Thesis

SilverCrest Metals (NYSEMKT:SILV) is currently trading near the higher end of its 52-week price range, and the stock is also way above its 200-day EMA (read: Exponential Moving Average) which raises concerns about the stock’s current valuation. This view is further reinforced when we consider SILV’s price-to-book valuation in comparison with peer miners (those engaged in exploration/ development of primary silver projects).

This calls for an analysis of SILV’s expected ‘after-tax NPV’ (based on management’s latest estimate) to be derived from its flagship asset namely, LC (read: Las Chispas) in relation to the company’s current market cap to check if the stock appears overvalued. The fact that LC’s ‘Base-Case’ after-tax NPV is ~$406 MM compared with SILV’s current market cap of $1.15 BB initially indicates that the company might be overvalued, and investors could consider taking some profit at these rates. Well, that could be an appropriate approach for some investors.

However, our discussion on the company’s valuation will highlight that the stock is not overvalued despite its recent strong price performance. I believe there’s significant room for SILV’s share price growth over the next 3-5 years by which time the LC mine would have become fully operational. The focus of this article’s discussion would be the company’s valuation. However, our discussion on SILV’s valuation does not take into account the price gains that may accrue from a tentative offer for acquisition of SILV, nor does it incorporate the impact of possible future dividends originating from LC’s future FCFs (read: Free Cash Flows). Let’s get into the details.

Figure-1 (Source: Mining.com)

Valuation

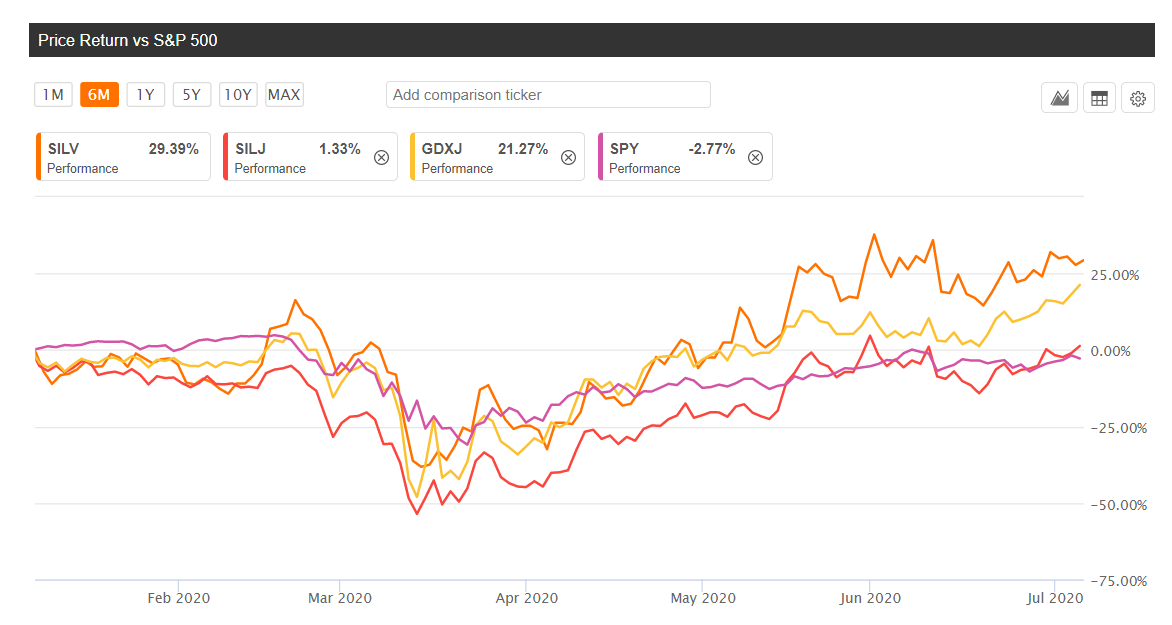

SILV beat the market returns during the initial phase of COVID-19

As a matter of fact, SILV significantly outperformed the 6-month price performance of 3 benchmark indices (which I think, are somehow relatable to the company). The selected indices include:

- ETFMG Prime Junior Silver Miners ETF (SILJ) – where SILV is one of the top holdings, and ranks among the ETF’s top 5 performers year-to-date;

- VanEck Vectors Junior Gold Miners ETF (GDXJ) – where SILV is relatively a new entrant with <1% ETF holding; and

- S&P 500 – where SILV is not a constituent, and the ETF is included to gauge SILV’s price performance versus the broader stock market.

