

| $0.64 | $1.50 | -$0.50 | -$0.80 |

- Total net income per unit fiscal 2020 (est.): $0.84

- Impact of depreciation of $120M (est.) exceeding capex of $20M (est.): $1.61

- Adjusted free cash flow per unit 2020 (est.) = $0.84 + $1.61 = $2.45

- Current annual distribution per unit = $2.4 (implied coverage 1.02)

Summary

In an unusually warm year, SPH’s distribution coverage will be tight. However, the yield exceeds 22%. The company may choose to sustain a year of low coverage in seasonally warm weather. However, it may also cut to a far more conservative level of, say, an annual $1.6 distribution per unit. That would be 1.5x covered on my estimates and carry a 15% yield. This is good business given the network effects in propane distribution, and low economic risk in this environment given fuel usage is less cyclical.

It appears a heads you win, tails you win setup. Either it maintain a 22% yield for material upside, or it cuts to around a 15% yield with 1.5x coverage which is 3x most peers. Either way, the underlying business is solid, and there is potential for greater income and maybe price appreciation here. 2020 won’t be a great weather year, but the market has more than discounted it already.

Disclosure: I am/we are long SPH. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.