JHVEPhoto/iStock Editorial via Getty Images

The recent discussions on Shopify (SHOP) have been fascinating to me. The stock seems to be turning into a battleground position come up with those convinced that it is heading a lot lower and others convinced it is now a fantastic buy.

I find myself in a middle-ground position as someone who has long admired the business but hasn’t been comfortable touching it for much of the last couple of years. That has now changed as I have started to scale into the business. I have now accumulated a reasonable position in Shopify, to add more should it continue to fall.

As a disclaimer, I come to the Shopify position as an investor that buys platform technology businesses and lets them sit for years. Shopify has been one such business that I have long admired and have wished to add to alongside my positions in Atlassian (TEAM), HubSpot (HUBS), Amazon (AMZN), MercadoLibre (MELI), and Sea (SE), also long-term holdings.

Still, I could never do so at a price that I liked. That has finally changed for me in the last couple of months. Here are the 4 reasons why I have been accumulating this business.

1) The Platform For Companies Who Value Brand

E-commerce delivery has bifurcated into two very distinct paths. Some merchants value the audience and engagement that a large player like Amazon brings with hundreds of millions of consumers that flock to the Amazon platform every day. Yet, being a merchant on Amazon comes at a price.

The platform actively commoditizes suppliers and abstracts any form of brand differentiation to ensure that consumers capture maximum value. Of course, the scale and platform reach of Amazon are very difficult to replicate. For every merchant that is happy to seed its brand identity to the Amazon platform, there are others who still wish to engage in omnichannel commerce while maintaining a strong brand presence.

It’s here where Shopify comes in. Shopify has made a very successful business by enabling merchants to get online. At just $30 a month, SMBs can use a credit card to create an online storefront and manage pricing updates, coordinate inventory, and accept payments.

As it turns out, it’s not just SMBs that value the ease of use that Shopify enables. Shopify has more recently onboarded large merchants who want to maintain their own brand identity in e-commerce and has brought on larger customers such as Lord and Taylor, Heineken (OTCQX:HEINY) (OTCQX:HINKF), Staples, and others.

Shopify 4Q ’20 Investor Deck

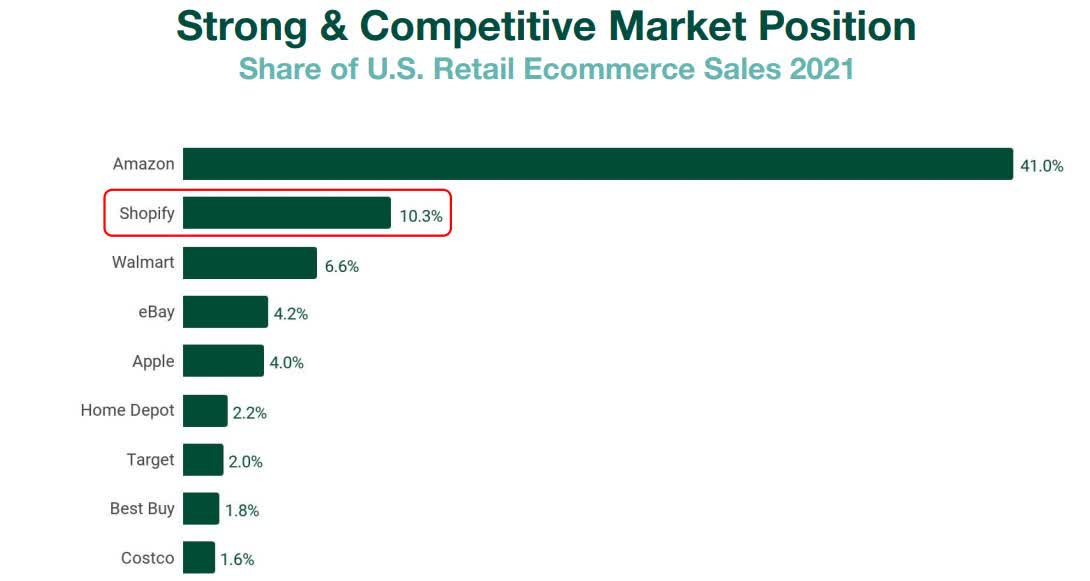

The demonstrated success of Shopify’s business model has seen it move into the #2 position in market share for e-commerce in the US, behind Amazon who is #1 by some considerable margin. However, these numbers don’t show that Shopify has steadily increased its share from almost nothing just a few years ago.