Figure 2 highlights the resilience of SILV’s business model during the initial phase of COVID-19 (from January 2020 to date) in terms of its ability to outperform the benchmark indices. It highlights that, unlike the silver benchmark ETF that posted minimal returns (same case with S&P 500, though GDXJ is an exception) despite the sharp hike in YTD silver prices, SilverCrest managed to stay ahead of the competition.

Figure-2 (Source: Seeking Alpha Premium)

Figure-2 (Source: Seeking Alpha Premium)

An apparently high valuation

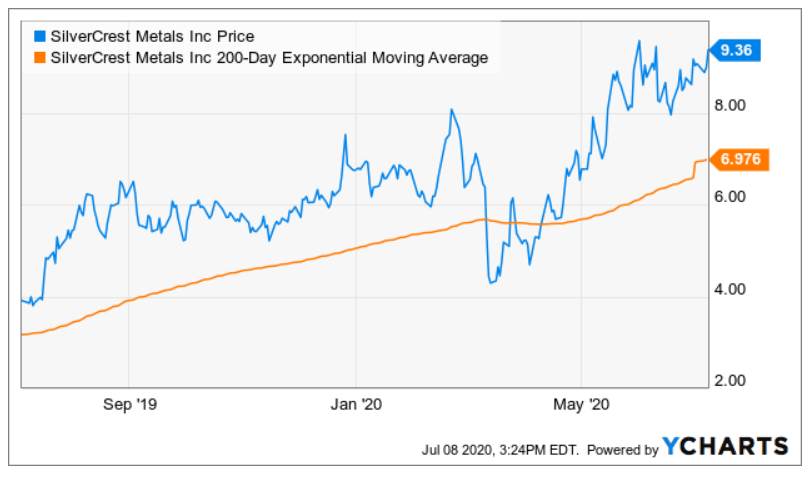

Unsurprisingly, SILV’s current prices (at $9.36, at the time of writing) are also significantly higher than its 200-day EMA (read: Exponential Moving Average) of ~$7 (Figure-3) and gives the notion of SILV’s apparent overvaluation.

Figure-3 (Source: YCharts)

Figure-3 (Source: YCharts)

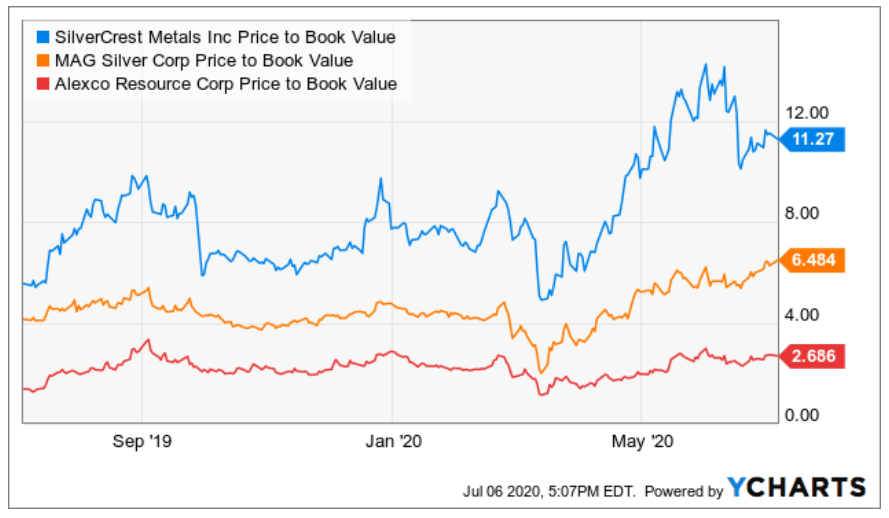

Now, let’s check SILV’s price-to-book ratio compared with peers. Apart from SILV, my selected peer group includes MAG Silver (NYSEMKT:MAG) and Alexco Resource Corp. (NYSEMKT:AXU). Note that both SILV and MAG have their flagship assets located in Mexico, whereas AXU’s key project is located in Canada (the location tells us something about the jurisdictional risk; check pt.6 in the ‘Assumptions and Risks’ discussion presented later in the article). The reason for selecting these 3 companies is that their flagship mining assets are scheduled for production in the near term (say, between 1 and 3 years). Figure-4 shows that SILV’s PB valuation is in fact the highest among peers, implying that the market is anticipating strong future growth in SILV following the recent momentum in silver prices.

