Paul Hamilton/iStock via Getty Images

Author’s note: This article was released to CEF/ETF Income Laboratory members on January 7th, 2022.

The Cohen & Steers Quality Income Realty Fund (RQI) is an actively-managed, diversified, leveraged U.S. REIT CEF. RQI’s diversified holdings, strong 6.1% distribution yield, and market-beating returns, make the fund a buy.

RQI is a strong fund and investment opportunity, but less appropriate for risk-averse investors who wish to avoid leveraged funds or investments. For these investors, the Cohen & Steers Total Return Realty Fund (RFI), an extremely similar, unleveraged, fund by the same investment manager, might be a better choice.

RQI Basics

- Sponsor: Cohen & Steers

- Distribution Yield: 6.1%

- Discount to NAV: 2.4%

- Management Fee: 1.63%

- Leverage Ratio: 23.8%

- Total Returns CAGR 10Y NAV: 15.0%

RQI Overview

RQI is an actively-managed, leveraged CEF investing in common and preferred U.S. REIT securities. The fund is administered by Cohen & Steers, a small investment firm with a strong, proven track-record in the real asset management business, including real estate. RQI, being an actively-managed fund, benefits from having a strong management firm behind it.

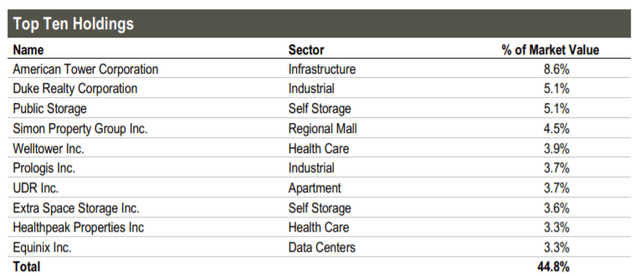

RQI is a well-diversified fund, with investments in 169 securities, and with exposure to most relevant REIT industry segments. Concentration is somewhat higher than average, with the fund’s top ten holdings accounting for slightly under 45% of its value. RQI’s largest holdings and industry exposures are as follows.

RQI focuses on large, blue-chip REITs, like Prologis (PLD) or American Tower Corporation (AMT). It also focuses on comparatively safe REIT industries, like infrastructure, while being underweight riskier ones, like malls. As such, the fund is unlikely to experience significant losses or underperformance.

RQI’s diversified, high-quality holdings and industries reduce portfolio risk and volatility, and are a significant benefit for the fund and its shareholders.

RQI’s holdings are also very similar to those of its index, the Vanguard Real Estate ETF (VNQ), with some caveats. For reference, VNQ’s largest holdings:

As can be seen above, both RQI and VNQ have very similar largest holdings. Both invest in American Tower, Prologis, Public Storage (PSA), and others. There are, however, relatively large differences in the weights of these holdings. RQI, being an actively-managed fund, overweight REITs which management believes are likely to outperform, and vice versa. As an example, RQI is overweight Public Storage, being its third-largest holding, but only the sixth-largest holding of the index. Public Storage has outperformed these past few months, so this was evidently the right decision, so far at least.