SHOP Q4’21 Investor Deck

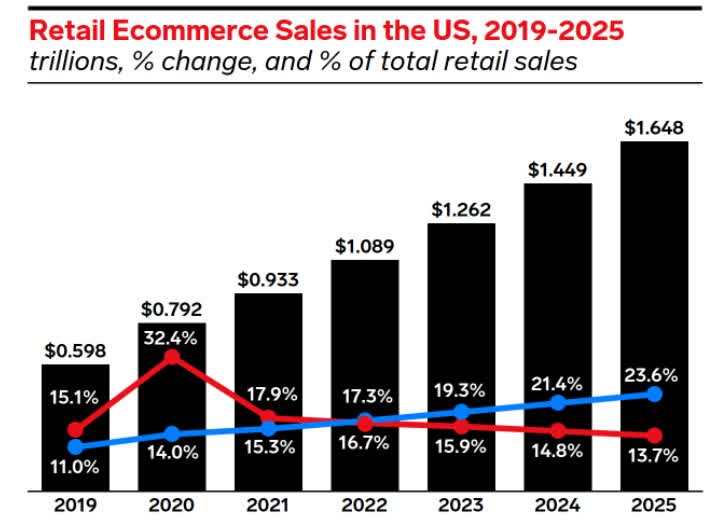

The runway for e-commerce is long. E-commerce will continue to increase at a mid-teens growth rate over at least the next three years in the US. Even then, it will still only make up less than 25% of total retail sales.

emarketer.com

Based on recent commentary from Shopify, the business expects to continue to capture a disproportionate share of commerce growth over the next few years. With brands having witnessed their commoditization on the Amazon platform, it’s more than likely that they will continue to invest in retaining their own brand identity for e-commerce efforts.

2) The Moat Is Sticky And Switching Costs High

While there are other providers of e-commerce enablement, such as Squarespace (SQSP) and BigCommerce (BIGC), the reality is that most merchants who gain any success or traction with their e-commerce offering tend to stick around on the same platform.

It’s typically not worth the pain and the hassle to move around e-commerce platforms if everything is working. Moving platforms introduces unnecessary integration risk with a new vendor and loss of data combined with potential downtime. Inertia is typically the order of the day when moving e-commerce platforms.

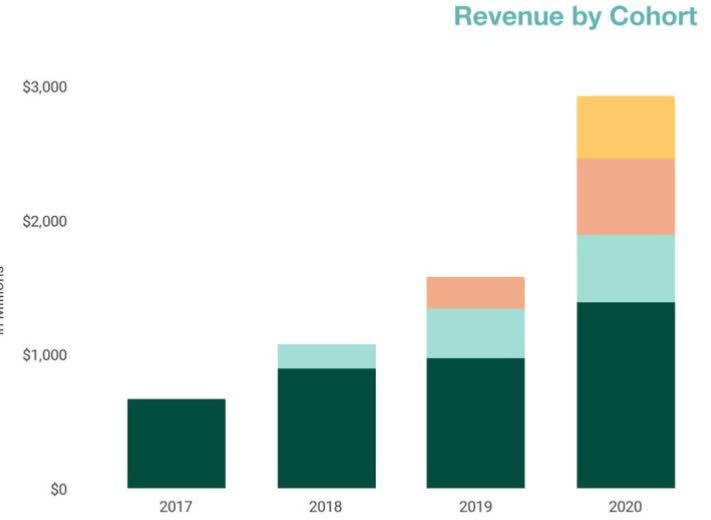

But data also empirically leads me to that view is that despite a relatively high failure rate amongst small and medium-sized businesses, Shopify has shown a consistent increase in the revenue per cohort for each merchant class. This fact suggests that the merchants that prosper tend to stick around and don’t leave the platform.