Figure-4 (Source: YCharts)

Figure-4 (Source: YCharts)

[Author’s Note: Since these companies do not currently generate any revenues/earnings, I haven’t considered other traditional valuation metrics like the P/E ratio or the EV/EBITDA ratio.]

Is SilverCrest overvalued?

I don’t think so; and I’ll explain the reasons for my views. To start with, I’ll pick SILV’s after-tax NPV (expected from its LC property). As per SILV’s May 2019 PEA (read: Preliminary Economic Assessment), Las Chispas is expected to generate ~$406 MM in after-tax NPV, with a project IRR of 78%. Of course, this NPV estimate takes into account a silver price environment of ~$16.68/oz (Figure-5) during the project’s 8.5 years LoM (read: Life of Mine). The $406 MM NPV does not justify the stock’s current market cap of $1.15 BB, and this is why I think SILV’s valuation needs to be double-checked. In other words, the current market cap is ~2.8 times [$1,150 MM ÷ $406 MM] the project’s ‘Base Case’ NPV.

Figure-5 (Source: Latest Presentation, June 2020-pg.8)

Figure-5 (Source: Latest Presentation, June 2020-pg.8)

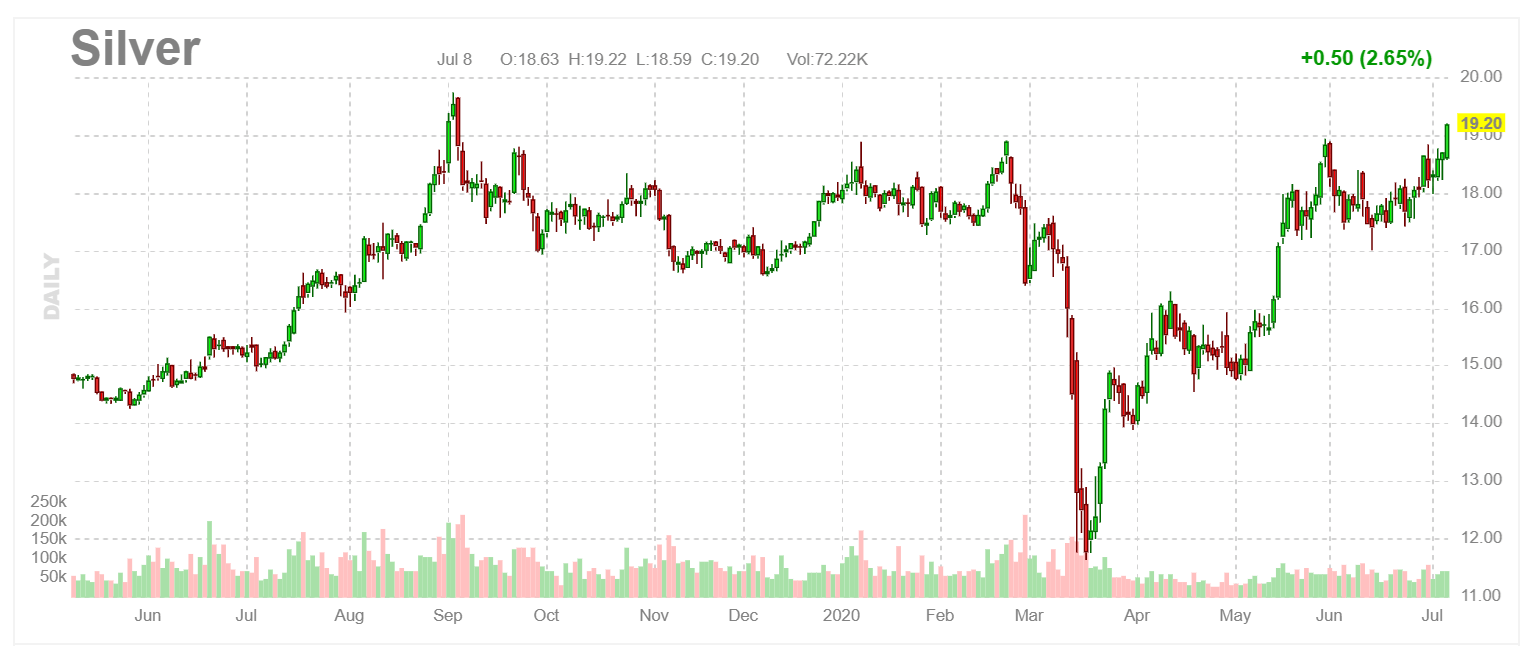

However, the ‘Upside’ case presented above assumes LoM silver and gold prices at $1,450/oz and $19/oz. At the time of writing, silver prices had already breached the $19/oz mark and were trading at $19.20/oz (Figure-6); posing a strong and sustained rally above their mid-March lows of ~$11.80/oz. Note that gold prices are ~$1,819/oz (at the time of writing). This situation reveals that SILV has significantly breached the gold target price for its ‘Upside’ scenario and has also breached the silver target price, though marginally. I’d assume that, given the gold-silver ratio of ~100x, the project’s ‘Upside’ NPV of $507 MM could be expected to be achieved, thus lowering the differential between current market cap and project NPV from ~2.8 times (discussed earlier) to ~2.27 times [$1,150 MM ÷ $506.5 MM]. Well, SilverCrest still seems overvalued based on a comparison of its market cap with the LC project’s NPV, right? Wrong.

Figure-6 (Source: Finviz)

Figure-6 (Source: Finviz)

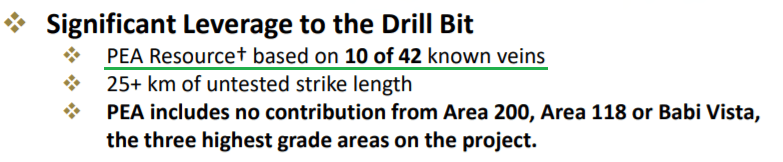

LC’s February 2019 resource estimate highlights a total of ~108 MM AgEq (read: silver equivalent) ounces in ‘Indicated’ and ‘Inferred’ resource categories (Figure-7). SILV’s LC property has 42 discovered mining veins, and the management has issued the 2019 resource estimate based on only 10 out of those 42 veins (Figure-8).

Figure-7 (Source: SILV’s Mineral Resource estimates)

Figure-7 (Source: SILV’s Mineral Resource estimates)

Figure-8 (Source: Latest Presentation, June 2020-pg.5)

Figure-8 (Source: Latest Presentation, June 2020-pg.5)