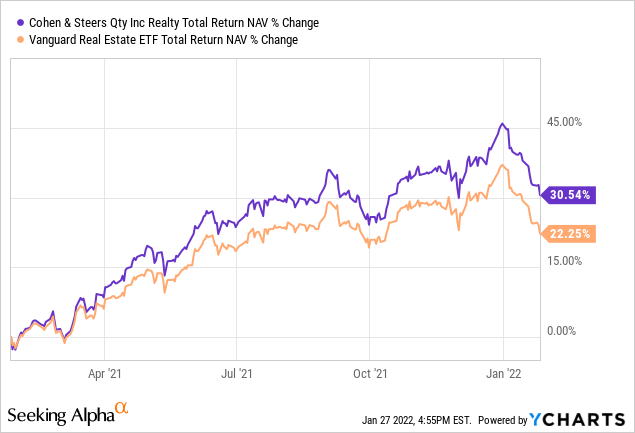

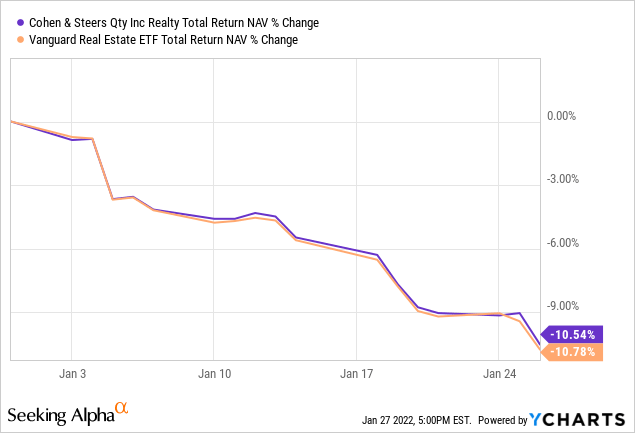

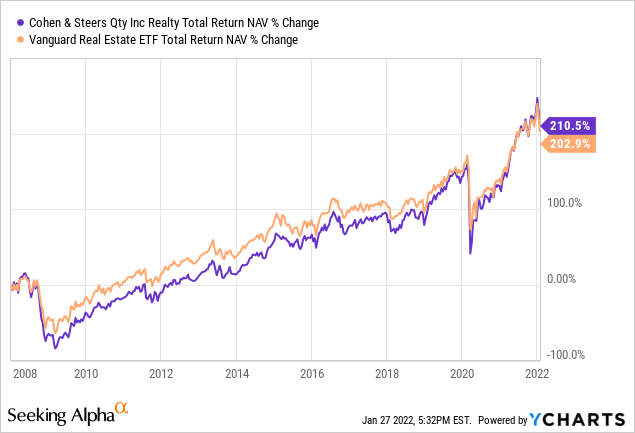

RQI makes several other small changes to its holdings and weights, trying to outperform the index, while maintaining broadly similar investments / exposures. As such, the fund’s investors receive most of the diversification and risk-reduction benefits of investing in an index, with the potential (and realized) market-beating returns of an actively-managed fund, a solid combination. This is very notable on the fund’s total return NAV graph, which quite clearly shows the fund closely tracking its index, as both have similar holdings, but with RQI consistently outperforming, due to consistent alpha.

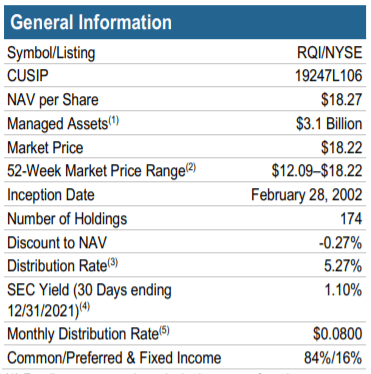

The fund focuses on common REIT shares, with these accounting for 84% of its value. Preferred REIT shares account for the remaining 16%. Preferred shares are higher on the capital stack, and so are safer investments. Preferred shares are also structured in such a way as to make (significant) capital gains unlikely. RQI’s preferred share investments serve to reduce both risk and prospective returns, but only slightly so, as preferreds only account for a small portion of the fund’s holdings.