Q4’20 SHOP Investor Deck

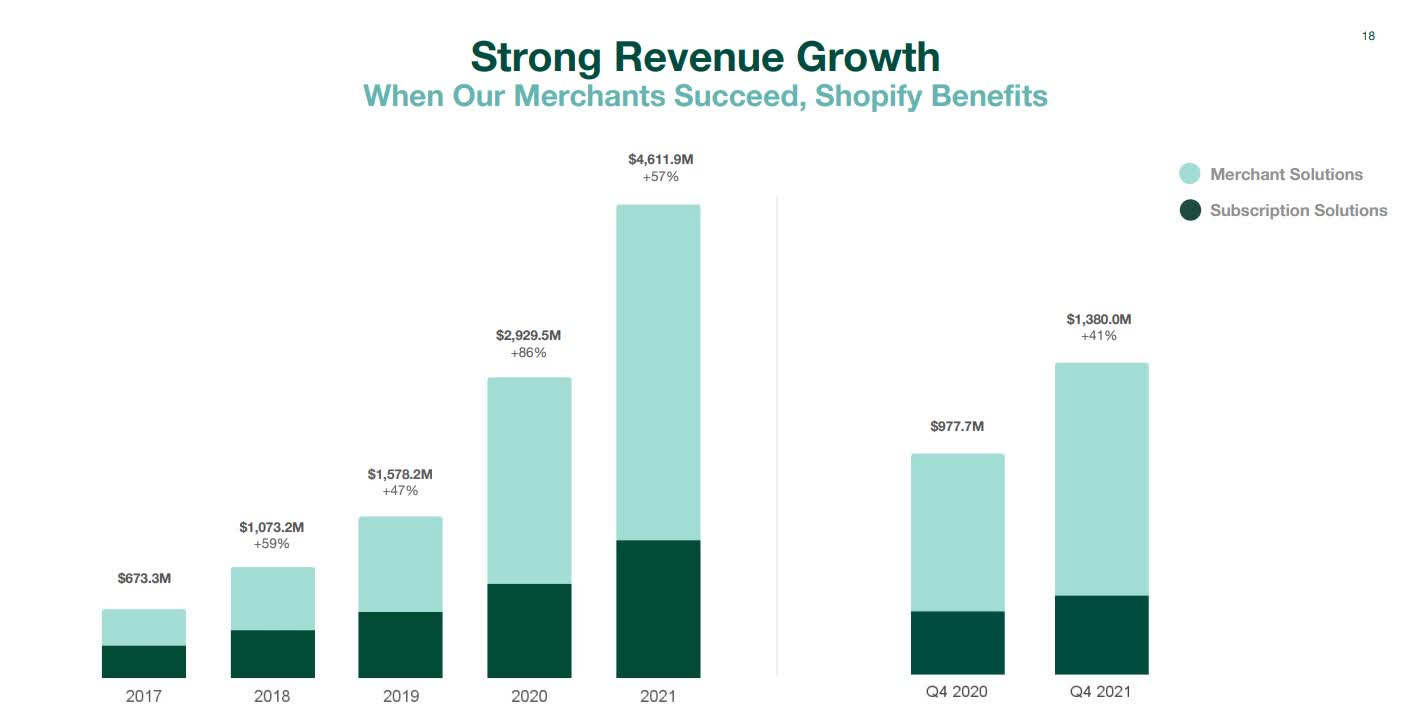

Shopify has two segments, one of which is Subscription solutions, which represents the recurring revenue Shopify gets from its e-commerce enablement, and Merchant solutions, which is transaction-based revenue for ancillary services delivered on the platform.

Shopify 4Q ’21 Investor Deck

Merchant solutions are the transaction toll that Shopify takes on merchants’ activity on its platform. Not only has this business grown much larger in scale than its recurring subscription solutions business in recent years, but it’s also growing much faster.

That suggests merchants consuming multiple modules and services on the Shopify platform and a high level of service utilization on the platform, which makes them increasingly unlikely to leave.

3) Ample Optionality In Areas Such As Fintech

Shopify has ample optionality and is now a large Fintech player. What’s most interesting about Shopify is the significant optionality that the business has developed over the last few years. The Shopify trojan horse is e-commerce enablement that expands into a comprehensive offering covering payments, fulfillment and logistics, financing, and other needs.

Essentially, Shopify’s premise is to capture all ancillary services spend to enable every dollar of e-commerce that merchants transact on the platform.

The business has been demonstrating meaningful success here. 51% of total gross merchandise volume on the Shopify platform is transacted with Shopify payments, up from just 46% in the prior year.

Shopify’s lending platform, Shopify Capital has increased its advances to merchants at 43% year-over-year. The business is bulking up its fulfillment offering through the Shopify Fulfillment Network.

SHOP has committed to owning more of the fulfillment experience and bringing this in-house compared to logistics via 3rd-party providers. This shift will help guarantee a better experience for merchants with faster, 2-day delivery times across 90% of the US.

The company is tapping into its partner ecosystem to enable new services and additional value for its merchants. The business has an ecosystem of more than 40,000 partners actively recruiting new merchants to the Shopify platform and an active developer army who have created more than 8,000 applications on which Shopify receives a revenue share for applications transacted.

Shopify is enabling new service delivery in the areas such as cross-border e-commerce through its partner Global-e Online (GLBE) and payment via installment through a partnership with Affirm (AFRM). The business has also been driving consumer e-commerce discovery of Shopify merchants through its Shop App, connecting its merchant ecosystem with consumers and helping drive awareness, engagement, and eventually revenue.

Shop App could ultimately be a significant gateway to boosting merchant attach of Shopify Payments, and helping introduce new revenue streams such as advertising, potentially monetized through Shopify Audiences. International expansion and other payment solutions such as money management are medium-term priorities that represent new growth areas for the business.