Simply put, if resource located in 10 veins is expected to generate an NPV of >$500 MM (in the current gold/silver price environment), then resource located in total 42 discovered veins can be expected to generate approximately ~$2 BB in after-tax NPV. Based on the current market cap of ~$1.15 BB, this would entail a gain of ~76% from the current prices (or a long-term target price of ~$16.50). However, I believe that the journey to such price target would not be a smooth one. In my view, there are certain key assumptions and risks that could impact the project’s after-tax NPV and consequently, the achievement of this price estimate. So, let’s take a look.

Assumptions and risks

- Resource from the existing 10 veins will hit (or be close to) management’s PEA estimates.

- Resource from remaining 32 veins will be proportionate (in size) with the expected resource from the existing 10 veins. Discovery of additional mining veins would upscale the project’s NPV.

- Silver prices will be able to retain their current strength. On that note, the >$500 MM NPV takes into account silver price of $19/oz. In my view, considering the global uncertainty associated with the COVID-19 outbreak, together with the planned significant infrastructure investments to support EV (read: Electric Vehicles) transformation, silver prices could be heading to $25/oz over the next 5 years (or earlier). This could push the project’s NPV beyond the current estimate of ~$2 BB.

- Project’s costs would be in line with management’s expectations. On that note, SILV expects the project’s AISC (read: All-In-Sustaining-Cost) during the initial 4 years to be under $5/AgEq oz, and ~$7.5/AgEq oz over the project’s initial LoM of 8.5 years. At current silver prices, SILV could generate a good $14/AgEq ounce margin.

- The project would not be flagged with delays. On that note, the LC property’s FS (read: Feasibility Study) was initially planned to be issued during H1 2020, but the timeline was stretched to Q4 2020 due to government-mandated operational suspension, in the wake of COVID-19 outbreak. However, this delay will enable SILV to add further drilling results in the FS to enhance the quality of the underlying resource.

- Project would remain essentially free from political risk, and the Mexican authorities would not create operational and financial hurdles in the progression of the project. I’d say the jurisdictional risk in Mexico has advanced from ‘mild’ to ‘moderate’. For instance, the recent tax dispute between existing Mexico-based silver producer First Majestic (AG), and the Mexican authorities gives the notion that Mexico is no more the safe-haven for silver miners, like it previously used to be.