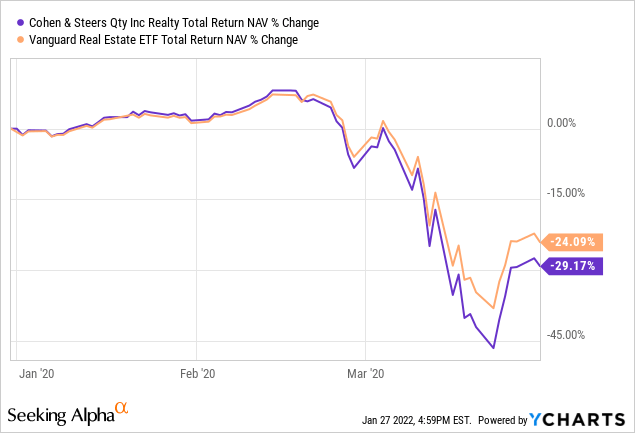

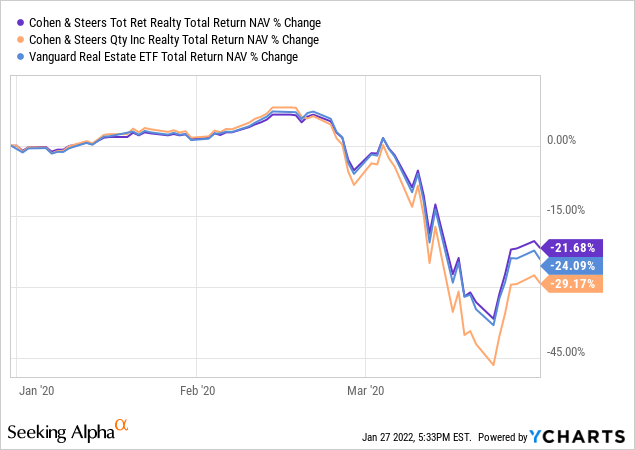

RQI is also a modestly leveraged CEF, with a 23.8% leverage ratio. Leverage means more assets, which means more income, capital gains, and total returns, but also losses during downturns. Leverage is particularly harmful during severe downturns and recessions, as a fund might have difficulties making interest rate or capital payments on its debt during these. RQI’s leverage ratio is quite modest, so its effect on these variables is low. Investors should expect the fund to slightly underperform during downturns, as was the case during early 2020, the onset of the coronavirus pandemic.

RQI’s leverage makes it difficult for the fund to outperform during downturns, but not impossible.

Distribution Analysis

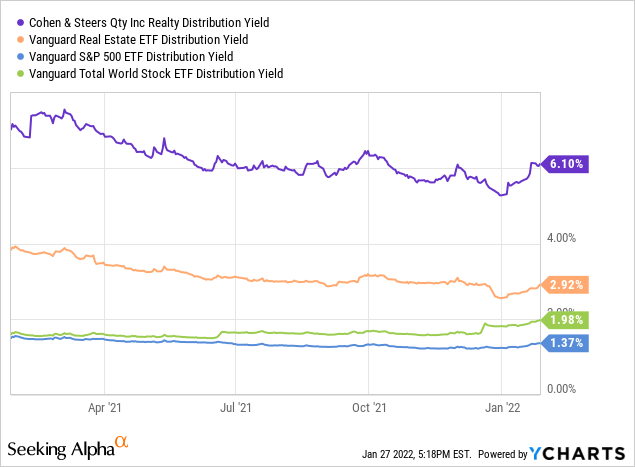

RQI currently sports a 6.1% distribution yield. It is quite strong on an absolute basis, and much higher than that of the fund’s index, as well as broader equity market indexes. It is, however, somewhat lower than that of its peers, with the average REIT CEF sporting a 7.0% distribution yield, as per CEFConnect data.

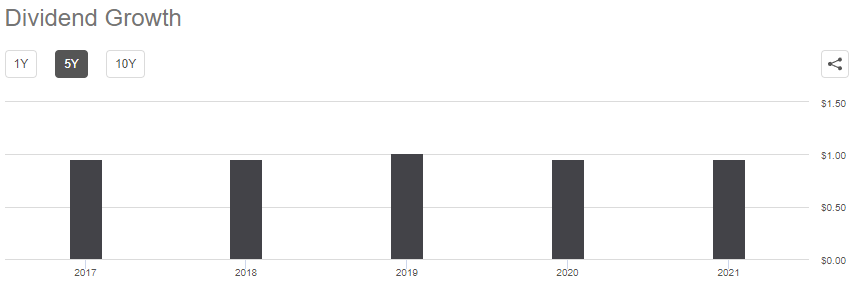

RQI’s distributions are also quite sustainable, with the fund paying the same $0.08 monthly distribution since 2015, with some growth in prior years. RQI’s distribution was extremely volatile in the years preceding the housing bubble. Although this is undoubtedly a negative, I don’t believe that information this old is all that material moving forward.