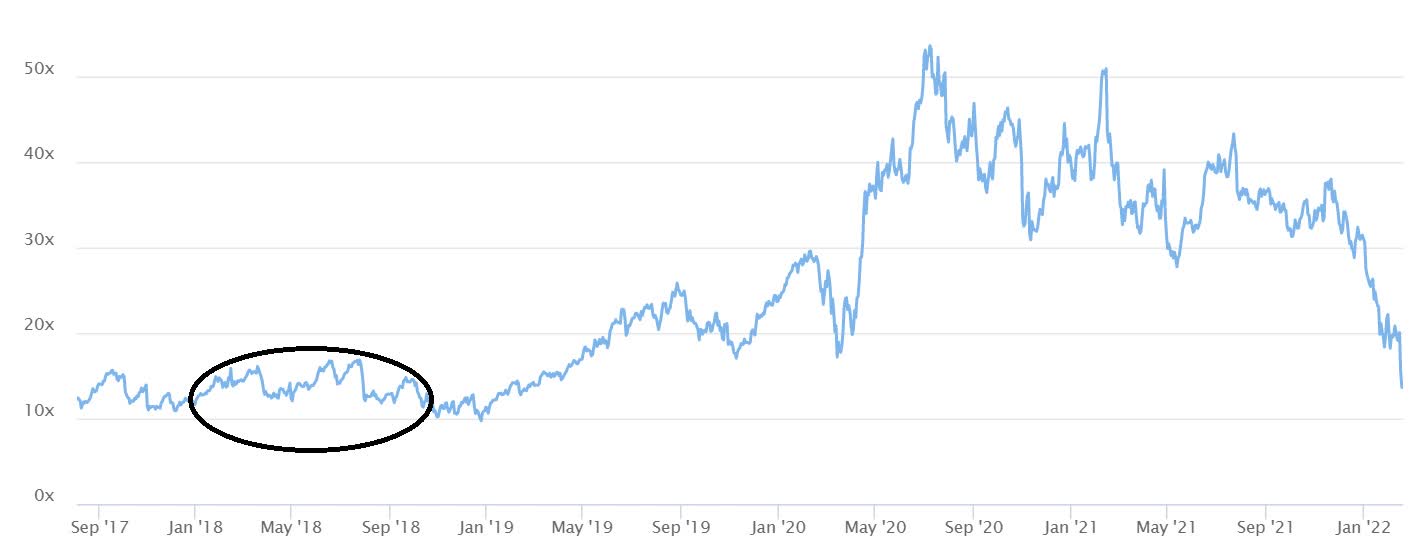

4) Valuation is Finally At A Level That Interests Me

While I didn’t doubt that the Shopify business was a good one, the area that I struggled with more with just what this business was worth. Recent prices well north of $1000 were not particularly interesting to me. I approach the Shopify valuation on a price-to-sale basis since the business is still investing capital in customer acquisition and new research and development initiatives.

tikr.com

What has particularly interested me at current prices is that on a price to sales basis for the next 12 months, Shopify now trades lower than its pandemic lows, and is now well within its long-term range, of 10 to 15x NTM sales. The business is also trading at lower multiples than when the 10-year bond rate was considerably higher than where it currently is today.

In my opinion, Shopify is a much better business than that of three or four years ago. It’s established a more extensive ecosystem with more partners and additional business revenue drivers. Given the current market conditions, I acknowledge that there is a risk that Shopify could trade lower.

Hence I will continue to average into the position should that occur. Still, I have built up a position that I am now quite happy to hold onto for the next decade and see how it performs, provided its business momentum continues to be there.

Risks

Several risks exist with the Shopify investment case. One of the largest currently is market risk and the likelihood that further derating the business could still be possible.

Shopify is also undergoing a considerable investment program over the next few years to develop its logistics and fulfillment capabilities further and own more of the fulfillment experience than relying on 3rd-party providers. Such investment will further delay free cash flow generation to the business, potentially depressing margins further, though increasing Shopify’s take rate.

Competitively, new players are also emerging in the marketplace, notably Squarespace and BigCommerce. While Shopify has a significant market share lead over both, the space is rapidly evolving and subject to shifts in market share.

Concluding Thoughts

Shopify provides the e-commerce operating system for millions of businesses to develop an Omnichannel presence and maintain their own brand identity. The business is now increasingly well-diversified and benefitting from various revenue streams, including payments and fulfillment revenues, with the potential of more to come.

The current pullback in the business from more than 60% from all-time highs represents an intriguing entry-level for those investors prepared to give this a long-term view.

While acknowledging the near-term risks, I am interested in building out and scaling in my Shopify position should the share price continue to fall, believing that the business could do quite well on a five-year time horizon.