- Grading will not be affected. Note that the current PEA incorporates average head grades of ~1,234 gpt (read: grams per ton) and ~581 gpt in ‘Indicated’ and ‘Inferred’ resources, respectively. While its normal to expect some deviation from the average grading, any future discoveries of large-scale, low-grade deposits would hit the project’s economics. However, I believe that currently this risk is less likely to materialize since the 2019 PEA does not take into account the underlying resource at LC’s three highest grade deposits namely Area 200, Area 118, and Babi Vista (refer to Figure-8 above).

- The PEA provides an initial resource indication, and a more accurate estimate would be uncovered when SILV issues the FS towards the end of the fiscal year. A higher/lower resource estimate in the FS could impact the project dynamics accordingly.

- A construction decision is expected to be made soon after the issuance of the FS (expected before YE 2020). In my view, any delay in construction decision (say, possibly due to an extended COVID-19 run, or COVID-19 cases appearing at the project site) would also hit the project’s economics.

A conservative price estimate

Considering the ~4x upside in project’s NPV accruing from expected additional resource in the remaining unexplored 32 veins, we could assume that even if LoM silver and gold prices remain at the ‘Base Case’ estimate of ~$16.68/oz and ~$1,269/oz (refer to Figure-5) for silver and gold prices, respectively, that is, a material downside to the present day PM (read: precious metals) prices, the project’s NPV would lie somewhere around $1.62 BB, leading to a target price of $13.22 [$1.62 BB (expected conservative NPV) ÷ $1.15 BB (current market cap) X $9.36 (current share price)].

In my view, if we apply a 15% risk margin (assumed) to the target price of $13.22 (to accommodate the impact of some of those risks discussed earlier), a very conservative price estimate would be $11.24, and that’ll record a gain of ~20% from SILV’s current price.

Valuation: Bottom line

To cut a long story short, SILV’s long-term price estimate varies between a conservative estimate (that takes into account ‘Base-Case’ silver/gold price estimates and applies an assumed 15% risk margin) of $11.24, and a slightly accommodative estimate of ~$16.50 (that takes into account the ‘Upside’ case silver/gold price estimates and applies a 0% risk margin).

In my view, SILV’s long-term price range will vary between these two prices; absent the impact of any price appreciation attributable to a potential takeover offer (discussed later) and any future dividends that SILV would be able to pay once it becomes fully operational (also discussed later).

A potential takeover target

Considering SILV’s significant growth potential, robust mining economics, and the stock’s defensive stance against a potentially challenging market (low CAPEX of ~$100 MM, low payback period between 7 and 9 months at current market prices, NPV to CAPEX ratio that varies between 4:1 and 5:1 based on the ‘Base-Case’ and ‘Upside-Case’, respectively, nil capital commitments etc.), it is fair to believe that the company is a potential takeover target. But what would be the timing of such an offer?

In my view, SILV might receive such an offer once it has issued the FS, and also announced a construction decision. At that point, mining giants (say, Rio Tinto (NYSE:RIO), or BHP (NYSE:BHP), who’d want to gain exposure to PMs, particularly silver) might consider acquiring the company, given the attraction of the PMs market. Alternately, an offer may be made after the construction decision is taken, and once the construction is nearing completion as this could tempt a potential acquirer to obtain a promising, de-risked project.

[Author’s Note: The discussion of any such tentative acquisition offer is merely to highlight the potential for share price gains based on SILV’s attraction as a takeover target, and is purely based on my opinion. It’s possible that SILV moves from project construction to operation (throughout the LoM) without being approached by any potential acquirer.]

Future Dividends

As mentioned above, LC’s payback period ranges from 7 to 9 months depending upon the prevailing PM prices, whereas the project’s initial LoM estimate is 8.5 years. This creates room for significant FCF generation. Given SILV’s robust liquidity worth >$160 MM (that is adequate to fund project’s expected initial CAPEX of ~$100 MM), I believe strong PM prices would enable SILV to pay sustainable dividends, going forward.

To put that into context, SILV expects to generate annual FCF of ~$115 MM during the initial 4 years of mine production, and these expectations are based on ‘Base-Case’ silver/gold prices. Since current silver/gold prices are actually breaching the ‘Upside-Case’ price forecast, the project’s FCFs could be stronger if the PM prices could sustain.