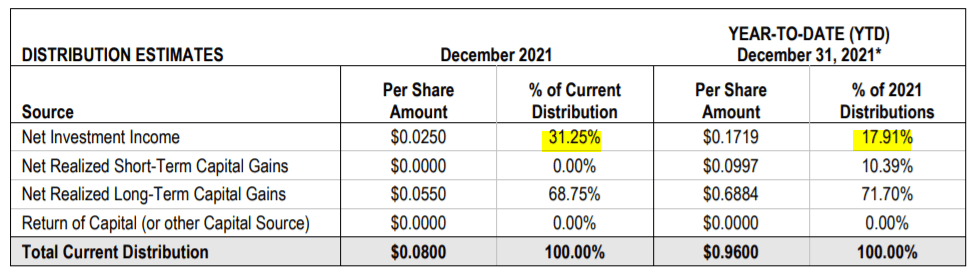

RQI’s distributions are quite strong, but barely covered by underlying generation of income. From company filings, it seems that the fund’s distribution coverage ratio is usually around 30%, which is where it stands as of December 2021. Lower distribution coverage ratios are common, with the fund sporting an average ratio of 18% for 2021, a very low figure.

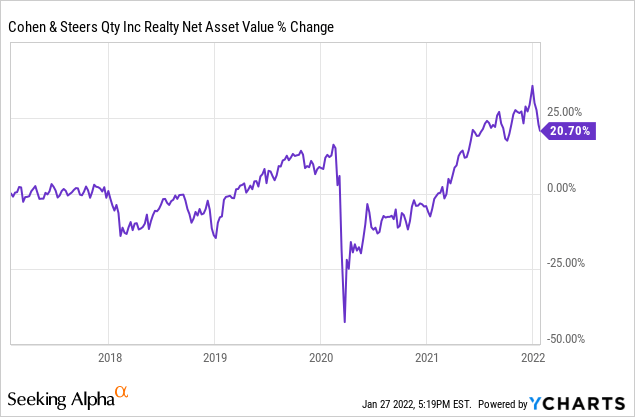

As should be clear from the above, RQI is reliant on capital gains and asset sales to fund most of its distribution. In the vast majority of cases, the fund generates sufficient capital gains to fund its distributions and grow its asset base. RQI NAV has grown at a 4.0% CAGR for years, and quite consistently so. Low distribution coverage ratios are not ideal, but as long as NAVs are growing the distributions are sustainable, and safe.

On a more negative note, capital gains should be non-existent during recessions and downturns, which might make it difficult for the fund to fund its distributions during these. Destructive return of capital distributions, or asset sales at unfavorable prices, are both a distinct possibility. Management might decide to cut the fund’s distribution instead. As such, RQI’s investors should expect the fund to cut its distribution during recessions and downturns, especially particularly severe, long-lasting ones.

The fund’s distribution was cut by a massive 43.5% in 2009, in the aftermath of the housing bubble, but survived 2020-2021 unscathed. Distribution cuts are likelier than not, in my opinion at least, but definitely not a certainty, as per the fund’s distribution track-record.

RQI’s strong 6.1% distribution yield is a benefit for the fund and its shareholders, and particularly important for income investors and retirees.

Performance Analysis

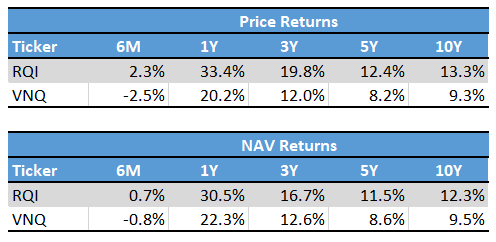

RQI’s performance track-record is quite strong, with the fund consistently outperforming its index, on both a NAV and price basis. Returns were due to a combination of distributions and capital gains, slightly more of the latter. Price returns were slightly higher than NAV returns, especially these past few months, as the fund’s discount to NAV has narrowed. The fund currently trades with a small 2.4% discount to NAV, so further discount narrowing seems unlikely.