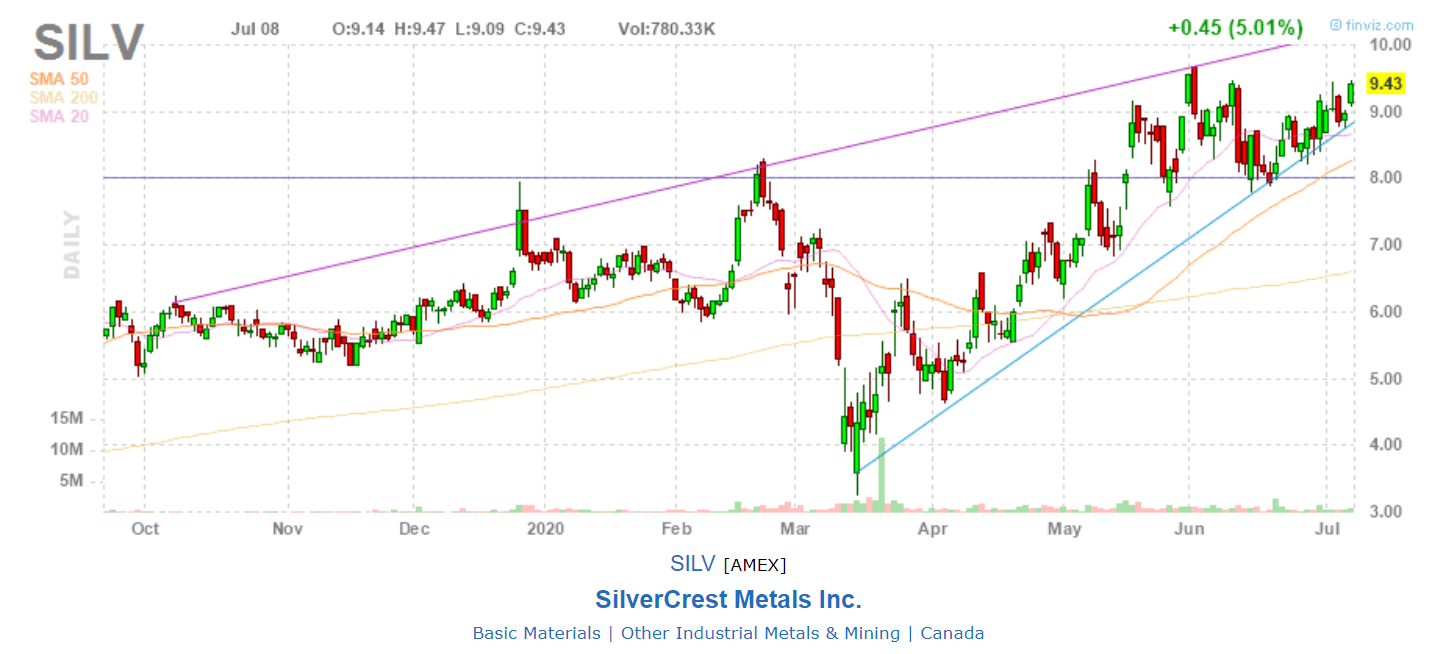

Technical Analysis and Investor Takeaway

At the time of writing, SILV last traded at $9.43 (and is about to breach its 52-week highs). Technically speaking, these prices could be considered risky and indicative of a profit-taking opportunity, but I believe it’s best to hold the stock at this point. Of course, considering these price levels, it won’t be a good idea to initiate a new position in the company unless you plan to go for a ‘long’ investment. That said, let’s check the stock’s technical chart (Figure-9).

Figure-9 (Source: Finviz)

Figure-9 (Source: Finviz)

The chart reveals that the resistance and support lines will join above $10. If silver retraces a few steps at or around $18.50/oz, then it’d make sense to take some profit. Until then, it’d be wise to follow silver’s lead to test how far this rally goes. While the momentum in silver is currently weighing down heavily on SILV’s price performance, the next significant catalyst would be the announcement of FS, and a construction decision later on. In my view, investors should keep a check at these two tailwinds to gauge SILV’s near-term price performance.

Despite the fact that SILV has a relatively higher PB ratio (in line with peers), I believe the stock has the potential for share price growth over the long term. This is explained by the tentative NPV gains from its Las Chispas project that significantly overshadow the company’s current market cap.

Author’s Note: This article was submitted on 8 July, 4:40 PM ET when silver price was ~19.15/oz and gold’s price was ~$1,819/oz. Given the volatility in PM prices, it’s possible that by the time the article is published, silver and gold prices might have marginally moved from the reference prices used in the article. Readers should note that the crux of the article is to highlight a valuation gap based on the project’s NPV and the company’s current market cap, rather than to highlight a momentum trading opportunity based on the PM rally. Thank you for reading.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.