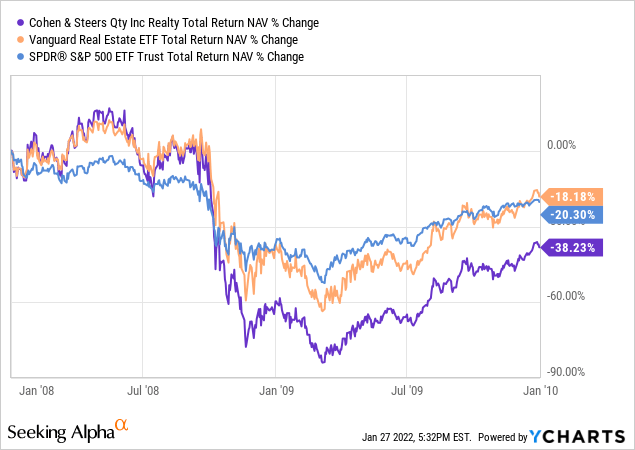

Seeking Alpha – Chart by author

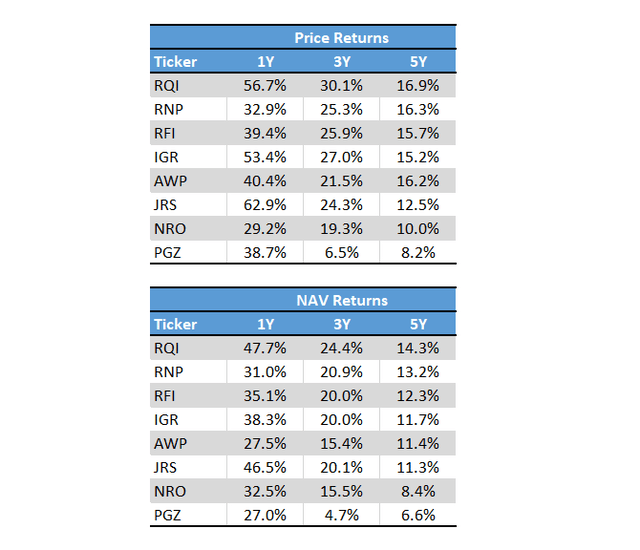

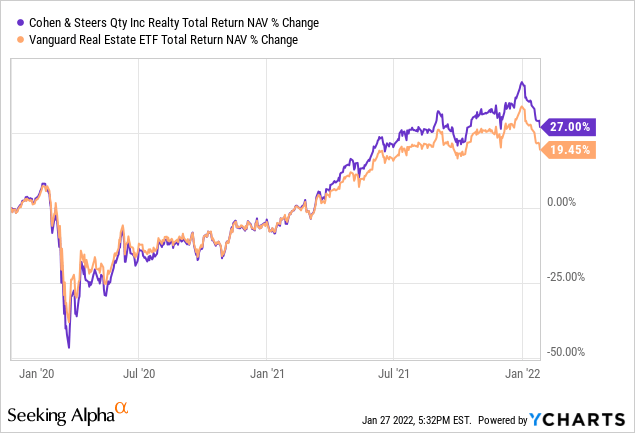

RQI is also the REIT CEF with the strongest long-term performance in the industry, on both a price and NAV basis. RQI has outperformed its peers for more than a decade, and for most relevant time periods too. As a small aside, the figures below are slightly different from the ones above, as the former come from CEFConnect, and are outdated by a couple of days.

RQI’s strong performance is partly due to the fund’s use of leverage, and partly due to its consistent generation of alpha. Cohen & Steers is a fantastic real asset manager, which has consistently generated alpha and market-beating returns, and which will, I believe, continue to do so in the future.

RQI – Risks and Drawbacks

RQI is a strong fund and investment opportunity, but it does have one significant drawback: its use of leverage. As mentioned previously, leverage means more assets, which means more income, capital gains, and total returns. Leverage also means more losses during downturns, and these could prove ruinous during a particularly severe downturn.

RQI faced a brutal recession in 2009, as the housing bubble and attendant crash caused REIT valuations, prices, and distributions to crash. RQI significantly underperformed its index, as expected.

RQI’s use of leverage severely hampered the fund’s recovery, as the fund was forced to make interest rate and capital payments on its debt on a reduced asset base. It took the fund close to three years to recover from this debacle, versus around two and a half years for its index. RQI also took about twelve years to outperform relative to its index following the financial crisis, even as the fund’s performance post-crash was fantastic. In other words, for RQI, two years of excess losses were equal to twelve years of excess returns, very lopsided figures.

Importantly, leverage is really only a significant negative during severe, long-lasting downturns. RQI recovered from 2020 coronavirus crash just fine, as this was a shallower, shorter crash.

As should be clear from the above, RQI is a somewhat risky fund, and inappropriate for more conservative income investors and retirees. For these investors, RFI is the obvious alternative.

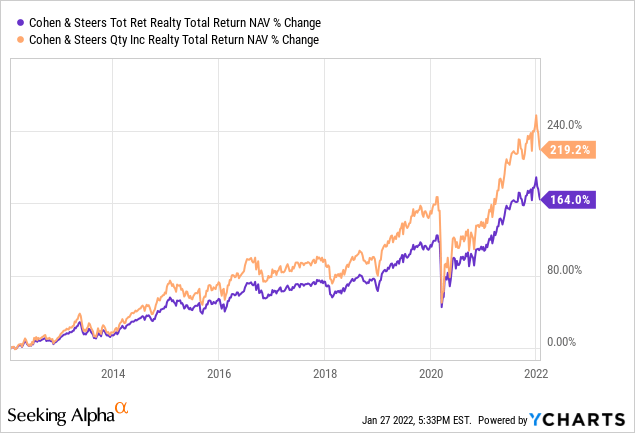

RFI is another REIT CEF by the same investment management firm, and shares most of RQI’s characteristics. RFI is unleveraged, and so performs much better than RQI during downturns, as was the case during the past financial crisis.

RFI’s lack of leverage also means the fund underperforms during recoveries, bull markets, and most other relevant market conditions. RFI has underperformed RQI for the past ten years or so, and for most other relevant time periods too.

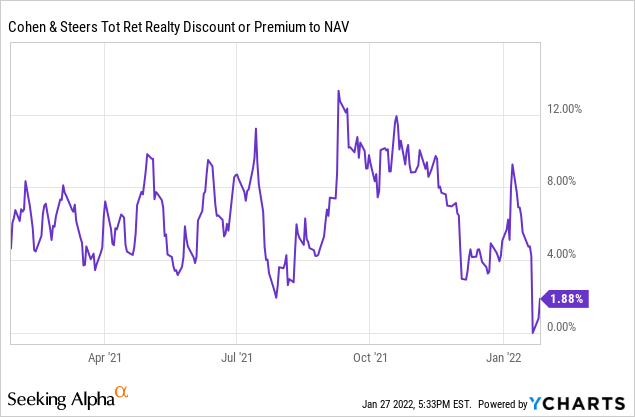

RFI is an outstanding fund, and particularly appropriate for more risk-averse investors and retirees. I actually believe that RFI is, on net, the stronger fund. The market seems to agree, and so RFI consistently trades with a large premium. The premium has, however, significantly dropped these past few days, and currently stands at 1.9%. At these levels, I think investors should strongly consider an investment in RFI, but with a close eye to current discounts and prices.

Conclusion – Buy

RQI’s diversified holdings, strong 6.1% distribution yield and market-beating returns make the fund a buy.